This article is from the Australian Property Journal archive

GROSS effective rents across the major eastern seaboard CBD office markets fell in the June quarter, as landlords adjusted their expectations in response to the COVID-19 lockdown and proved more willing to give higher incentives.

Cushman & Wakefield’s quarterly Office Marketbeat showed face rents in the major east coast CBD office locations remained steady.

During the quarter, Sydney CBD prime gross effective rents fell 8.6% from $1,075 per sqm to $984 per sqm, while average incentives jumped from 21% to 27%.

Following a softer Sydney leasing market during the lockdown period in April and May, Cushman & Wakefield reported an almost 400% month-on-month increase in leasing inquiries in June.

“With the onset of COVID and the introduction of lockdown measures, most Sydney tenants seeking office space re-evaluated their timelines. However, we have seen a substantial uplift in new leasing inquiry levels in June as the NSW economy re-opens,” Tim Courtnall, head of NSW office leasing, Cushman & Wakefield said.

“The pandemic has also boosted the relative attraction of metro and city fringe markets such as Parramatta, South Sydney and North Sydney. These markets are benefiting from rising incentives in line with the CBD and significantly lower rents which appeals to tenants that may be looking to lower costs or adopt decentralisation strategies.”

Gross incentives across the A grade, B grade and premium grade markets all lifted over the quarter, to similar levels of 27%, 26% and 27%.

B grade gross effective rents averaged $780 per sqm, down by 8.5% through the June quarter.

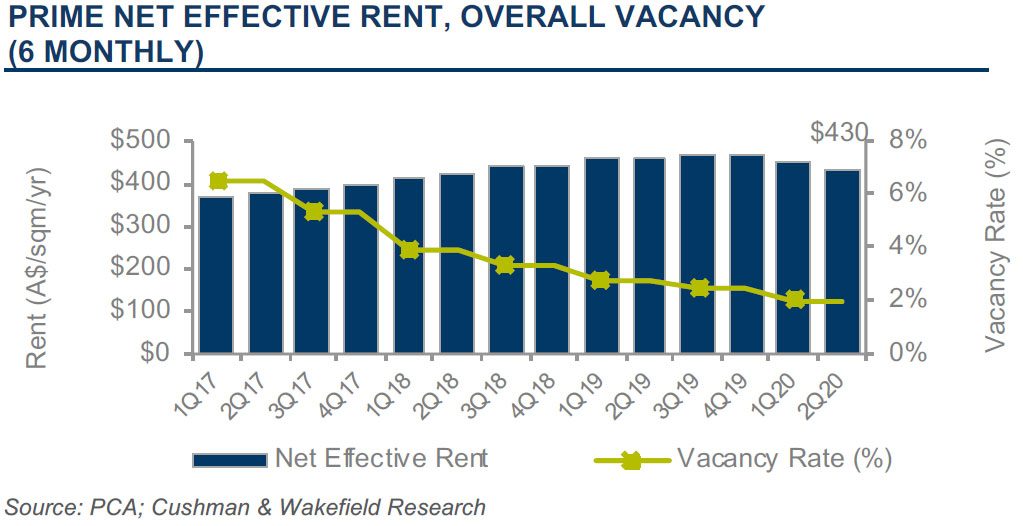

Prime net effective rents in the Melbourne CBD fell 5.4% from $454 to $430 per sqm, with incentives climbing from 29% to 33%, and no change to face rents. Incentives are now 27% higher than a year ago, as a large supply of new stock and a softer leasing environment put upward pressure on incentives.

Projects reaching or nearing completion include the Collins Arch and Olderfleet towers, close to each other on Collins St, as well as parts of the 80 Collins St precinct and Two Melbourne Quarter at opposite ends of the major thoroughfare, the Vic Police headquarters at 311 Spencer St, Charter Hall’s 130 Lonsdale St at Wesley Pl, 180 Flinders St.

Combined, those developments bring a total of about 333,000 sqm to the market, albeit 91% of which is pre committed.

Premium and A grade net effective rental growth in the CBD were negative for the second consecutive quarter, down to $510 to $470 per sqm and from $450 to $415 per sqm over six months respectively. B grade market net incentives lifted to 33%, and have lifted 26% in the 12 months to June, as face rental growth stalled over the quarter.

Brisbane’s CBD office market remained relatively unaffected by COVID-19 in the quarter. Prime gross effective rents slipped by just 1% to $470 per sqm, and incentives increased marginally to 37.1%, with unchanged face rents.

Cushman & Wakefield research shows declining CBD rents are generally tracking changes to the official unemployment data. Australian Bureau of Statistics data indicates a 7.5% decline in employment in New South Wales, 9% in Melbourne and 5.7% in Queensland between 14th March and 30th May.

“Face rents are holding up in all east coast CBD office markets, but landlords are adjusting their expectations amid ongoing market uncertainty. They are offering more attractive incentives to secure tenants over the longer term while occupiers adapt to the new realities of a more decentralised workforce,” Australian head of research, Cushman & Wakefield, John Sears, said.

“While activity is building as the economy re-opens, we expect CBD office leasing markets to remain subdued until economy growth gains pace and an effective vaccine is widely available.” Sears said.