This article is from the Australian Property Journal archive

AUSTRALIA’S rapidly expanding build-to-rent (BTR) sector is expected to see 55,000 dedicated units completed by 2030.

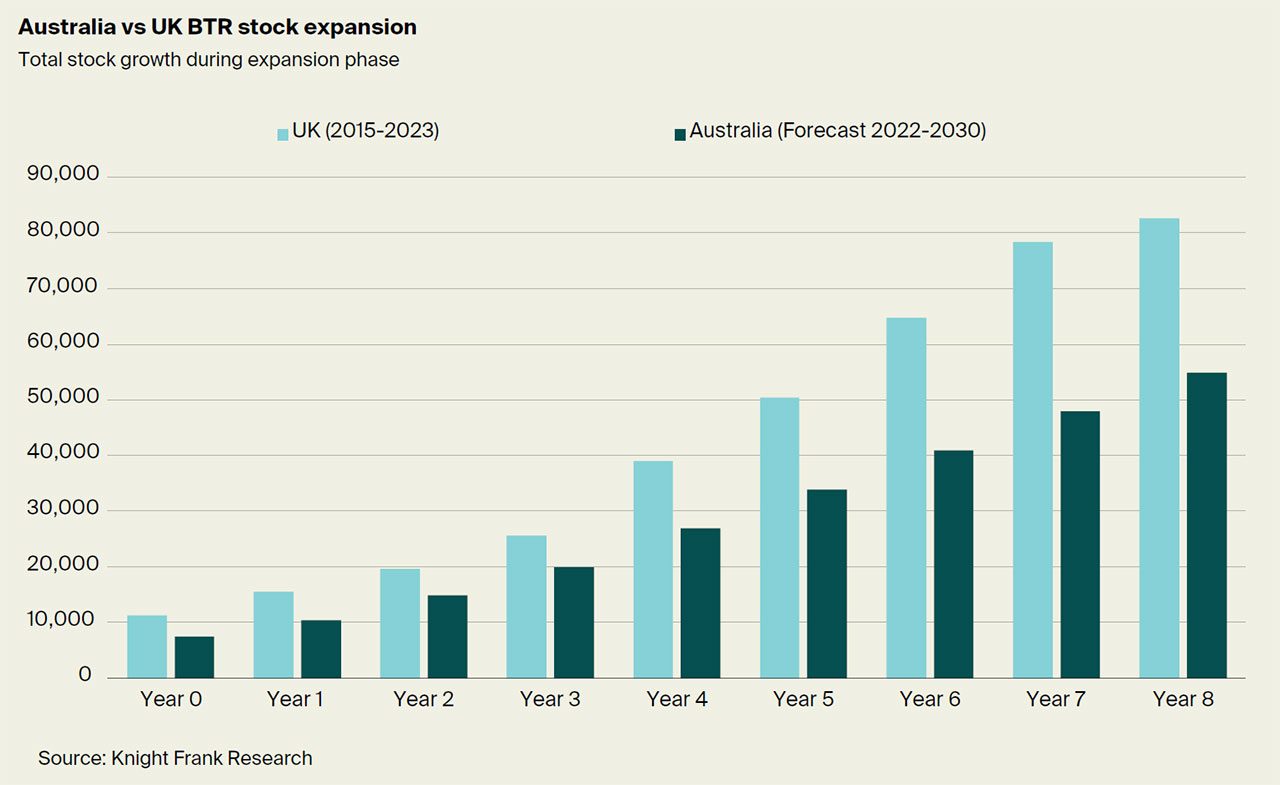

According to the latest research from Knight Frank, the forecasted figure is based on the current pipeline of developments along with the UK’s current BTR growth trajectory.

If BTR stock reaches this projected 55,000 mark, it would still represent just 1.5% of Australia’s rental supply.

“A wave of construction activity is now underway, with the pipeline is most advanced in Melbourne and Brisbane, but activity is picking up across all major cities,” said Ben Burston, report author and chief economist at Knight Frank.

“The current groundswell of activity points to a sustained expansion in total stock, and by 2030 BTR is expected to have emerged as a critical part of the housing supply mix, with Australia set to mimic the UK’s BTR journey over the past decade.”

Currently, Australia has an estimated 8,350 dedicated BTR apartments under construction and a further 12,900 units approved for development in the near term.

“The acceleration in development that we have seen in Australia in 2023 mirrors the beginning of the expansion phase that occurred in the UK from 2015 onwards,” added Burston.

“Over the following eight years to 2023, total UK stock has expanded from 11,312 to 82,636 units, reflecting average growth in the total stock of BTR units of 30 per cent per year, or 9,450 units.”

Knight Frank’s forecasted figure of 55,000 units suggests an annual delivery of 5,900 units from 2024 onwards.

Burston noted this volume would be a slower acceleration than seen in the UK in terms of annual unit delivery.

The BTR market in Australia has been held back by a combination of cyclical and structural supply challenges.

“However, many of these constraints have either abated or been removed and the sector appears set to expand rapidly over the next decade,” said Burston.

“Given the size of the market for rental accommodation, investors and developers are able to access a market offering the potential for large-scale capital deployment, while the community stands to benefit from a much-needed additional source of supply to help address Australia’s structural undersupply of housing.”

The report found investors on a global scale were looking for increased exposure to alternative sectors, including residential sectors led by BTR.

“For the first time, residential is the most sought-after sector for global investors targeting the Asia Pacific region, and Sydney and Melbourne are the preferred locations. Investors are gravitating toward the residential sector partly because of its defensive characteristics, specifically the ability to adjust rental income streams more quickly than other sectors in response to inflation,” said Tim Holtsbaum, head of Knight Frank.

“They are also assured by the relative resilience of residential rental performance during market downturns, with rents rarely falling in any major city.”

“Investors are seeking out resilient markets with long-term growth potential and the lack of an established BTR sector in Australia presents an opportunity to deploy capital into build-to-core strategies with the ability to achieve significant scale over time.”

In Australia, Melbourne is currently leading the nation in BTR developments with 4,920 apartments under construction and a further 8,250 approved for development.

Brisbane follows with 1,743 under construction and 2,567 approved for development, while Sydney has 1,529 under construction and 965 units approved.

Development are also typically one- and two-bedroom units, representing 36% and 44% of all units respectively.

“While many think the market is largely confined to Melbourne and Sydney, cities like Perth and Canberra also seeing signs of growing interest, partly owing to relatively low land values and strong rental yields,” added Holtsbaum.

“Inner fringe locations in Melbourne, Brisbane and Sydney are natural candidates for the first wave of schemes, given their offer of amenity, close proximity to CBDs and a high proportion of potential tenants given their comparatively well-educated and young populations.

“But over time we expect to see a broadening of developer interest to encompass middle-ring suburbs with high levels of amenity and connectivity.”