This article is from the Australian Property Journal archive

PROFIT-making sales and number of transactions continued to grow across the December quarter, as the property market picks up momentum.

According to CoreLogic’s latest Pain & Gain report, that looked around 90,00 resales over the last quarter of 2023, 94% of transaction in the Australian property market recorded a nominal gain.

The median gross profit was also up over the quarter, hitting $310,000, with all three metrics up on the previous period.

“The improvement in the key metrics of this report really highlight the improving profitability in the housing market since the recovery trend began in early 2023,” said Eliza Owen, head of research at CoreLogic.

Loss-making resales were down to 6.0% in the quarter, to a median of $40,000. With the volume of loss-making sales also down 5.1% on the previous quarter.

“We’ve observed a decline in the number of loss-making sales, which fell to just 5,500 during the December quarter, even as overall transaction volumes increased,” added Owen.

“The broad-based increase in profitability and value across the Australian housing market helps to shore up financial stability at a time of stark increases in mortgage costs for some households.”

Over the quarter, the total nominal profit from resales reached $29.9 billion, up from $28.7 billion in the previous quarter.

The portion of resales within a two-year hold period reduced from 7.9% in the September quarter to 7.5%, indicating a minor easing in short-term loss-making resale conditions.

Though there was also an increase in resales with a hold period between two and four years, from 13.3% in the September quarter to 14.0%.

“This change reflects homes that were bought in 2020 and 2021, and it turned out to be the most popular timeframe for reselling properties in the quarter,” said Owen.

“While some of these sales might have been influenced by a rise in mortgage rates, it’s interesting to note that only 3.7% of homes sold during this timeframe ended up making a nominal loss.”

Adelaide was the most profitable capital city market for the fifth consecutive quarter, with more than 98% of resales making a nominal gain.

The Perth market also recorded improvement with the rate of loss-making sales reducing to 8.4%, marking its most profitable period since July 2015.

In terms of profitability, regional markets outperformed capital cities over the quarter with 95.5% of resales in regional areas seeing nominal gain, compared to 93.2% in combined capitals.

Regional markets also saw a more rapid increase in profitability.

“Due to the lingering value add of the COVID-boom, regional markets are looking more profitable than capital cities,” added Owen.

“Regional markets typically have lower property prices and a different lifestyle appeal and are outperforming capital cities in terms of profitability potentially due to sustained demand, limited housing supply, and a more favourable cost of living environment.”

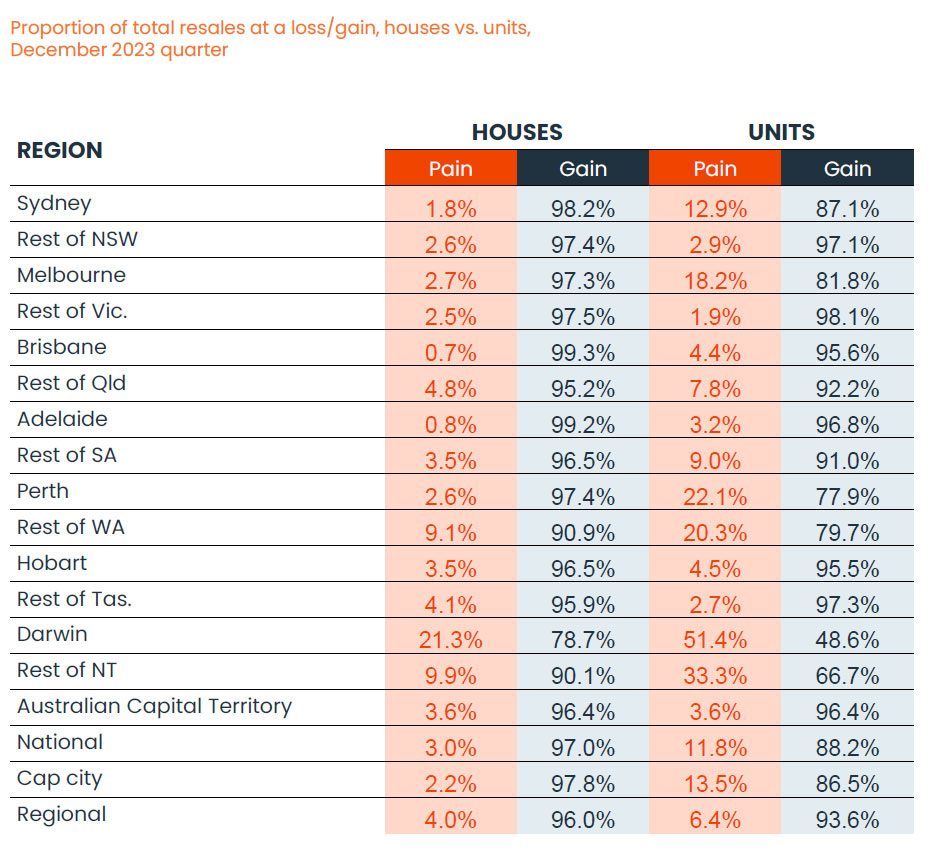

Houses were still recording higher rates of profit-making sales compared to units, with 97.0% of house resales making a nominal gain, compared to 88.2% of units.

“Underlying land value, scarcity factor and desire for more space through the pandemic has led to a substantially larger rise in house values relative to unit values over the past four years,” said Owen.

“The relatively large premium on house values has put them out of reach for many, particularly first home buyers and lower-income households. As units become increasingly attractive to buyers, the price gap between detached housing and medium to high density options will close and profitability of units will improve.”

The median hold period of resales across Australia was 9 years, making November 2014 the median initial purchase date for resales through the quarter, with national home values up 63% since then.

While nationally, loss-making house sales had a median hold period of 5.9 years and loss-making unit resales had a median hold period of 8.4 years.

“Of the greater capital city and regional house markets, most loss-making sales have been held for less than three years. Loss-making unit sales were far more likely to be held for longer, due to weaker capital growth performance,” added Owen.