This article is from the Australian Property Journal archive

DESPITE some recent high profile deals, shopping centre transactions continue to meander along, with a shrinking demand for assets and the gap between buyers and seller expectations the likely reasons, despite an influx of assets being put to the market.

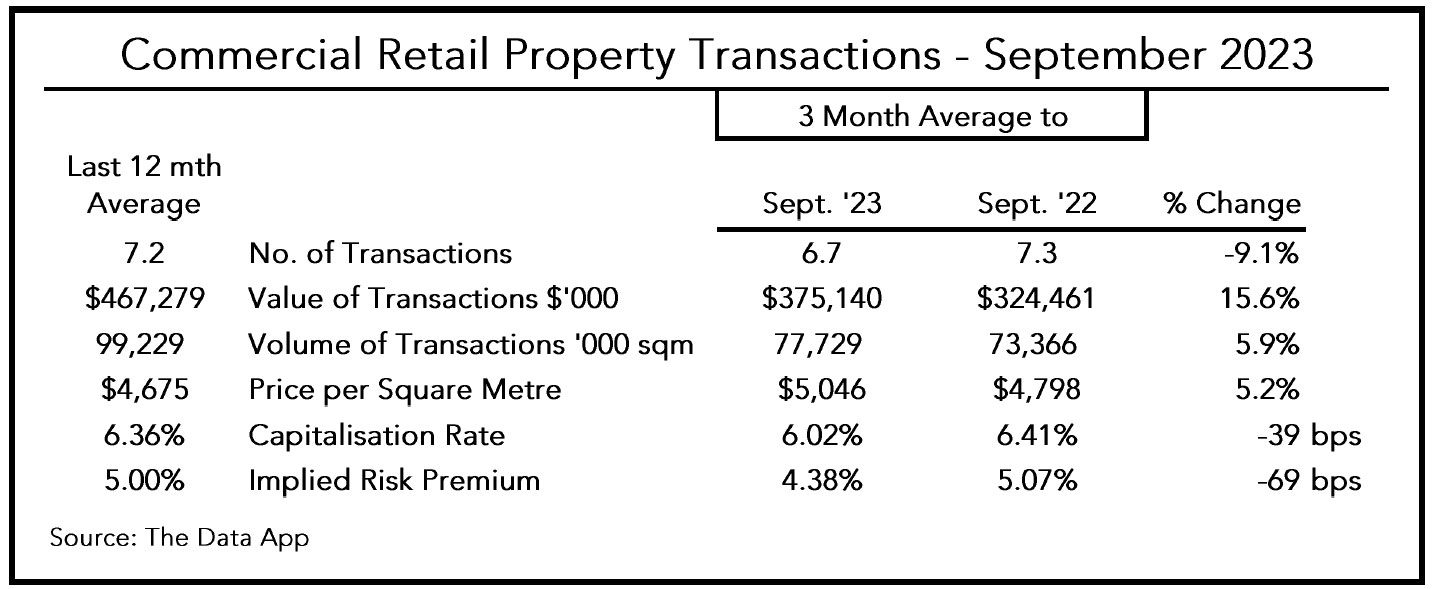

The latest numbers from The Data App show the number of transactions per month in the three months to September was 6.7, down from 7.3 a year earlier and below the 12-month average of 7.2.

However, the total value of deals lifted 15.6% annually to $375.1 million – albeit below the 12-month average of $467.2 million.

Volume of transactions per sqm and price per sqm are 5.9% and 5.2% higher respectively year-on-year.

The Data App estimates shopping centre cap rates are slightly lower than a year earlier, although, given the small amount of transactions and domination of small retail assets, this makes the accuracy of cap rates problematic, according to The Data App director Rob Ellis.

Of the deals that did go through, capitalisation rates were down 39 basis points year-on-year to 6.02%.

Ellis said that “clearly, with an ample supply of shopping centre assets on the market, the lack of transactions is primarily due to a lack of buyer interest”, giving two reasons.

“Firstly, the demand for assets has shrunk. With little appetite presently from the AREITs to acquire shopping centres in general and large centres in particular, the prime source of demand is likely to come from either overseas, primarily sovereign, funds or syndicates.

“This source, in turn, is increasingly constrained by the increase in the cost of capital.

“Secondly, is the price at which property holders are willing to divest assets.” The Dapa App estimates cap increased by a shade off 80 basis points to a shade under 7%. In comparison, the weighted cap rate of all the AREIT shopping centre assets reported was an increase of 24 basis points to 5.3%.

“To increase the attractiveness of retail assets to investors, cap rates clearly need to rise. This is particularly the case for larger retail assets, which are beyond the reach of most retail investors and therefore need to attract syndicated or overseas funds,” Ellis said.

He added that the recent decline in cap rates, due to the domination of small centres being sold, also means the implied shopping centre risk premium is “some way” below its long-run average.

“Without taking any view of the outlook, the risk premium would also suggest cap rates need to rise to increase by around 155 basis points to bring the attractiveness of shopping centres back to their long-run trend.”

Ample supply

Property fund manager ISPT this week put four landmark retail assets to the market week, including the Melbourne CBD’s GPO building and The Strand Melbourne – it’s expecting $180 million from the pair – as well as Halls Head Central in Western Australia and Eastgate Bondi Junction in Sydney

In the three months to September there was 400,000 sqm of shopping centres placed to the market, with 160,000 sqm transacting – suggesting nearly 250,000 sqm of overhang.

Singaporean sovereign wealth fund GIC is seeking a purchaser for its half-interest in north Perth’s Whitford City, with hopes of $250 million, while the triple-supermarket anchored Waverley Gardens Shopping Centre is on the market with a book value of about $218 million, and AMP Capital Shopping Centre Fund is divesting a 50% stake in Adelaide’s Westfield Tea Tree Plaza with expectations of about $350 million.

Recent deals to have come through include Aware Super’s property investment platform and real estate partner Barings acquiring a newly completed Coles and build-to-rent development in Canberra for $157.5 million, and HomeCo Daily Needs REIT offloading HomeCo Midland in Perth to investor and developer PWD for $75 million in what is the biggest large-format retail transaction since late last year.

Prior to that, Hong Kong private investment firm PAG snapped up Midland Gate for a discounted price of $465 million, in Perth’s first major regional shopping centre sale this year, from the Vicinity Retail Partnership and from the Commonwealth Bank Group Super.

In a recent APJ Talking Property podcast, MSCI Pacific head of real estate research Benjamin Martin-Henry discussed transaction volumes hitting the lowest level since 2011 with sales of industrial, office and retail assets all slumping in the first half.