This article is from the Australian Property Journal archive

AFTER an extended stand-off between vendors and buyers on the prices of office buildings, shopping centres and warehouses that saw hefty devaluations, the prospect of further global interest rate cuts has brought the market trough to the horizon – and the retail market is set to lead the recovery in values.

Cushman & Wakefield’s Australian CRE Glidepath report indicates overall commercial real estate investment volumes are already showing signs of positive momentum – investment volumes across markets in the June quarter totalled $10.1 billion, more than double the $4.9 billion transacted in first three months of 2024.

The firm’s commercial property price index (CPPI) is forecast to decline 8% peak-to-trough once valuations bottom out in early 2025. Offices are forecast to see the largest repricing, falling 25%, followed by industrial (down 3%) and retail (down 11%).

Investor sentiment towards commercial property is beginning to lift. The proportion of commercial real estate professionals who view the market as being in a downturn has declined from a peak of nearly 75% at the end of 2022 to 45%, roughly equal to the number who see the market as having reached bottom or being in the early stages of an upturn (43%).

Aggregate volumes are expected to continue rebounding through 2025 to reach $47 billion for the year as clarity on the path of interest rates close the bid-ask spreads between buyers and sellers. At one stage during the recent freeze in transactions, MSCI Real Assets found the gap between buyer and seller expectations has widened, implying that the current repricing cycle, which has already outstripped the correction seen during the global financial crisis (GFC), prices need to fall by at least another 18%.

Lower bid-ask spreads will allow capitalisation rates to stabilise throughout the year, before cap rate compression begins in 2026, according to Cushman & Wakefield.

“As we pass through the cyclical bottom and the direction of rates becomes clearer, the subsequent recovery in volume is allowing for prices to adjust across the commercial property market,” Cushman & Wakefield’s national economics and forecasting manager, Sean Ellison said.

“We’re seeing cap rates at or approaching their peaks and expecting spreads to settle in a far narrower range by the first half of 2025. The value of retail assets has already found its stabilisation point and is poised to rebound, and we expect industrial and office markets to follow.”

Retail to leader

The research indicates that the retail market is poised to lead the recovery in values. The CPPI is forecasting a 16% upward repricing from Q4 2024 and 2030. Investment volumes in the June quarter totalled $1.4 billion, and are expected to grow to $2.9 billion each quarter by the end of next year, with more key deals already starting to trickle through.

The logistics and industrial sector saw cap rate expansion have a minimal impact amid stronger rents and lower vacancies. The sector is forecast to see a price increase of 19% between the first quarter of 2025 and 2030. Investment volumes in the June quarter were recorded at $2.6 billion, up from less than $900 million the previous quarter, and will reach $3 billion by late 2025.

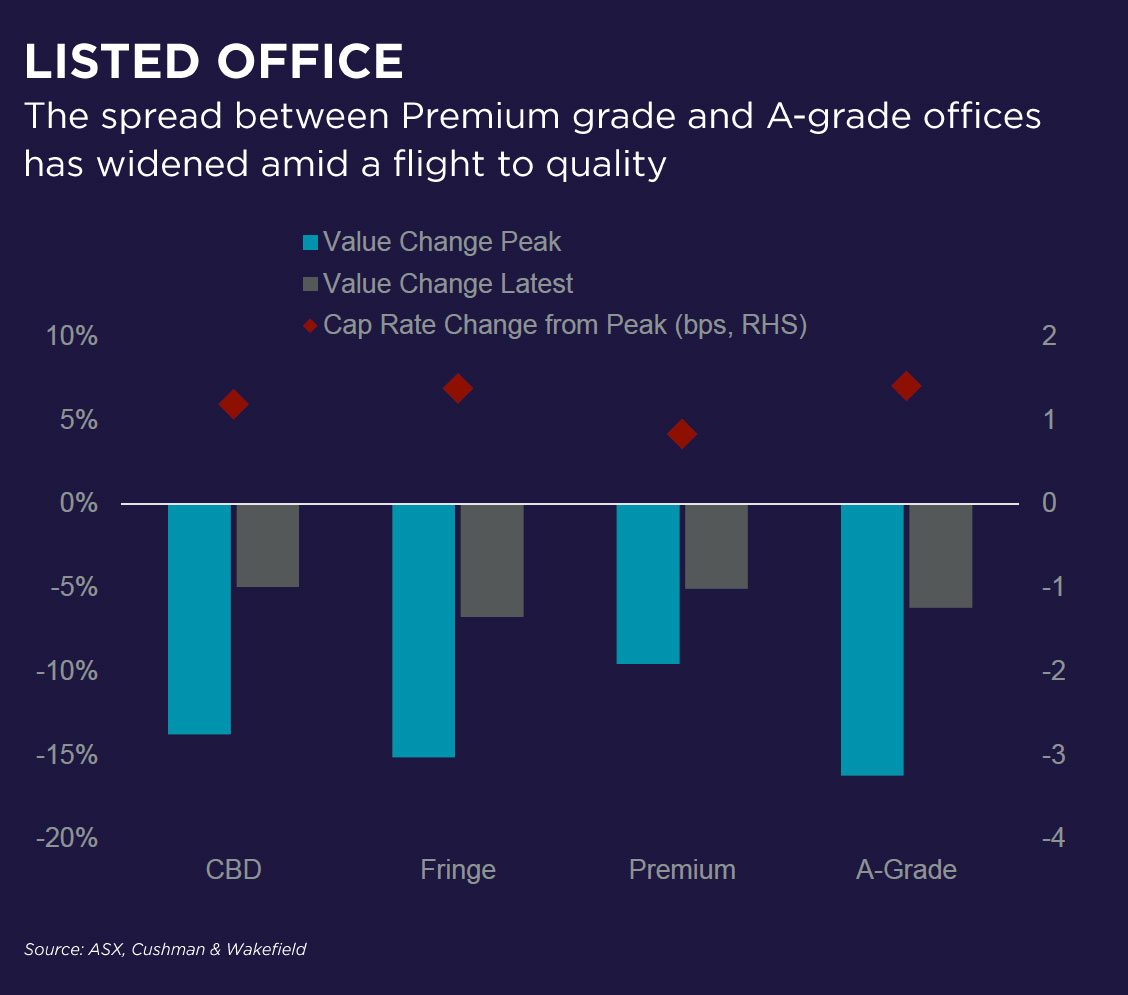

The effect of cap rate expansion on values has been most acutely felt in office markets, as the sector faces structural headwinds in the form of the working-from-home trend and higher interest rates. As vacancies tighten and incentives decline, particularly for higher-grade assets, the CPPI shows the most significant rebound of 28% from Q1 of 2025 to 2030 – although will not reach peak values seen in mid-2022.

Office investment volumes also rose more than $2 billion quarter-on-quarter in Q2 to $3.5 billion and is predicted to rise to $4 billion by the end of 2025.

Alternative assets are predicted to form a larger share of overall CRE investment volumes, rising from $9.3 billion in 2024 to $11.5 billion in 2025. Alternative assets are forecast to comprise circa 25% of overall CRE transaction volumes over the next five years, jumping from 15% in the 2015 to 2019 period.

Cushman & Wakefield’s head of international research, Dr. Dominic Brown said there is close to $70 billion in capital across Asia Pacific sitting on the sidelines “looking for the right time to re-enter the commercial property market”.

“Almost two-thirds of that forms part of opportunistic, value-added or debt strategies and is searching for higher yields, and Australia remains a preferred destination for capital across the region.”