This article is from the Australian Property Journal archive

THE Sydney and Melbourne residential markets are 45% and 49% overvalued and prices are tipped to fall in the year ahead, while Darwin’s market is yet to bottom out, according to SQM Research.

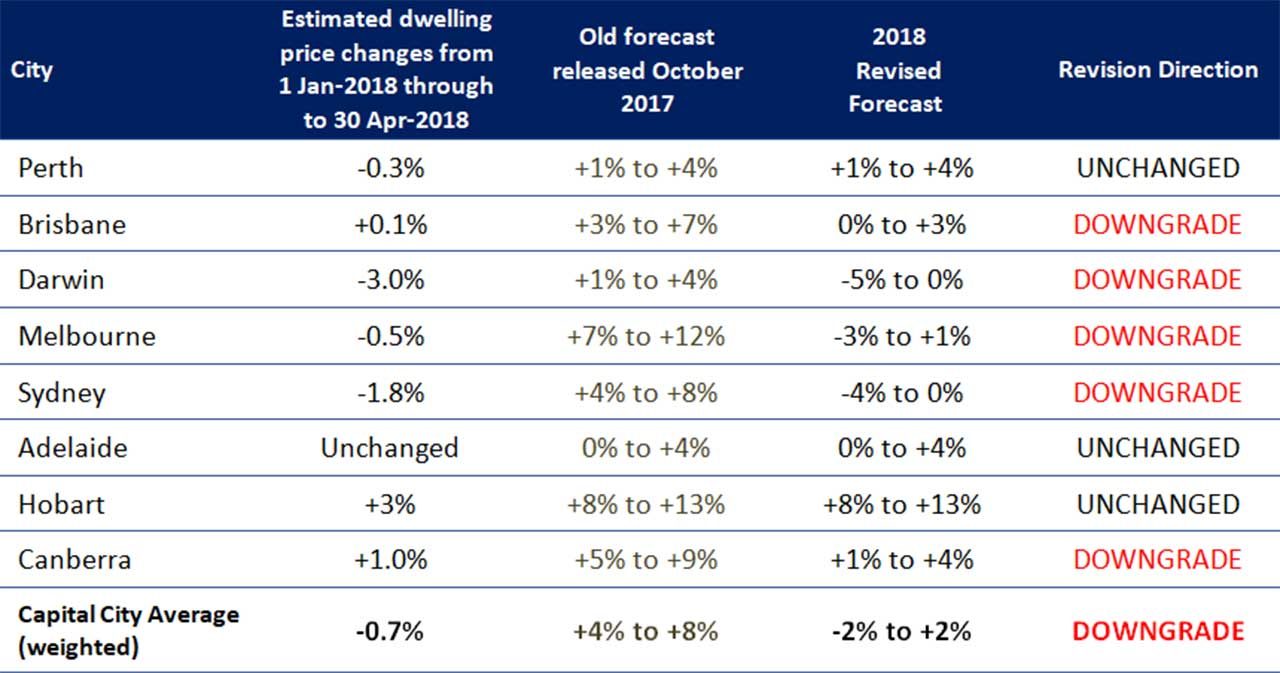

The weighted capital cities forecast for this year was taken from growth of between 4% and 8% to between a drop of 2% and rise of 2%, on the back of auction lower clearance rates, aggregated property listings and asking prices.

Five capital cities were downgraded, including Brisbane and Canberra as well as Sydney, Melbourne and Darwin.

“The evidence now suggests that action to reduce borrowings risks is now affecting the national housing market as a whole,” SQM Research managing director Louis Christopher said.

It follows NAB’s downgrade in recent weeks for national house price growth of 0.7% to negative 0.8%, also based on soft performances in Sydney and Melbourne.

That followed ANZ’s declaration that the national residential market slowdown had already occurred, with the slowdown seeing a fall in growth to around 1% in the second quarter before ending at 1.9% for 2018, and accelerating again through 2019 to 4.1%.

Meanwhile, AMP Capital chief economist and head of investment strategy, Shane Oliver, has said Sydney and Melbourne house prices would fall a further 5% this year.

SQM Research does not expect a general housing price crash to occur this year. Christopher said the conditions required to create such a downturn are not in the housing market at present, with the national economy healthy overall, unemployment relatively low and stable, population growth very strong, and oversupply of new real estate only occurring in pockets.

“Moreover the correction now experienced in Sydney will likely be restricted to single digit percentage price declines (from peak to trough). However, there may well be a period of extended stagnation in the market unless authorities take action to stimulate the market.

“If there is a more pronounced downturn, SQM Research believes that monetary authorities as well as federal and state governments may intervene to stabilise the market,” he added.

Hobart was unchanged and remains the clear leader for growth in 2018, from 8% to 13%. Perth remained at growth of 1% to 4% and Adelaide from stable to a 4% increase.

Sydney’s outlook has been taken down from growth of 4% to 8% and could now drop by 4%, assuming property investors return at a tempered rate following APRA’s recent lifting of its benchmark of 10% growth in lending to housing investors.

Christopher, said recent auction results in Sydney suggest market activity further deteriorated during April, with results of the last weekend possibly pushing the clearance rate below 50%. Current levels have historically led to price falls.

Listings have grown by more than 34% in annual terms and are now at similar levels to 2011, when prices fell 3% for the year, and listings are tipped to rise further this month. Days on market for listings has increased from 107 days to 118 over 12 months, and asking prices in April fell 1.1% for houses and 0.6% for units.

“This suggests a degree of capitulation by property sellers which will likely mean a negative pricing result for the June quarter,” Christopher said. “Given the loosening of investment property credit growth restriction, there may be a response from Sydney investors. However, given other housing credit restrictions it is unlikely that the response will be significant,”

Christopher said that on a nominal aggregate incomes-to-dwelling prices measure, the Sydney market is around 45% overvalued.

Melbourne was downgraded to a fall of 3% up to a 1% rise. Auction clearance rates have fallen to the low 60% to high 50% range. The inner regions have seen softer rates, and the south-east and north-east are a little higher.

Listings remain low recent rises have them at 6% higher than 12 months ago. Asking prices have slowed from annual growth of 22% to between 5% and 7%.

“SQM Research expect vendors to adjust to the market further in coming months as days on market for listed properties is increasing,” Christopher said.

The market is around 49% overvalued.

Christopher said the significantly-slowed sales turnover would have negative ramifications for stamp duty receipts, particularly in New South Wales and Victoria.

Brisbane’s base case forecast has been downgraded by 4%, to 0% to 3% growth. Auction activity has been weak, at as low as sub-40%, but private treaty campaigns are broadly the preferred sale method. Listings have been trending up recently, driven by inner-city units.

“Building approvals are falling and this will eventually help absorption levels of existing surplus stock. However, given the very slow investor take up, it will take many months before the market returns back to equilibrium,” Christopher said.

Vacancy rates in Darwin were recorded during the March quarter, a time in which vacancies typically fall.

“This was an unexpected event and reduces our confidence that the bottom is in place for the Darwin housing market, which has experienced a four-year housing downturn,” Christopher said.

Rents fell by a further 1% for houses in April, now sitting below 31% their peak, and 0.5% for units, 45% down from the peak. Property listings are at more than double the lows recorded before the downturn.

Canberra listings have grown after a strong market in 2017, and they now sit at levels seen during the downturn of 2012. Rental vacancies have remained tight, currently at 0.6%, and rents have accelerated with 12-month increases of more than 7% for houses and units. The price forecast for 2018 has been downgraded by 4% to 1% and 4% growth.

Australian Property Journal