This article is from the Australian Property Journal archive

THE bias of shopping centre cap rates remains skewed to the upside, while owners of everyday needs assets are receiving very little compensation for their investment risk, according to new research.

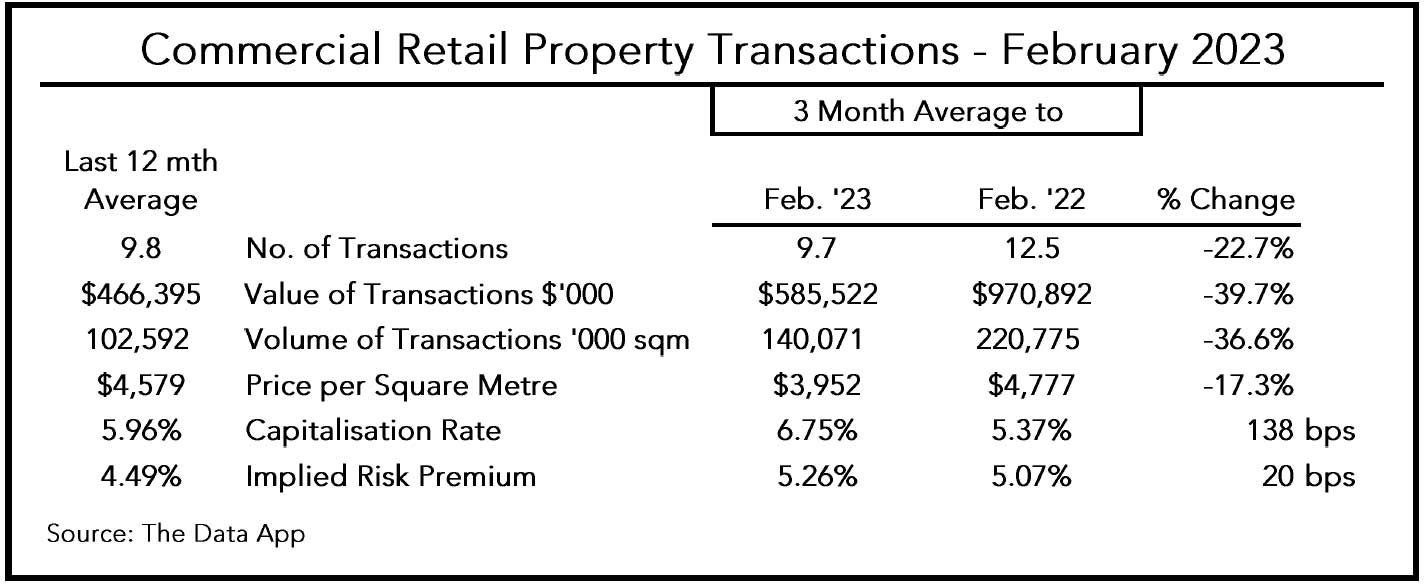

Cap rates across the retail sector are nearly 150 basis points higher than a year ago, figures from research collective the PAR Group show. Total transactions in the market for the three months to February have started to edge higher, hitting $585.5 million, but remain nearly 40% below the levels of the same period a year earlier.

Cap rates came in at 6.75%, up from 5.37% 12 months prior. The implied risk premium is 5.26%, up from 5.07%.

The volume of transactions by sqm is down 36.6%, and prices per sqm are down by over 17%.

Rob Ellis, director of The Data App, part of PAR Group said the long-run implied risk premium – the difference between the risk-free rate of interest, as measured by the yield on indexed-linked securities, and the cap rate – for all retail assets is around 5.75%.

“So, without taking any view of the future, simple mean reversion and applying the current risk-free rate of interest, would imply shopping centre cap rates of around 7.4%. On this basis, the bias of cap rates still remains skewed to the upside.”

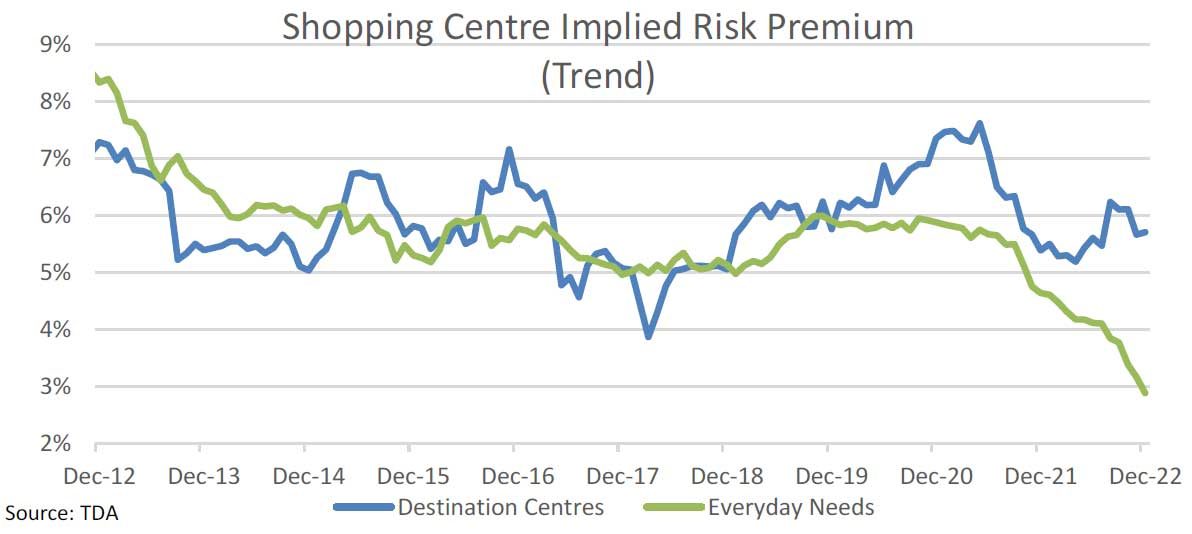

However, research by Damian Stone of Y Research under the PAR Group umbrella highlights the wide divergence in cap rates between everyday needs shopping outlets – those dominated by a supermarket – and destination centres, such as sub-regionals or larger, which contain a high level of discretionary spending shops.

Cap rates for destination centres are around 7.4%, while everyday needs are around 4.5%.

The main risk premium disparity is found with everyday needs outlets. Currently, the implied risk premium for these assets is under 3%, compared to a historical average of around 5.7%.

“It may well be consumers forgo eating out to cooking at home, or some other reason to boost the attractiveness of everyday needs centres. Be that as it may, compared to history, investors in these assets are receiving very little compensation for investment risk and, if history is anything to go by, would suggest an upwards lift to everyday needs cap rates, or significantly lower risk-adjusted returns,” Ellis said.

Meanwhile, the long-run risk premium for destination centres is around 5.85%, only a tick above the current level of about 5.7%.

“Whilst consumer spending looks set to moderate as the year progresses, particularly discretionary spending, the current risk premium is not out of kilter with the long-run trend,” Ellis said.

“This is not to say cap rates for destination centres will not rise further, just that the current risk premium is close to ‘normal’”.