This article is from the Australian Property Journal archive

OFFICE and retail investment have roared back into fashion, while commercial property transactions across the country hit $43 billion over the first three quarters of this year, already eclipsing 2020’s full-year total and outpacing the pre-pandemic period.

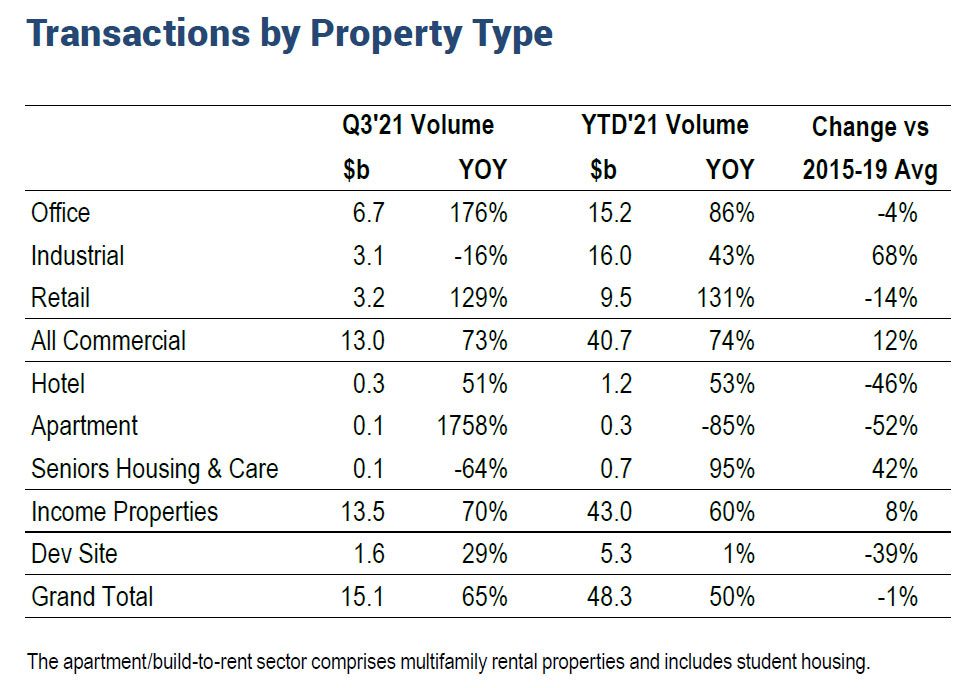

Real Capital Analytics’ latest Australia Capital Trends report showed Australian commercial property sales activity gathered pace in the September quarter to reach $13.5 billion, a 70% year-on-year jump over the subdued third quarter of 2020.

The year-to-date total is 60% higher than 2020 and 8% higher than the average in the five years before the pandemic. Nearly $7 billion worth of transactions are awaiting settlement, the fourth quarter is shaping up to follow historical trends for investment activity and 2021 is likely to go down as the year of the “megadeal” – including Australia’s largest-ever real estate transaction which saw Blackstone earlier this year sell the Milestone logistics portfolio of 45 assets to ESR and GIC for $3.8 billion.

For the first nine months of the year, sales of industrial properties surpassed those of offices for the first time in Real Capital Analytics records, at $16.0 billion. Also driving that figure was another Blackstone portfolio deal, a 90% stake in the Fife logistics portfolio selling for $850 million, while a Logos-led consortium picked up the Moorebank Logistics Park for $1.7 billion.

GPT has just spent $682 million acquiring the Ascot Capital logistics portfolio, comprising 23 warehouses weighted to the eastern seaboard, while The Australian has reported that Blackstone is in negotiations to take a 49% stake in the $3.5 billion Dexus Australian Logistics Trust.

Office investment volumes during the September quarter were buoyed by Lendlease’s $1.2 billion sale of Melbourne Quarter Tower to the National Pension Service of South Korea, and totalled $6.7 billion for a $15.2 billion year to date figure.

Sydney office sales have picked back after a record-low year in 2020 and the city has reclaimed its traditional position as the number one office market in Australia. Its third quarter was spearheaded by M&G Real Estate’s joint venture with Mirvac to acquire a 50% stake in the EY Centre at 200 George Street for $579 million.

“After a slow start to the year, the office sector is now flourishing. Volumes have eclipsed 2020 levels and are on par with pre-COVID averages as investors show renewed confidence in the sector,” Benjamin Martin-Henry, RCA’s head of analytics, Pacific said.

“Retail is also doing well, and we are starting to see larger shopping centres transact as investors look to make big plays for quality stock.”

Deal volumes in the retail sector reached $3.2 billion, buttressed by the closing of Myer Melbourne’s sale to the Charter Hall Long WALE REIT and Abacus, and Casey Central Shopping Centre selling to Haben and JY Group for $225 million.

While sales in the third quarter were muted, the year-to-date deal volume was 68% ahead of the pre-pandemic five-year average. Since the quarter’s close, Haben and JY Group have bought Wollongong Central from GPT for $402 million, while GPT is also offloading Casuarina Square in Darwin for $420 million, UniSuper and Cbus Property bought major stakes in AMP Capital’s Pacific Fair and Macquarie Centre malls for $2.2 billion in Australia’s largest-ever retail property transaction.

Meanwhile, RCA has already seen record years for childcare, pubs and self-storage assets, with what is traditionally the busiest quarter of the year still to go.

Blackstone this week locked away the Fort Knox Self Storage portfolio of 11 self-storage assets in Melbourne, in what it said is one of the largest transactions in the alternative asset class sector in Australia, soon after Abacus Property Group went on a self-storage buying spree, snapping up 22 facilities for $370 million,

It follows record volumes in 2020 for data centres, student accommodation, services stations and medical offices all registered record annual deal volume.