This article is from the Australian Property Journal archive

VICTORIAN residential lot sales have dropped to their lowest quarterly total in two years, as the market inevitably slows after record levels of growth.

According to new analysis from RPM Research and Data, beyond just stabilisation the state’s greenfield land market also experienced a slowdown in Q2 as a result of inflation, high construction costs and rising interest rates.

“Many buyers have been forced to re-assess their borrowing capacity and re-evaluate their buying decisions in light of interest rate rises, including the most recent 0.5 per cent increase in the cash rate to 1.85 per cent,” said Luke Kelly, managing director of project marketing at RPM.

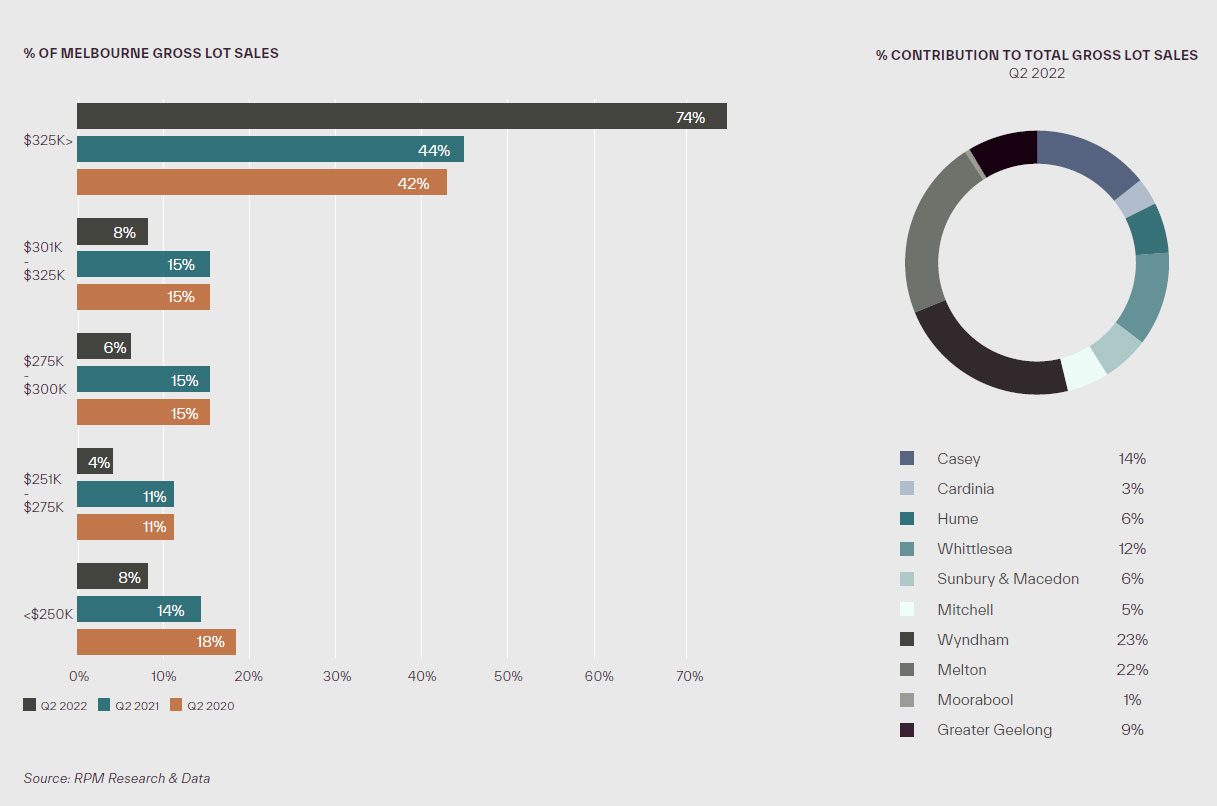

On a rolling 12-month basis, Victoria saw around 25,950 vacant lot sales and 4,856 in quarter two alone, representing a yearly decline of 41% and a quarterly drop of 14%.

“At the same time, they’re facing increasing residential construction costs, rising living expenses fuelled by inflation and higher home loan repayments,” said Kelly.

“This is leading to a subdued market in the coming months, with a number of prospective buyers deciding to sit on the sidelines as a result of the uncertain climate, resulting in declining month-on-month sales activity.”

Lot prices continued to grow over the period, increasing by 3.6% for the quarter and 9.6% for the year to $379,000, at the same time as median lot sizes reached 366sqm, a record low.

Kelly noted that the new home market is shifting to meet challenges of affordability in the market, with more offerings of townhouses, small lot houses and smaller lots.

“We have already seen this represented in sales activity for the second quarter, with new releases incorporating smaller lot sizes in their offering and accounting for more than two thirds of sales,” he added.

“This will help to buttress the fall in vacant lot sales heading into the second half of 2022.”

Kelly anticipates sound market fundamentals and changing product offerings by developers will result in this slowdown being limited to the short-term.

“We’re seeing developers invest in new premium greenfield sites for affordable lifestyle communities as they position themselves for the recovery,” said Kelly.

Victoria’s Western Growth Corridor maintained its dominant position across quarter two, accounting for 45% of sales in growth corridors, even with sales dropping 9% to 2,049 gross lot sales. It also saw its median lot price grow by 6.1% to $381,000.

The Northern Growth Corridor saw the slightest decline in sales, down 7% to 1,297 lot sales.

While the corridor did see a 13% boost to supply, contributing to a market share increase to 29%, a six year high. Lots also saw a 2% increase in price to $353,000.

Gross sales in the South East Corridor were at just 800 lots, down 24%, with new supply down 4% for a total share of 18%. While still being the least affordable, with the median lot price in Casey and Cardinia above $400,000.

Finally, the Geelong Growth Corridor saw the sharpest fall, dropping 32% for the quarter and 63% for the year to 388 gross lot sales, representing 9% of all vacant land activity.

The Geelong Growth Corridor also saw a fall of 0.5% in median lot sale price to $380,000, indicating the peak has already passed in this market.

Meanwhile, the englobo market transactions were stable throughout Q2, with deals ranging between $10 million and $40 million keeping the market afloat.

With RPM’s managing director of transactions and advisory, Christian Ranieri, noting that typically speaking the englobo sector is cut off from forces impacting the larger market.

“Greenfield development sites, particularly around Melbourne, are scarce and developers need to buy sites even during downturns to ensure they have a pipeline,” said Ranieri.

“These factors, including the continued strength of the industrial market, recently dubbed the tightest market in the world, mean the englobo sector won’t see the same downturn as the residential land market.”