This article is from the Australian Property Journal archive

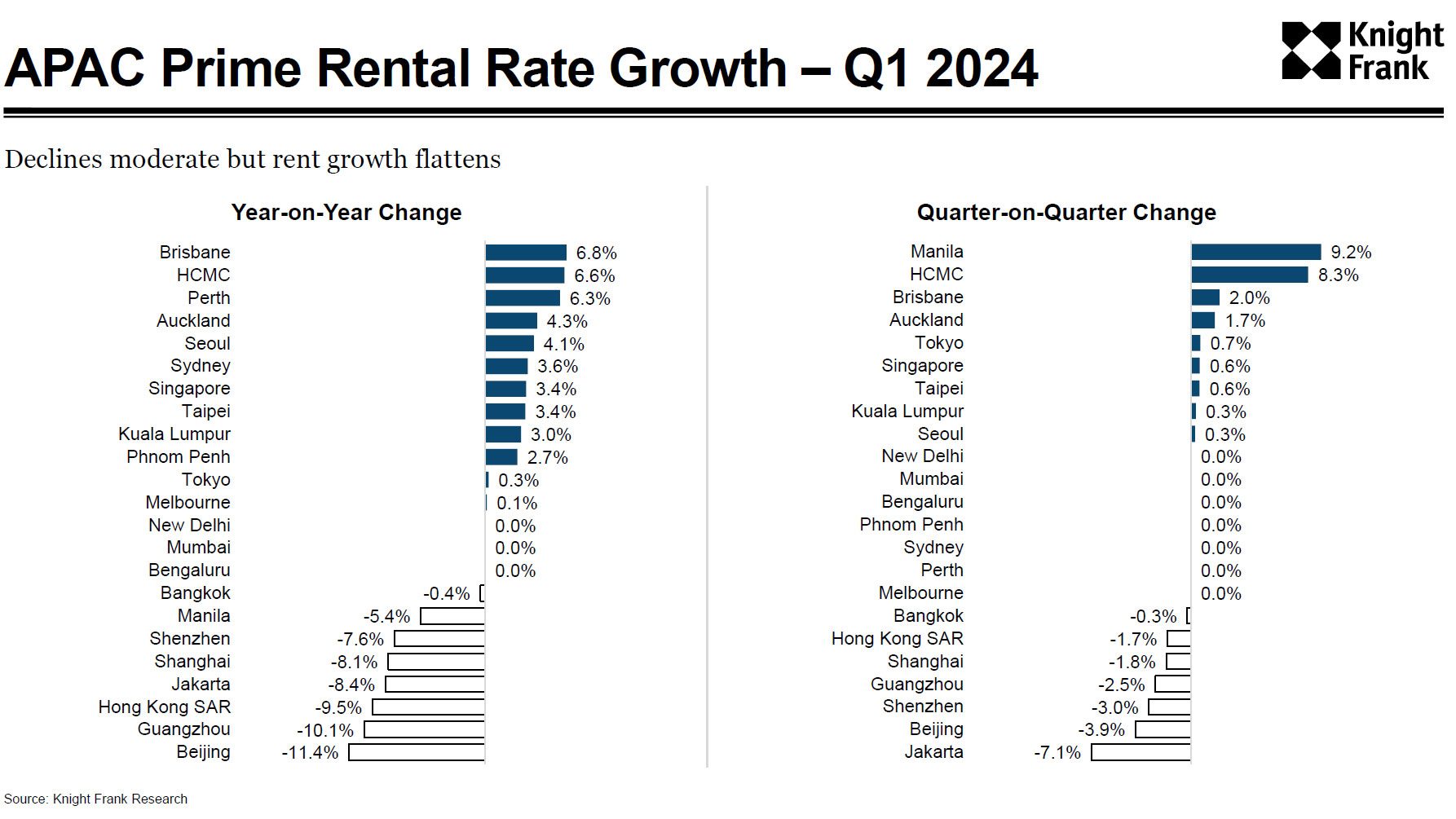

BRISBANE recorded the strongest office rental growth in the Asia Pacific over the 12 months to the end of March, according to Knight Frank, with more growth in store, while Perth came in third.

Knight Frank’s Asia-Pacific Prime Office Rental Index for the March quarter found Brisbane recorded rental growth of 6.8% over the 12-month period, the highest of all 23 cities tracked.

Ho Chi Minh City was next at 6.6%, while Perth came in third at 6.3%.

Of the other Oceania cities, Auckland recorded growth of 4.3%, followed by Sydney at 3.6% and, Melbourne which inched upwards by 0.1%.

Overall, the Asia-Pacific Prime Office Rental Index registered a 3.2% year-on-year decline, steeper than the 2.4% year-on-year fall in the December quarter. The seventh consecutive quarterly drop was largely driven by deepening rental declines in Chinese cities, which reached record lows during the quarter.

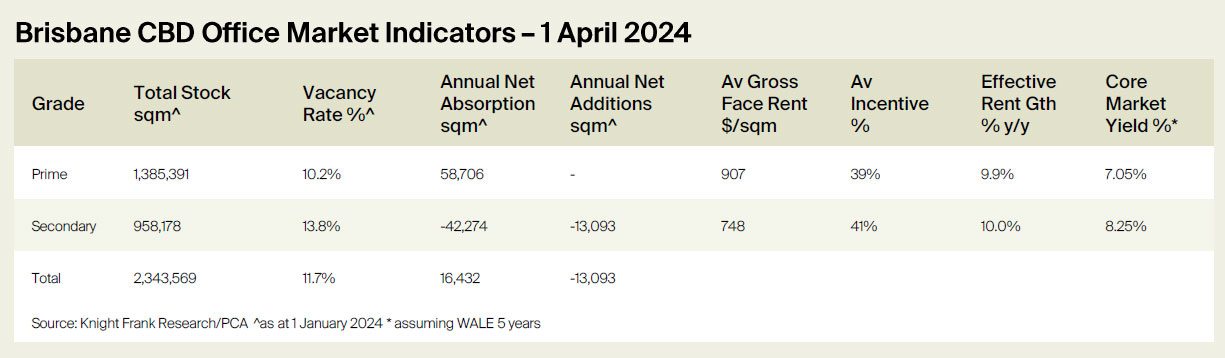

Meanwhile, Knight Frank’s Brisbane CBD Office Market showed average prime gross face rents increased by 6.3% to $907 per sqm in the 12 months to April.

Prime effective rents are forecast to grow by a further 5.7% over the remainder of 2024, and prime face rents are forecast to grow by an average of 6.1% in the five years from 2024 to 2028, Knight Frank projects.

Prime incentives now average 39%, shaved down from 40% six months earlier, and are predicted to fall to 38% over the next two years before plateauing.

Knight Frank partner, research and consulting Jennelle Wilson said demand for premium and upper A-grade space – or best-in-class assets – had continued to drive prime rental growth in Brisbane’s CBD office market.

“Conservatism due to slower economic growth and cost pressures is expected to moderate rental growth during 2025 before the inherent lack of new supply will see rents accelerate again from 2026 and 2028.”

Knight Frank is tipping the CBD’ s vacancy rate will fall to 9.7% by January 2025, down from 11.7% in January this year, due to a lack of supply coming online and ongoing tenant demand, before increasing again in response to new supply through 2025.

However, another period of low new supply between 2026 and 2028 will support vacancy falling again to below 9%, with the prime market to become very tight, particularly for contiguous space.

Knight Frank head of office leasing, Queensland Mark McCann said the Brisbane CBD office market had been supported by strong tenant demand over the past year, leading to significant rental growth.

“With no new prime supply since 2021 and more than a year before uncommitted new space is delivered, which is likely to be limited, larger tenants are increasingly commencing the process to secure their space well ahead of expiry due to supply constraints,” he said.

Tenant demand for the CBD has been broad-based over the past 12 months, although the professional, scientific and technical services and government sectors have been most active.

Recently, the state government has been the more active government tenant, but this is expected to switch to the federal government during 2024.

“The importance of the workplace to attract and retain staff plus maintain a dynamic and highly-attended office remains of key importance to both large and mid-tier tenants,” McCann said.

Brisbane’s office occupancy is currently averaging 83% of pre-COVID levels, according to CBRE, with that figure hitting 87% on peak days.

McCann said top and mid-tier professional firms are increasingly locking in future premises decisions and taking advantage of the relatively greater choice on offer now than there is expected to be in the next three years.