This article is from the Australian Property Journal archive

MORE valuation pain could be on the way for the office sector, while retail property funds logged positive returns for the first time in nearly two years.

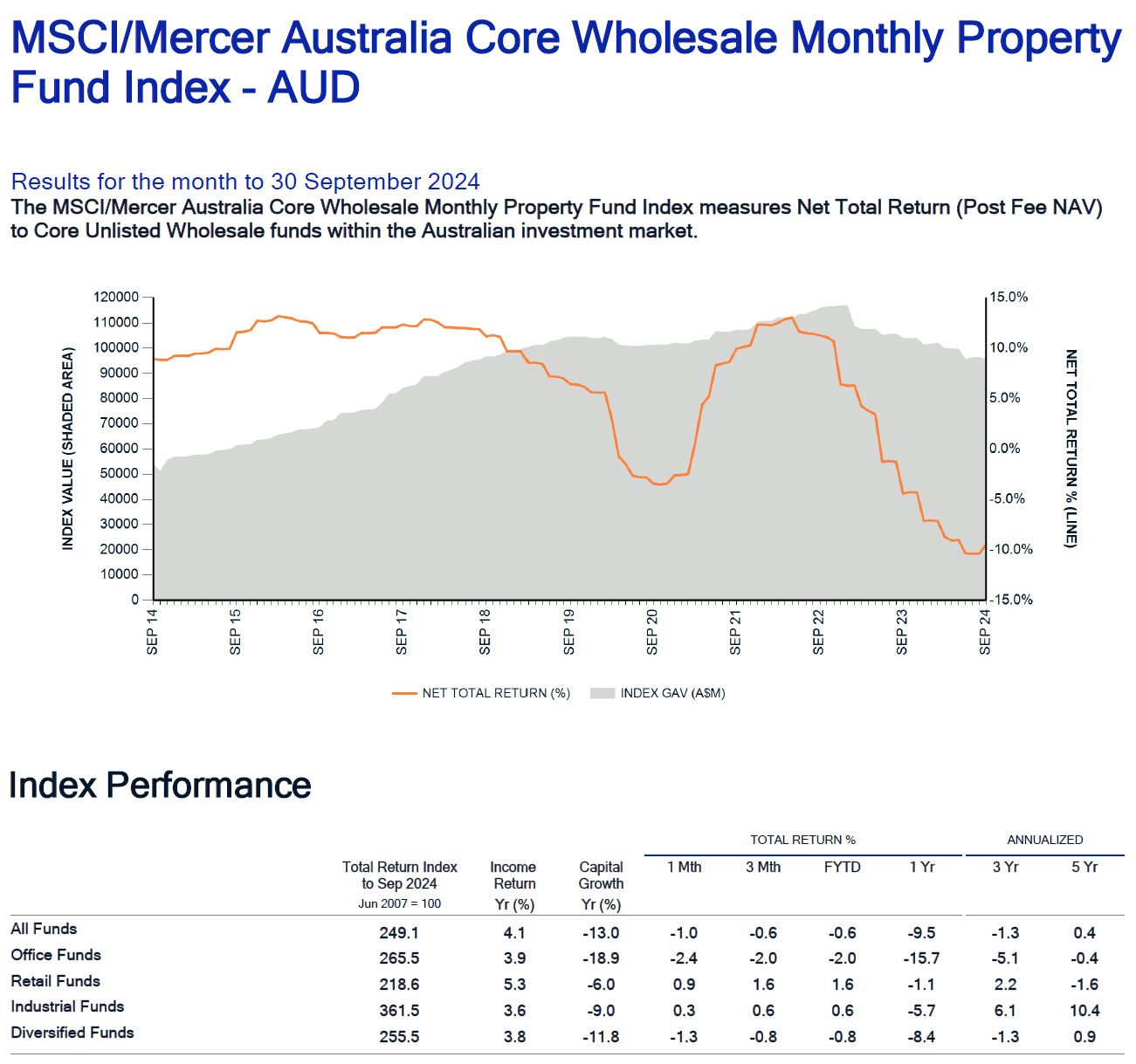

According to the latest MSCI/Mercer Australia Core Wholesale Monthly Property Fund Index, retail specialist funds recorded a capital growth of 1.6% for the September quarter, leading the traditional sectors.

“Strong sales volumes, fuelled by renewed optimism driven by high population growth and potential interest rate cuts, have likely contributed to this positive shift in values,” said MSCI’s head of real assets research, Pacific, Ben Martin-Henry.

Capping off a flurry of major asset transactions, Australia has just seen its biggest-ever single-asset retail deal, with Hines and Haben teaming up for the $900 million acquisition of Westpoint Shopping Centre in Sydney’s Blacktown.

Overall, the Index posted a negative total return of 0.59%, driven by a capital return of -1.61%, indicating that valuations are still falling.

“This fall will aid in aligning expectations between both buyers and sellers as it provides evidence that the market has yet to bottom out,” Martin-Henry said.

However, the pace of decline appears to be slowing as in the June quarter, capital return for the index came in -5.49%.

Office funds recorded further write downs in the September quarter, to the tune of -3.0%, taking the total loss in this current downturn to 26.9%.

“Whilst further losses aren’t exactly welcome news, what is welcome is that the pace of decline is slowing, as the result was a significant improvement on the -8.7% recorded in Q2 2024,” Martin-Henry said.

The office sector’s recent value adjustments seem to have improved its appeal, he said, with preliminary transaction volumes rising by 32% compared to the September quarter of 2023, and 38% year-to-date. Over $7 billion worth of office deals have been completed in 2024, with another $1.6 billion pending settlement. If all pending transactions finalise as expected, 2024 will exceed 2023 by a significant margin.

Further, the MSCI Price Expectations Gap Indicator suggests that the gap between buyer and seller expectations for Sydney offices currently stands at -7.8%, a significant convergence from the -21.5% recorded at the end of 2023. Martin-Henry said the shift “suggests that both sides are becoming more amenable on pricing”.

The MSCI/Mercer Index is released as Macquarie analysts warn that office values could have further to fall. In a research note, citing JLL data that pegs office values at 21% lower than the 2022 peak in Sydney, and 27% lower in Melbourne, they said that “further downside risk exists for valuations” given returns based on book values are “insufficient to meet hurdle rates of return for investors”.

Mirvac has recently divested the 40 Miller Street, North Sydney office building to Barings for $140 million, and 367 Collins Street in Melbourne for $345 million, both at a 20% discount to peak book values, while Dexus and the CPP Investment Board sold their half share in 5 Martin Place in Sydney to Cbus Property for $296 million, at a 24% discount to the peak value.

The MSCI/Mercer Index also showed Industrial recorded a positive total return of 0.64% in the September quarter, but was unable to generate positive capital growth as it came in at -0.31% for the quarter. Again, the pace of capital losses has also slowed significantly for the industrial sector as in the second quarter of the year the sector posted losses of -2.6%.