This article is from the Australian Property Journal archive

SYDNEY and Melbourne industrial market rents were stable over the second quarter even as vacancies pick up.

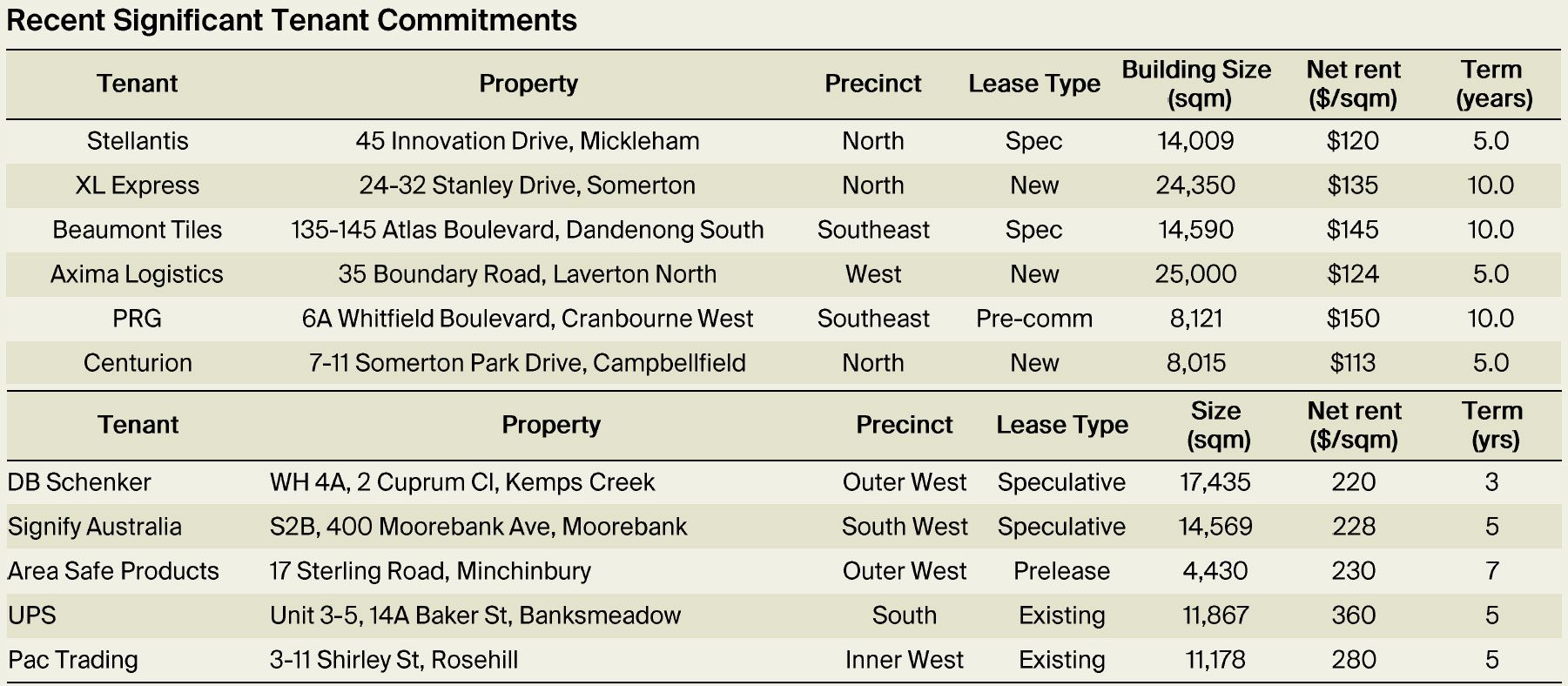

According to the latest research from Knight Frank, Melbourne’s prime net face rents were up just $1 to $141/sqm over the Q21 2024, reflecting a 7.7% increase over the last 12 months.

At the same Melbourne’s industrial vacancy rate was up 7.9% from the first quarter, with 865,916sqm available at the end of Q2, sitting 16% above the 10-year average.

Over the year so far, 548,188sqm of new space has been completed in Melbourne, with the pipeline will strong.

The second quarter saw 327,979sqm of warehousing leased, well ahead of its five-year average. This after Melbourne’s Q1 take up was down to 195,573sqm, which was a five-year low.

“In Melbourne we have seen a significant positive change in take up, which we expected. The reduction in Q1 was due to prospective tenants taking longer to make leasing decisions due to the greater availability of options and a lack of urgency,” said James Templeton, national head of industrial and logistics at Knight Frank.

“Across the board tenants have more options, which is a good thing as we can better match occupiers with the right facility rather than them securing any space they can find, which leads to a more efficient use of industrial property.”

This comes as a recent Cushman & Wakefield report found industrial and logistics space should see greater demand and rental growth over the second half of 2024 and into the new year in key precincts.

Meanwhile, Sydney’s prime net effective rents have remained stable since late-2023, with vacancies up 9% to circa 250,000sqm, which is 46% under the historical average.

New supply in Sydney is forecast to hit 866,000sqm, with around 343,800sqm delivered in 2024 so far.

“While vacancy rates have risen, they are now at a level that is more in line with the average and they are still low in terms of historical figures,” added Templeton.

“The fact that rents in Melbourne and Sydney have remained stable following very strong growth indicates that demand for industrial space is still strong, with the rise in vacancy rates largely attributable to the significant development pipeline rather than a drop off in demand.”

Prime incentives in Melbourne and Sydney were averaging 15.3% and 9.3% respectively.

With Sydney prime yields stable at 5.46% and Melbourne rising five basis points to 5.55%.

“This is a positive sign for the investment market, and we expect the increased certainty will lead to greater activity over the second half of the year,” said Tony McGough, partner, research and consulting, at Knight Frank.

“In Melbourne, the quarter saw small lot – of less than 5,000sq m – and medium-sized – of 1 to 5 hectares – land values rise, by 2% to $1171/sqm and 2.4% to $925/sqm respectively.

“For large sized lots of 10 hectares-plus, land values fell 5.8% over the quarter to $325/sq m. However, this was not due to a fall in demand, but the fact that what was available in prominent suburbs has been mostly sold, with up-and-coming development locations, where values are lower, now offering the greatest amount of land.”

CBRE’s H1 2024 Australia’s Industrial and Logistics Vacancy report recently revealed Australia to held the lowest vacancy rate in the world, at 1.9%, with Perth the lowest in the country at 1.2%.