This article is from the Australian Property Journal archive

INDUSTRIAL and logistics space is expected to attract greater demand and rental growth over the second half of 2024 and into the new year.

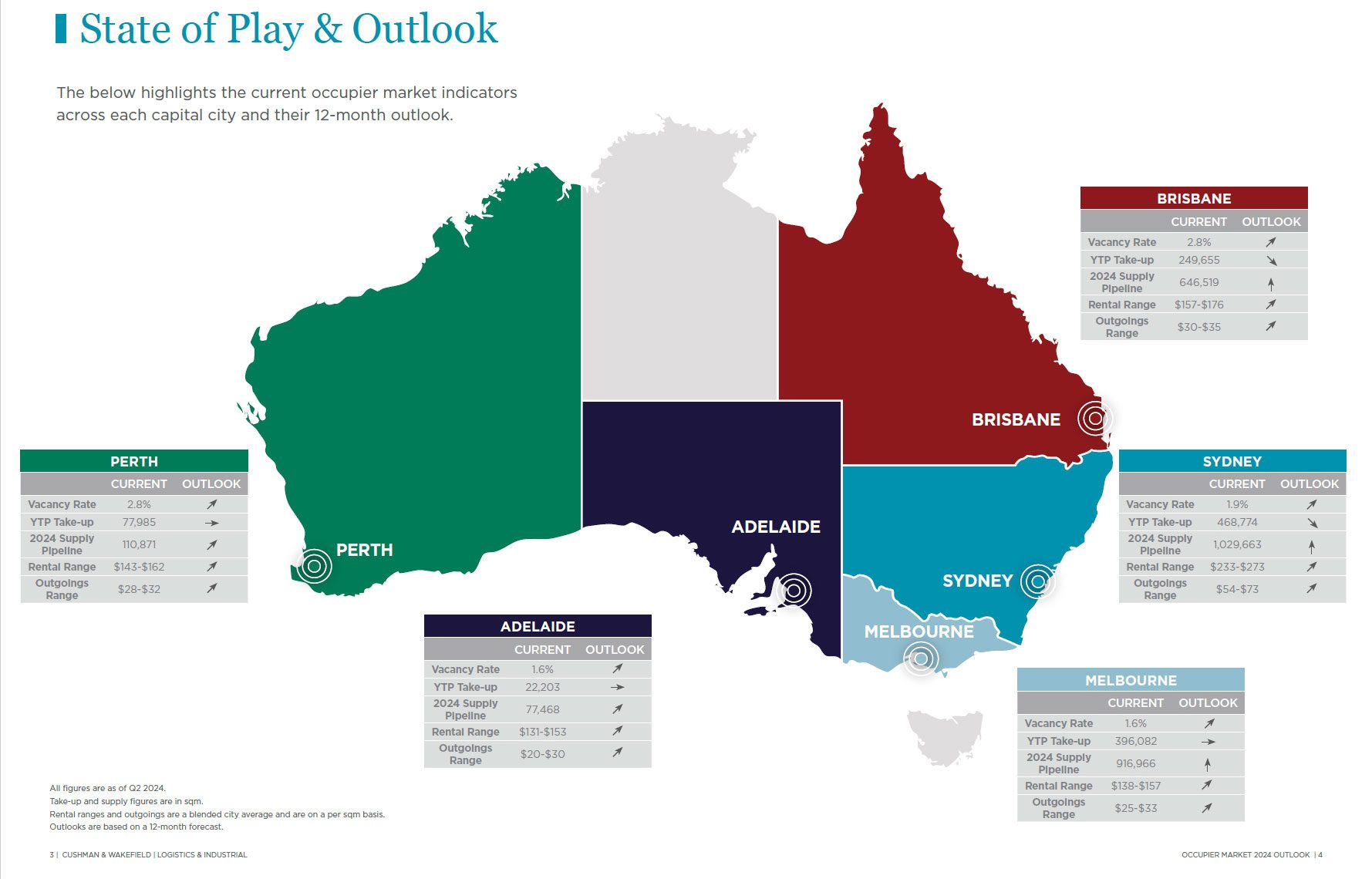

According to Cushman & Wakefield’s Logistics & Industrial (L&I) Occupier Market 2024 Outlook, key precincts will see surging occupier demand as tenants try to keep supply chain costs under control.

Though industrial rental growth has softened from its 1H 2024 peak, rents are still anticipated to be higher than historical averages, with an expected 6% growth for 2024 and 5% for 2025.

Since the onset of the COVID-19 pandemic, industrial and logistics rents have grown by nearly 70% but Cushman & Wakefield’s research found rents typically remain a small cost compared to more expensive costs like transport.

As a result, looking at rent on a population reach basis instead of a traditional per sqm basis reveals how much rent an occupier will pay to service their customer catchment.

“When measuring rent paid per 100,000 people within a 30-minute drive, higher rent in inner and central markets is offset by significant supply chain savings, given reduced transport costs and a larger addressable population,” read the research.

“For example, rents in South Sydney are $12.90 per 100,000 residents, representing a 40%+ discount to select non-infill markets in Sydney. South Sydney can service a much larger population in a 30-minute drive compared to a non-infill market despite having the highest gross rents in the country.”

Luke Crawford, head of logistics & industrial research at Cushman & Wakefield, Australia noted that this data won’t be as useful to businesses that don’t deliver to their customers but estimates in excess of 50% of the demand pool does deliver business to customer (B2C).

“When an occupier assesses optimal customer fulfilment locations, in most cases, access to population outweighs higher rents given the cost savings it can provide in other parts of the supply chain,” said Crawford.

“Occupiers recognise there isn’t a one-size-fits-all solution, and are also exploring strategies to reduce real estate expenses through warehouse consolidation and efficiency and drive operational savings.”

Rental growth is varied at a submarket level in the long-term, with four of the 25 submarkets expected to see prime rental growth of more than 25% in the next five-years.

This includes Sydney’s Central West and Brisbane’s Trade Coast as the top performing submarkets at 29.0% and 27.8% growth respectively.

Demand has also dropped off from peak levels, with gross take-up of 3-3.2 million sqm expected for the year and 3.5-3.7 million sqm in 2025.

“While lease deals are taking longer to execute in the current environment, our current enquiry data shows there are over two million square metres of active tenant briefs in the market. That underscoring healthy underlying demand to meet the anticipated increase in supply over the next 12 months,” said David Hall, national director and head of brokerage, logistics & industrial at Cushman & Wakefield, ANZ.

“As elevated rents become the norm, occupiers are becoming more focused on strategies to mitigate costs, including automation and technology to streamline operations and servicing from other city and regional facilities if feasible. For well-capitalised occupiers, asset acquisitions to stabilise long-term cost structures is another option gaining momentum.”