This article is from the Australian Property Journal archive

AUSTRALIA’S industrial & logistics vacancy rate remains the lowest globally despite recording a boost in supply across most markets in the first half.

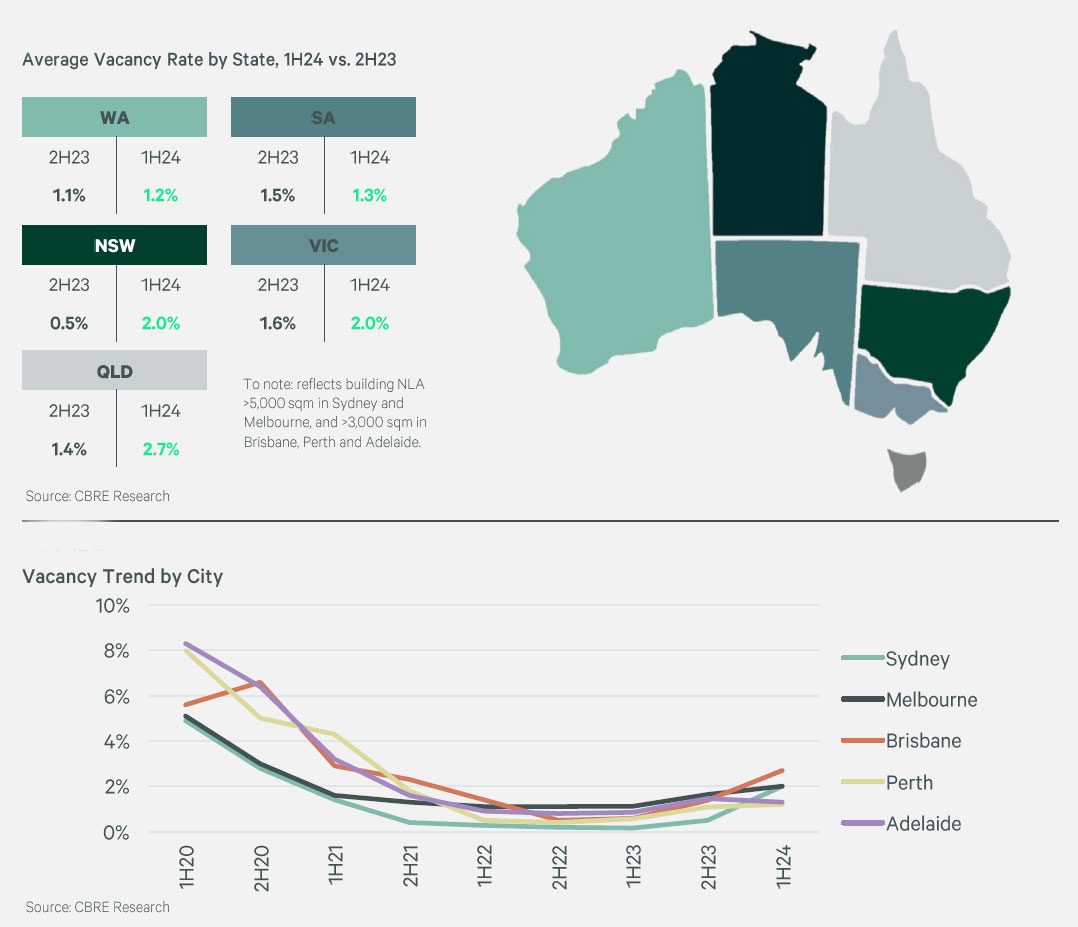

According to CBRE’s H1 2024 Australia’s Industrial and Logistics Vacancy report, revealed Australia to hold the lowest rate at 1.9%, with Perth the lowest in the country at 1.2%.

“We are witnessing a rise in the vacancy rate across most cities, as demand normalises, and greater sub-lease space is being added to the market,” said Sass Jalili, head of industrial & logistics research at CBRE.

“Despite the rise in space availability, we still do not expect to see the national average vacancy rate surpass 4% in 2024.”

While overall vacancy rates remain below 2%, the first half saw uplifts in Sydney, Brisbane and Melbourne.

Sydney vacancy levels were up over the half from 0.5% to 2%, mainly thanks to boosts in the outer western markets.

Melbourne’s vacancy rate also increased to 2%, with lifts across most precincts excluding the western precinct, which holds the highest rate but saw a marginal drop over the half.

Brisbane’s industrial & logistics market recorded the highest vacancy rate in the country at an average of 2.7%.

Meanwhile, after Perth’s 1.2%, Adelaide has the lowest rate at 1.3% and was the only market to see a decline.

National net absorption has dropped to its lowest level on record with the most significant falls seen across the eastern cities.

Melbourne’s net absorption levels fell over the quarter by remain the strongest in the country, with Brisbane seeing a drop by more than 50%, while Perth and Adelaide both recorded increases.

Over the half, gross take-up of floorspace reached 0.9 million sqm, with just 50% of take-up made up of tenants expanding as occupier demand moderates.

“Sub-lease activity has multiplied across the market but has not significantly affected the vacancy rate. Over the past six months sub-lease activity has been most prominent in the Sydney market, accounting for 50% of vacant floorspace,” added Jalili.

“[In Melbourne] sub-leasing has remained steady with minimal options available in the North and South East, and circa 140,000 sqm of sub-lease space available in the West. With uncertain global politics and speculation around interest rates we expect to see continued subdued occupier demand throughout the remainder of 2024.”

Perth’s sub-lease space represents just 13% of the total space vacant and is only significant in the East and South precincts.

In Brisbane, sub-lease space represents just around 16% of total vacant area in the Brisbane industrial & logistics market.

“Over Q1 2024 transaction activity was slow, but that is not surprising given the incredible rental growth of previous years owing to low vacancy,” said Michael O’Neill, regional director of industrial & logistics at CBRE.

“High prevailing rents, softening consumer demand, higher outgoings, and reduced sense of urgency all contributed to a slower start for all markets. This has resulted in vacancy approaching or exceeding 2% in nearly all markets. Overall, we’re seeing the market begin to normalise to pre pandemic conditions.”

Meanwhile, rental growth has continued to moderate over the last 12 months, as the current year-on-year growth rate for national super prime grade face rents is 12%.

With rental growth still forecast for further construction over the remainder of 2024.