This article is from the Australian Property Journal archive

OFFICE sublease availability has dropped or remained steady across all major CBD markets except Melbourne as businesses seek out competitively-priced office space with high-quality existing fit-outs.

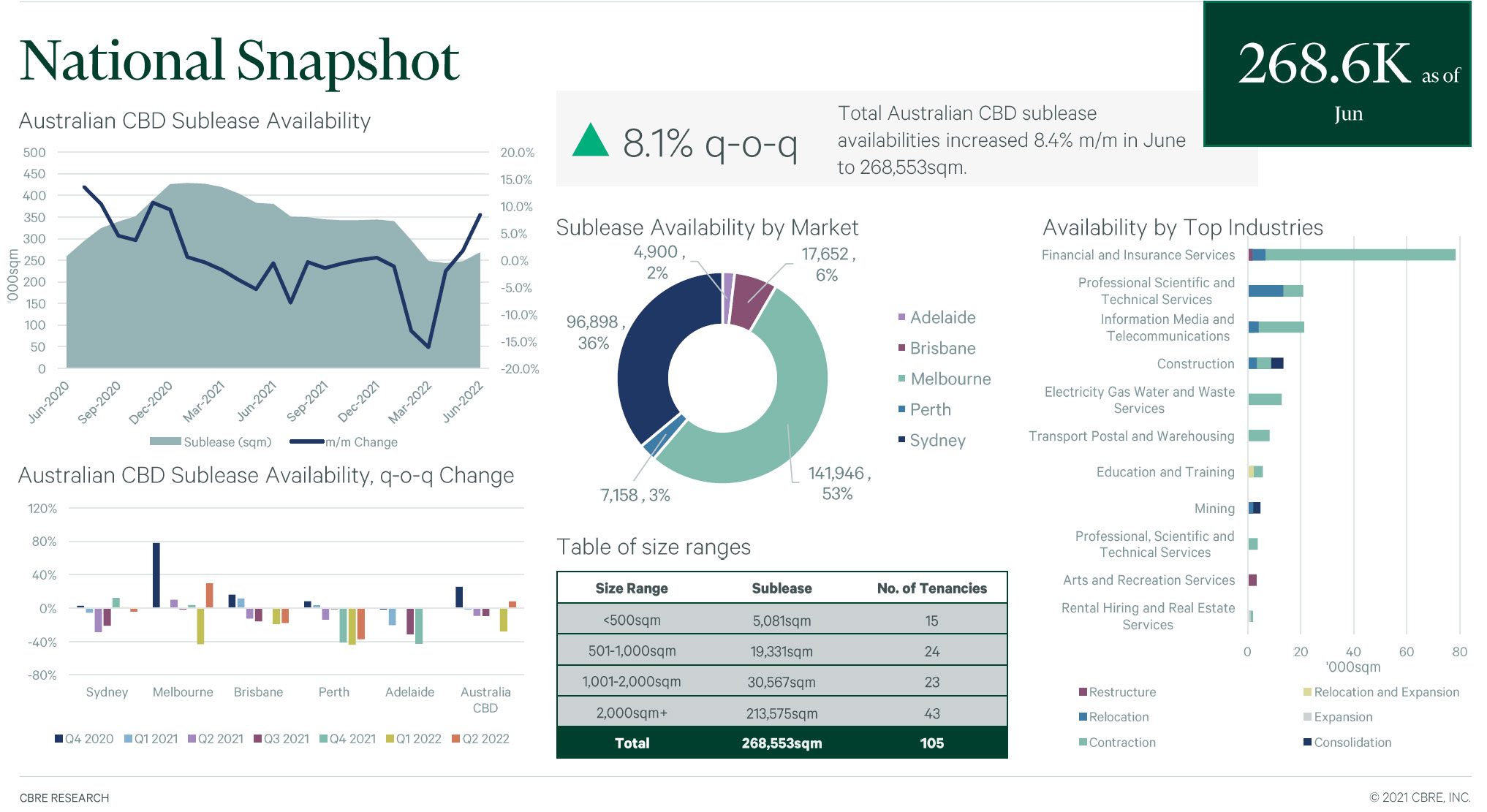

CBRE’s latest Sublease Barometer showed Melbourne’s 29.6% rise pushed quarterly national sublease availability upwards by 8.1% in the June period, the overall 268,553 sqm tally of sublease stock remains 26.3% below that recorded at the end of December and well below the market peak of 428,600 sqm in January 2021.

“The long-term trend remains positive as tenants proactively pursue competitively priced space with high quality existing fit-outs,” CBRE’s Pacific head of office leasing Mark Curtain said.

“While sublease vacancy will continue to fluctuate in the short term, particularly as major users resolve their long-term office accommodation strategies, we expect it to trend back toward the historic average to represent about 1.0% of Australian CBD office stock.”

CBRE’s data shows the Sydney, Brisbane and Perth CBDs recorded sublease declines of 4.1%, 17.9% and 37.4% respectively throughout the June quarter, while Adelaide’s sublease availability remained unchanged.

CBRE research senior analyst Nick Baring noted that while the stock of space in Melbourne had risen by nearly $30 to 141,946 sqm, availability was still 26.3% lower than December.

“Some occupiers are adjusting their office footprint and are capitalising on strong occupier demand for pre-fitted space. That said, sublease activity continues to be fluid and with tenants already in advanced discussions on some of the larger sublease tenancies that have been brought to market in recent months, overall availability is expected to decline in the coming months.”

The large bulk of Melbourne’s 53 sublease spaces available are A-grade space, and by size is available in 2,000 sqm-plus spaces. There are currently 23 of these, totalling more than 117,000 sqm. There are 10 spaces ranging from 1,001 to 2,000 sqm that total over 12,600 sqm.

Financial and insurance services account for 40,000 sqm of Melbourne’s total, followed by professional, scientific and technical services (just over 20,000 sqm), then electricity, gas, water and waste services, and education and training.

While occupiers nationally have a better sense of their space requirements, workspace reviews are expected to continue until the end of the pandemic.

“Against this backdrop, we expect the Sydney and Melbourne sublease markets to remain active. Due to cost pressures, further additions and current availability is likely to be absorbed, given most sublease space is fitted and in prime grade buildings.”

While those workspace reviews will be ongoing, the return to the office stalled in June amid COVID, colds and flu, with occupancy rates hardly moving across the city’s CBDs.

Sydney has 96,898 sqm of sublease space available across 36 tenancies, with nearly 77,000 sqm made up of 2,000 sqm-plus spaces. Financial and insurance services account for 40,000 sqm, and construction companies more than 20,000 sqm. Premium-grade space accounts for 65% of that available.

The most common tenancies in Sydney and Brisbane are three to five years, while in Melbourne it is five years-plus.

Brisbane has 17,652 sqm of sublease space across seven tenancies, with nearly 13,600 sqm being from four tenancies of 2,000 sqm plus.

In Perth, the 7,158 sqm available is evenly spread across tenancy sizes and A and B-grades. Adelaide’s 4,900 sqm available is mostly A-grade.

Demand for office space increased by 11% to more than 1.622 million sqm in the first half of the year, led by a spike in enquiries in Brisbane, according to Colliers. Landlords of those larger spaces up for sublease might be encouraged by the total being driven by the 3,000 sqm-plus market in particular.