This article is from the Australian Property Journal archive

THE Purpose-Built Student Accommodation (PBSA) market will continue to experience strong demand driven by robust rental growth and a positive macroeconomic environment, despite government policy uncertainty around capping international student enrolments.

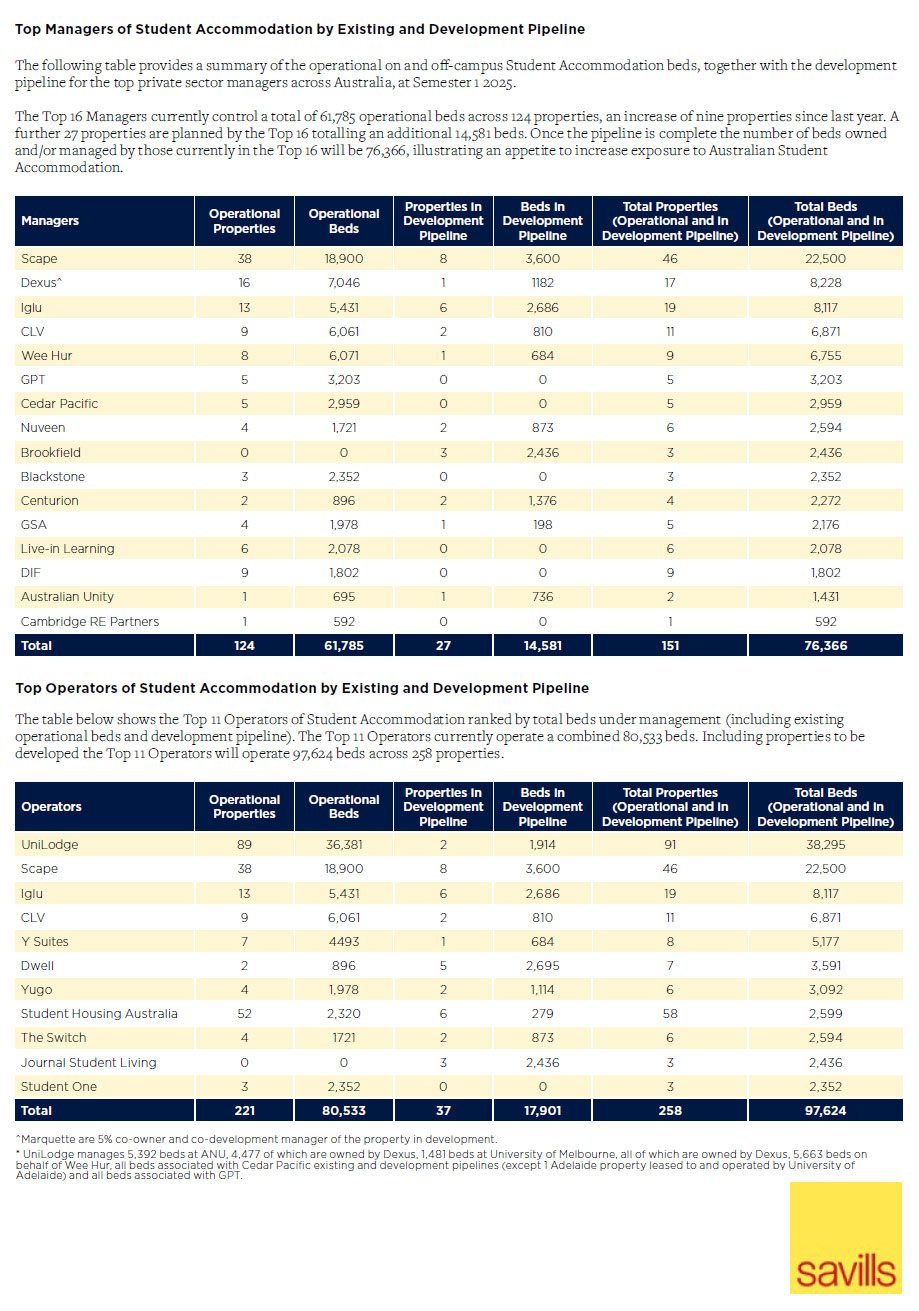

The latest Savills’ Student Accommodation 2024 Report reveals supply is growing in the PBSA sector, with 16 projects currently under construction across Australia’s major cities.

This is the highest number of active developments since the pandemic, signalling growing optimism among developers. Notably, Sydney is set to lead the charge, with over 4,300 new student beds slated for delivery over the next three years. Brisbane will follow suit, with more than 3,160 beds expected to be completed in time for the 2027 academic year.

Conal Newland, head of operational capital markets at Savills said while uncertainty around international student policies looms, demand for student accommodation will remain high.

“The global student accommodation sector is expected to recover in 2025, with investment levels increasing by 23% annually worldwide. In Australia, we anticipate strong demand continuing due to a positive macroeconomic environment, despite challenges posed by potential enrolment caps,” he added.

The recent political debate surrounding international student numbers has injected an element of unpredictability into the market. The Albanese government’s Education Services for Overseas Students Amendment (Quality and Integrity) Bill 2024 proposes to cap overseas student enrolments at 270,000.

Though the bill was ultimately rejected by the Coalition and the Greens, the threat of enrolment caps still looms, because the Coalition has promised even more deeper cuts, keeping developers and investors on edge.

In 2023, Australia’s net migration surged to 300,000, largely driven by an influx of international students, which some argue has exacerbated the housing crisis, putting pressure on the government to curb migration. However, industry experts argue that capping international student enrolments will not significantly ease the housing shortage.

The Student Accommodation Council’s report, Beyond the Visa Cap: Why Restricting International Students Won’t Solve Australia’s Housing Crisis, show the country’s 725,000 international students make up 5.4% of the rental market – and that capping their numbers will only reduce this figure by 0.6% by 2026, and have little impact on rental availability.

“The reality is that Australia’s housing crisis is a supply issue, not a demand issue. The private sector has been rapidly expanding PBSA stock in response to growing demand, but we are still undersupplied compared to markets like the UK,” said Newland.

Compared to the UK, Australia’s PBSA sector is heavily undersupplied due to decades of poor planning.

For comparison, Australia currently has only 132,700 beds in operation with 1.6 million students, whereas the UK market which has 1.3 million students, and there are over 700,000 PBSA beds in operation.

This type of kneejerk reaction by policymakers in Australia has seen the nation’s largest superannuation fund, AustralianSuper, preparing to launch in the United Kingdom PBSA sector.

The Savills report also highlights strong rental growth across Australia’s PBSA market, with rent increases across all major cities since 2022. Perth has seen the most significant rise, with student rents climbing by 19.7% annually, followed by Brisbane (16.1%), and Sydney (10.4%). These increases reflect high demand and low vacancy rates, with occupancy rates remaining consistently strong, even as operational costs climb.

“This rental growth has been crucial to maintaining developer and investor confidence, offsetting some of the feasibility challenges posed by rising construction, financing, and operational costs,” Newland noted.

Despite political uncertainty, global asset managers are betting on the long-term potential of Australia’s student accommodation sector. Recently, Nuveen, a major US investment firm, committed to a $275 million loan for a Brisbane PBSA project by Dexus and Marquette Properties, to repurpose an office building into a 1,200-bed student accommodation facility.

While rents are expected to slow over the next five years, Savills predicts that Sydney will remain the strongest performer, driven by new developments in key student hubs such as the Anzac Parade corridor and Macquarie Park. Additionally, Perth and Brisbane are set to receive their first new PBSA supply since 2022, offering fresh opportunities for both students and investors.

Meanwhile the report identified a key trend, the size of new PBSA developments is increasing, averaging 540 beds up from 498 in previous years.

Despite ongoing cost pressures, including a 23% annual increase in operational costs, the delivery of new PBSA beds continues, with over 12,000 beds expected to come online in the next three years.

Investor sentiment also remains positive, with a shift towards diversification in the Australian property market. According to Savills’ Investor Sentiment Survey, 58% of respondents indicated they plan to increase their exposure to student accommodation in the next two years. Notable players in the market, such as Scape, are expanding their portfolios, with the company set to manage up to 22,500 student beds following recent acquisitions.

Savills expects a significant increase in capital investment in the sector starting in 2025, which will further bolster investor confidence and market liquidity.

“While the current political climate presents challenges, the fundamentals of the PBSA market remain strong. The delivery of new assets in prime locations will continue to attract institutional capital,” said Paul Savitz, director of operational capital markets at Savills.

Despite the positive outlook, Savills cautions that the PBSA sector is not without its challenges. Increasing construction costs, rising interest rates, and potential regulatory changes could dampen the pace of new developments. Additionally, the Australian rental market is expected to experience a slowdown in rental growth over the next five years, as the market absorbs a wave of new supply.

“While the political environment may cause some short-term volatility, the long-term outlook for Australia’s PBSA sector remains positive. Developers and investors must remain focused on the fundamentals—such as strong occupancy rates, consistent rental growth, and an ongoing supply-demand imbalance in major student markets,” said Newland.