This article is from the Australian Property Journal archive

AUSTRALIAN farmland values continued to grow through the first half of 2024 – marking a 22nd consecutive half-yearly period of annual increases – with north-west Tasmania home to the dearest farmland, and as commodity prices, seasonal conditions and interest rates all made different impacts across the country.

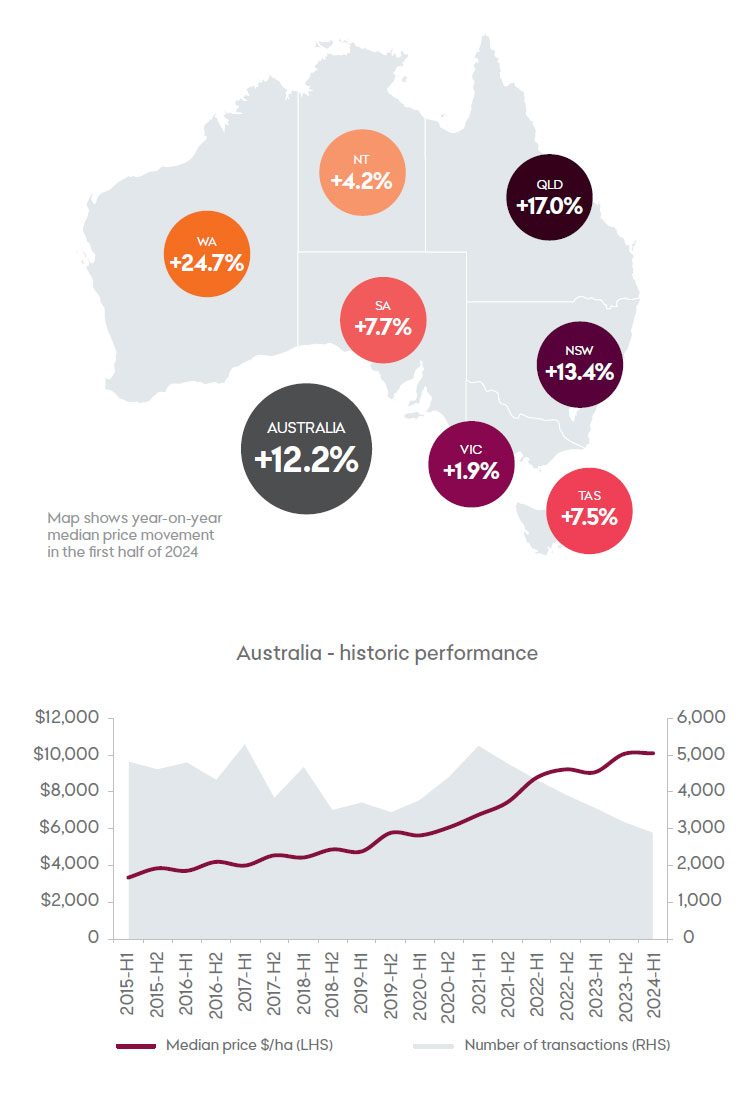

Rural Bank’s Australian Farmland Values Mid-Year Update 2024 showed the median price of farmland in the first half was $10,141 per hectare, up 12.2% compared to a year earlier.

This was an improvement of the slower year-on-year growth seen in the prior two half-yearly periods. After surges of 20% to 30% through 2021 and 2022, growth stalled to 3.2% in the first half of 2023, before improving to 9.6% in the second half of 2023.

While there was growth on a year-on-year basis, the median price in the first half of 2024 was essentially unchanged from the second half of 2023, down just 0.1%.

North-west Tasmania is home to Australia’s most valuable farmland, coming in at $28,827 per hectare, while the whole state’s median rose to a record high of $24,492 per hectare, a 7.5% increase on a year earlier.

This year, north-west Tasmania has seen Greenham Group hang up the for sale sign at blue-ribbon Westmore, optimised for beef or dairy production, with expectations of over $70 million, or nearly $20,800 per hectare. The 3,368-hectare Westmore is believed to be one of the largest contiguous holdings of agricultural land in Tasmania.

That came hot on the heels of Chinese billionaire Xianfeng Lu’a Van Dairy company putting up one of Australia’s biggest dairy operations to the market, comprising 9,500 hectares of farmland in Circular Head. Van Dairy had just sold a neighbouring 700-hectare farm to Prime Value for $15 million, at more than $21,400 per hectare.

Neil Burgess, Rural Bank senior manager industry affairs said, “At a national level, the story is essentially about stability in values with transaction volumes continuing to tighten as buyers increasingly fail to meet sellers’ price expectations.”

The major drivers of farmland values – commodity prices, seasonal conditions and interest rates – were mixed across regions and commodities, and reflected in the differing performances between states. Dry conditions proving challenging for most of southern and Western Australia, while Queensland and NSW experienced favourable rainfall.

On the upside, Queensland, particularly in the central highlands and south-east and the Hunter and North Coast of NSW, saw a continuation of strong growth trends due to more favourable seasonal conditions supporting buying intentions. Values lifted by 5.6% in both states over the half.

Victorian values have plateaued over the past 18 months, with the first half registering a half-on-half decline of 6.7%. Western Australia and South Australia both battled dry conditions in the first half of 2024 which likely translated into median prices falling from the record highs seen in the second half of 2023, down 12.1% and 11.0% respectively, although both saw continued growth on a year-on-year basis.

“The recovery of livestock prices after a disastrous 2023 and an easing in crop prices helps explain the variety in the median price movements we have seen around the country.

“In general terms, the traditional drivers of farmland values have led to a more subdued buyer appetite”, Burgess said.

“These factors are set to keep farmland values in a holding pattern for the second half of 2024, however, the longer-term outlook appears optimistic as demand may again strengthen if current rainfall forecasts provide a good finish to 2024 and interest rate cuts begin in early-2025.”

| Median price per hectare (H1-2024) | Price change from H2-2023 | Price change from H1-2023 | |

| National | $10,141 | -0.1% | +12.2% |

| QLD | $9,777 | +5.6% | +17.0% |

| NSW | $9,745 | +5.6% | +13.4% |

| VIC | $14,562 | -6.7% | +1.9% |

| TAS | $23,022 | +16.5% | +7.5% |

| SA | $7,890 | -11.0% | +7.7% |

| WA | $6,846 | -12.1% | +24.7% |

Australia’s most valuable farmland by State and region.

Tasmania – Northwest $28,827/ha

State median: $23,022ha

Victoria – South and West Gippsland $28,062/Ha

State median: $14,562ha

South Australia – Adelaide and Fleurieu $20,886/Ha

State median: $7,890ha

Western Australia – Southwest $17,236/Ha

State median: $6,846ha

Queensland – Southeast $16, 335/Ha

State median: $9,777ha

NSW – Hunter and North Coast $13,100/Ha (tied)

State median: $9,745ha

The tightening of the number of farmland transactions continued in the first half of 2024. Transaction volume plunged to a record low of 2,966, down 18.7% year-on-year and 4.8% below the second half of 2023, continuing a consistent fall in the number of transactions since a peak in the first half of 2021.

“Over the subsequent six half-yearly periods, transaction volume has fallen by 43% as fewer properties have been listed and have generally taken longer to sell,” Rural Bank said.

Australian farmland saw a reduction in annualised returns in the June quarter as capital growth slowed, however, income returns continued to show resilience.

The latest quarterly Australian Farmland Index from the Asian Association for Investors in Non-Listed Real Estate Vehicles showed income returns of 0.77% and capital growth of -0.28% led to a total return of 0.49% for the three-month period.