This article is from the Australian Property Journal archive

HIGH mortgage rates and soaring prices has driven housing affordability to its worst level on record, as Australians work overtime, take on second jobs, and even skip on healthcare costs in a bid to break into the heated market – and there is a growing divide in the market between those with family money and those without.

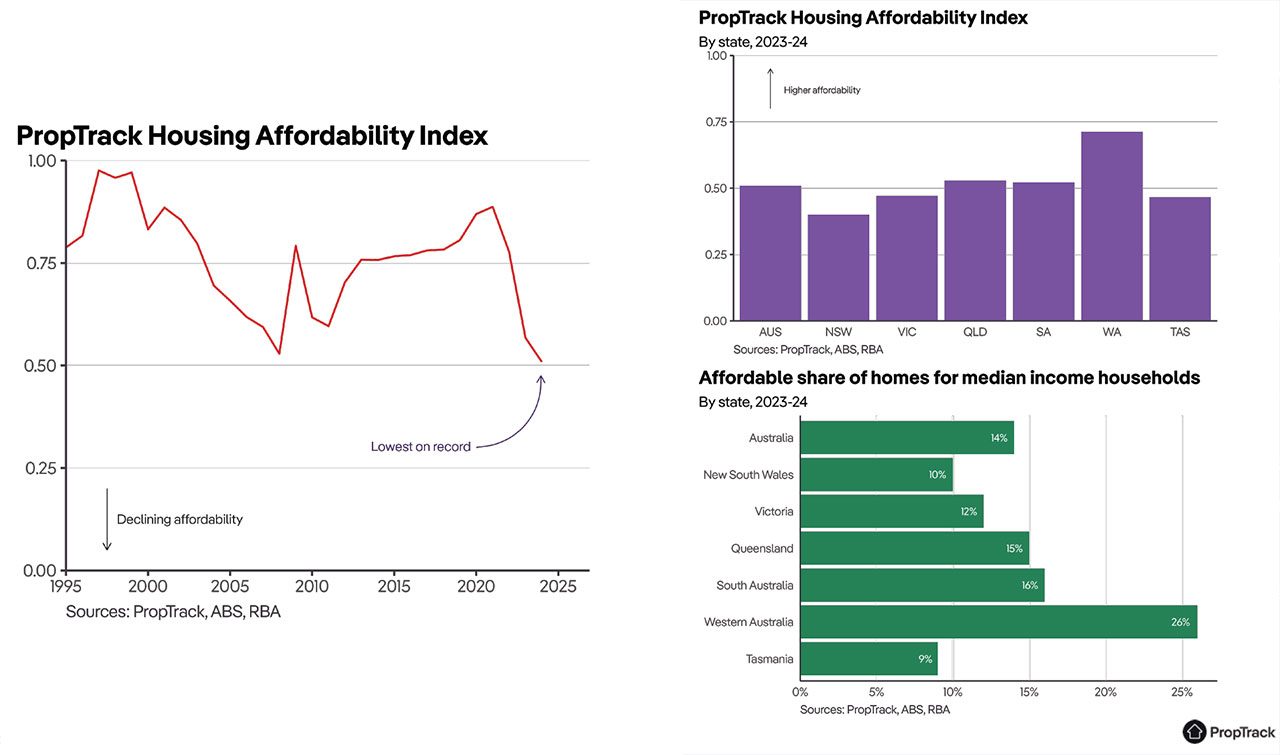

PropTrack’s new Housing Affordability Report showed that housing affordability deteriorated over the past year, and that a median-income household earning around $112,000 could afford just 14% of homes sold in the 2024 financial year – the smallest share of homes since records began in 1995.

This share has declined from 43% in just three years.

Low-income households have effectively been locked out of the market. A household earning $50,000 per year is able to afford just 3% of homes.

According to the report, an “unwelcome trend” is the increasing role of family wealth in determining both which Australians can buy a home, as well as when they can access the market.

“The outcome is that people who can buy either already have existing housing equity, so people who are upgrading and are benefiting from this home price growth we’ve seen over the past few years, or have family money, or they are part of the third of first-time buyers over the past year use the government’s home guarantee scheme, because saving a deposit at the moment is extremely tough,” PropTrack senior economist and report co-author Paul Ryan told Australian Property Journal.

“Within just a generation, we’ve gone from a period in the late 1990s where a typical household could afford to buy just with income half of all homes across the country, and the fact that that’s fallen so dramatically, but yet we still have more than half a million homes transacted over the past year, I think tells us quite a shocking story about who now is able to access the market,” he said.

“More and more, how much wealth you have matters for being able to crack into home ownership in a way that just a generation ago, it wasn’t the case.”

An average income household would need to save 20% of their income for more than five and a half years to save a 20% deposit on a median-priced home. NSW remains the state with the highest deposit hurdles – despite higher incomes, it takes around 6.5 years to save a deposit.

Affordability is worst in NSW, where a median income household can afford just 10% of homes sold in the states, and mortgage costs are at a nation-high. Tasmania and Victoria follow.

South Australia recorded the biggest decline in affordability over the past year. A median-income household was able to afford just 16% of homes sold FY24, down from almost half (49%) just three years earlier.

A median-income renting household could afford just 11% of homes sold over the past year. In comparison, a median household with a mortgage could afford 34% of homes sold over the past year.

Mortgage costs are as high as seen in 2008 and only just below the historical peaks reached in 1989-1990. An average income household would need to spend a third of their income on mortgage repayments to buy a median-priced home.

Meanwhile, Helia’s 2024 Home Buyer Sentiment Report, which surveyed over 3,000 aspiring home buyers, showed that cost of living (54%) has for the first time, surpassed housing affordability (43%) as the key barrier to entering home ownership.

Home buyers are making significant efforts to save for a 20% deposit. Nearly a third (31%) of home buyers have taken on overtime work, and almost a quarter (23%) have pursued secondary jobs. Additionally, they are cutting back on non-essentials, including takeaway coffee and food (48% and 44% respectively), hobbies (41%) and subscription services (34%). Concerningly, one in five (21%) are reducing their spending on health to achieve home ownership.

“Hopeful” for housing affordability improvement

“I think we’re hopeful that affordability will get a big bounce from lower mortgage rates,” Ryan told Australian Property Journal.

Markets have priced in about a one percentage point drop in the cash rate over the next 12 months or so.

“That will make a big difference to how many households on different income levels can afford. We’re not going to get back to the situation three years ago, when a median income household could afford 43% of homes. We’re not going to get back to that level because we’re not going to get back to interest rates at the level that we saw during the pandemic. Those were emergency levels of mortgage rates.

“In the short run, hopefully some relief.

“In the long run, hopefully we see more action towards arresting that decline in affordability and tipping it the other way with more housing. Government policies such as the National Housing Accord – recognising that the solutions to these housing affordability concerns are increasing housing supply – have been a very good development”

“These are changes that actually can have a meaningful impact. We’re talking about changes for the next decade.”

Ryan said the positives from overseas examples are that “changes can occur quicker than people expect”. He pointed to the Auckland upzoning 2016 that reduced restrictions on housing development and said that price growth there has “come to a halt”, there has been meaningful impacts on housing construction, and affordability conditions have improved.