This article is from the Australian Property Journal archive

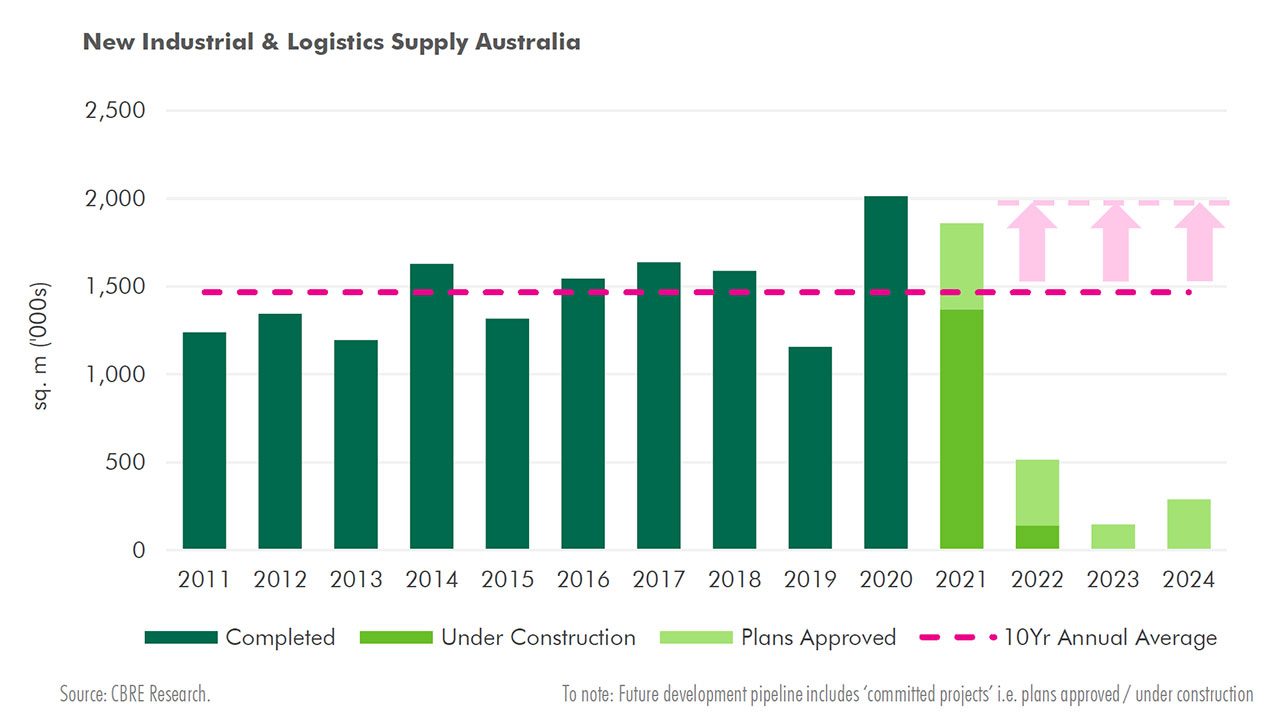

THE current industrial and logistics supply pipeline will struggle to meet the additional requirement of 500,000 sqm per year to fulfill the insatiable demand from the e-commerce sector, which is still at its infancy in Australia, according to CBRE.

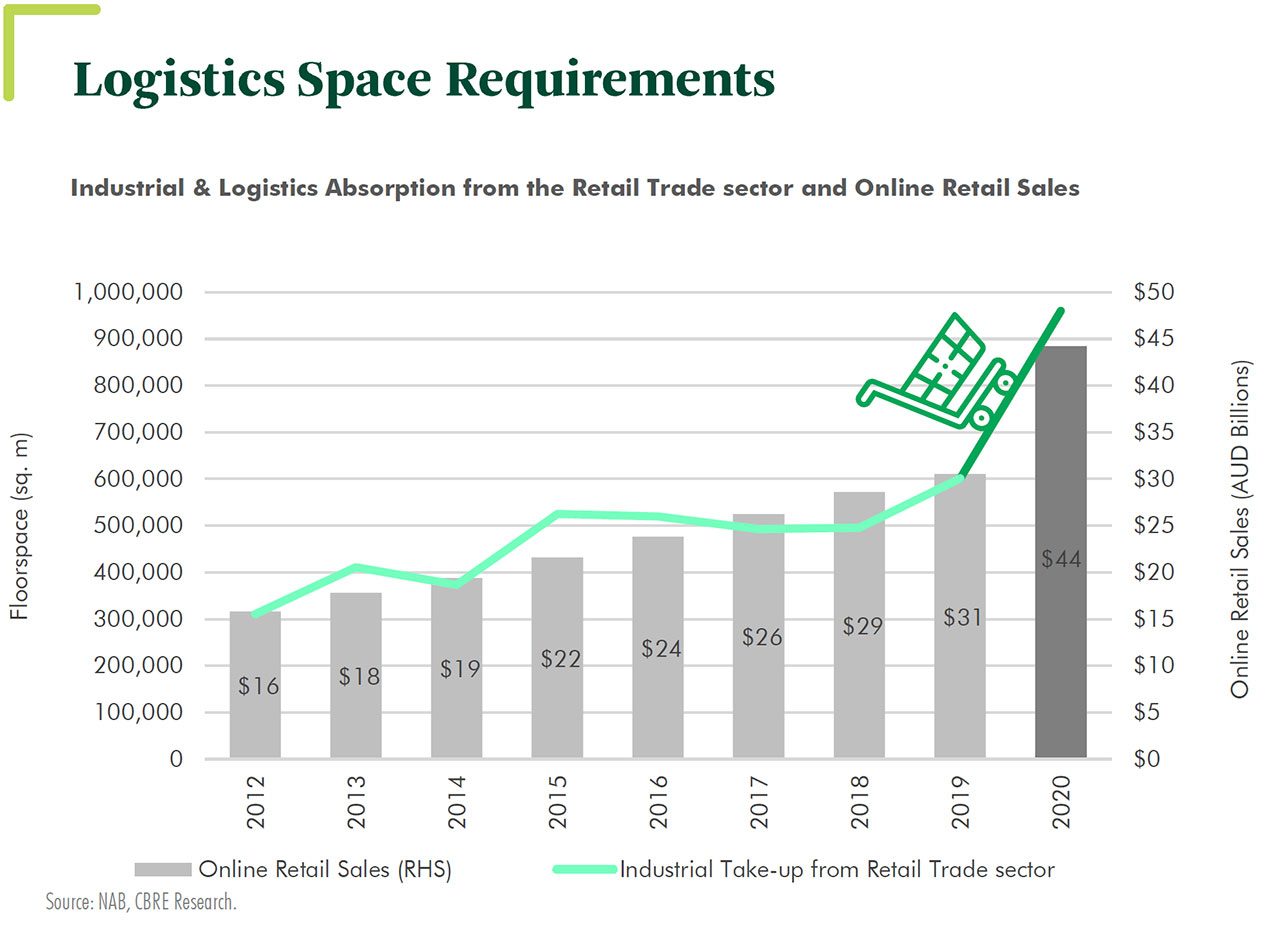

According to CBRE’s latest report, Australia’s E-commerce Trend and Trajectory, the COVID-19 pandemic boosted online sales which accounted for 13% of all retail sales in Australia in 2020, up from 7% in 2015.

As a result, retail-related floorspace absorption reached an all-time high, rising to roughly 1,000,000sqm, with Australia forecast to be a major mover globally on e-commerce penetration in the coming years.

Head of industrial and logistics research Sass J-Baleh said more space is required.

CBRE found an average of 1,400,000 sqm of space was delivered each year since 2010.

“Based on that, to cater for the growth in e-commerce, new supply will need to be elevated by approximately 35%.

“We forecast that an additional 490,000sqm of space per annum will be required over the next couple of years to support the growth of internet sales, which are expected to reach 20% of total retail sales by 2025,” she added.

“Australia’s current supply pipeline indicates a shortage of new space required to meet that.” J-Baleh said.

The report found lockdown measures accelerated online activity and space demands among e-commerce-related tenants during 2020, particularly in Melbourne.

According to Australia Post, online sales in Victoria rose by 82% in 2020, and accounted for 36% of all sales between July and October.

J-Baleh noted that in Q1 2021, Melbourne accounted for 53% of total industrial and logistics space absorbed in Australia, and that a quarter of that was from the retail trade sector.

The report also places Australia among the top 10 countries globally for forecast e-commerce penetration growth between 2020 and 2025.

Meanwhile the CBRE Global E-commerce Drivers Index 2021 found Australia’s e-commerce is still at its infancy and has further scope for growth.

The index covers six factors; share of urban population, mobile internet sales ratio, debit and credit card use, digital skills of the population, the presence of a dominant e-commerce player, and the percentage of population with a fixed broadband connection.

The report found Australia currently ranks in the middle of the pack with a score of 42 out of 100, just behind New Zealand, France and Canada, but well behind the leading South Korea and United Kingdom.

“Although Australia ranks reasonably high in most of the six factors, it scores relatively lowly in ‘mobile internet sales ratio’ at 37% and weak in ‘dominant e-commerce player’ – particularly as Amazon’s impact in the Australian market has not yet matured,” she continued.

The report found although the pandemic has accelerated the upward trend of the e-commerce penetration rate, Australia still lags behind other major countries and below the global average rate of 22%.

“The stronger presence of an e-commerce player is expected to rapidly develop and this will further drive the e-commerce penetration rate over the coming.

“Therefore there is still great scope for further expansion of this sector. We forecast the penetration rate will reach, if not exceed, 20% by 2025,”

J-Baleh said if Australia reaches an e-commerce penetration rate of 20% by 2025, this will equate to around $79 billion in online sales. A total increase of 79% in Australia’s internet sales (or $34.8 billion increase), between 2020 and 2025, is above the expected 61% growth in global internet sales.

This all points to more demand for industrial space. Over the next five years Australia will require at least 2.4 million sqm of additional e-commerce dedicated logistics space to support the growth of internet sales.

As a result, head of capital markets, industrial & logistics Chris O’Brien said major institutional investors are continuously looking to grow in the sector, with sale and leaseback arrangements a major trend in 2020.

Examples included ALDI’s portfolio in the food logistics sector, while in e-commerce the $137.1 million sale of VidaXL/HB Commerce’s site in Melbourne to GPT with a leaseback represented an investment yield of 4.08%.

“There is unprecedented demand for assets that are strategically positioned to accommodate fulfilment centres and last mile distribution hubs, as e-commerce growth is front of mind.

“On the back of the e-commerce growth story, we will see persistent increase in capital values, further yield compression, and rental growth.” O’Brien said.

Meanwhile Altis Property and Arrow Capital Partners this week acquired two industrial properties in Brisbane for $101.6 million and it recently started construction on Australia’s first major industrial and logistics community.

Demand for industrial assets continues to grow, Charter Hall recently secured a 90-year leasehold for the $300 million Light Horse Business Hub, which came hot on the heels of the $106 million purchase of a pharmaceuticals manufacturing facility and the acquisition of 25 cold storage and food distribution centres in a $270 million sale and leaseback deal with PFD Food Services.

Charter Hall has been a major player in the market rush for industrial and logistics assets, having now acquired more than $2.6 billion in industrial and logistics facilities so far in the financial year. Also recently, its Direct Industrial Fund No. 4 snapped up a pair of Patties Foods sites Victoria for $141 million in another sale and leaseback deal.

The global pandemic has made Australia even more attractive than before. A recent report by ANREV/INREV/NCREIF found investment managers raised $3.86 billion to invest down under in 2020 – $800 million more than 2019.

Real Capital Analytics data shows offshore buyers represented 42% of all deals in the first quarter, reflecting a 83% year-on-year growth.