This article is from the Australian Property Journal archive

SLOW wage growth, rise of e-commerce and falling discretionary spending have hit suburban shopping strips hard, pushing vacancy rates to 8.6% – its highest level since 2007. However the rise of online restaurant aggregators such as Uber Eats, Menulog and Deliveroo has seen food and beverage businesses increase their appetite for space.

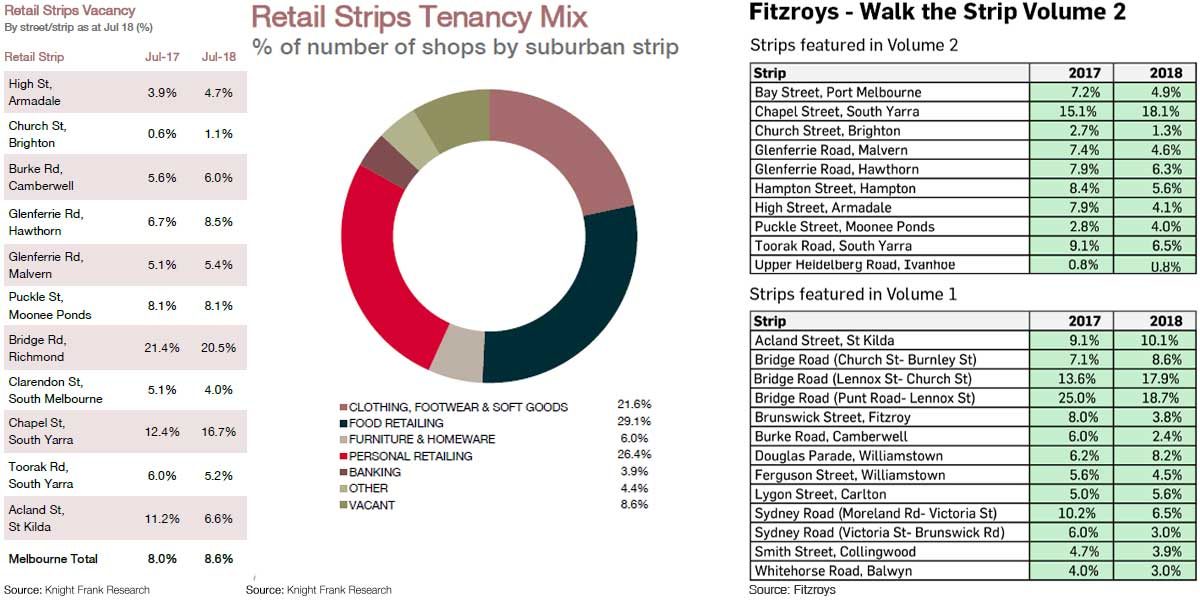

According to Knight Frank’s latest Retail Suburban Strips, the vacancy rate across Melbourne’s 11 prime retail strips is now well above the series average of 4.8%.

Knight Frank associate director of research Finn Trembath said that between 2007 to 2010 vacancy was fairly static, however it increased notably post 2012.

“This is a reflection of subdued trading conditions brought on by a shrinking pool of prospective tenants, the rise of e-commerce, and reduced discretionary spending caused by mortgage stress and more recently, slow wage growth.

“The rise in vacancy since 2017 was largely driven by an increase in empty storefronts along Chapel St where vacancy has soared to 16.7%. Bridge Rd saw a decline in vacancy however the number of empty stores is still the highest of all 11 prime retail strips covered in the survey at 20.5%, down from 21.4% a year ago,” Trembath said.

Knight Frank senior retail leasing executive Paul Pellegrino said the tenancy mix across Melbourne’s prime retail strips continues to be dominated by food as well as health and fitness, with a lower level of activity from clothing/footwear/soft goods retailing.

Knight Frank found there has been a shift from clothing to food retailing, which has the highest tenancy at 29.1%.

Trembath said the rise in vacancy since last year can largely be explained by a number of clothing and footwear retailers vacating their premises – six in every 10 (62%) vacancies in the last 12 months fell in one of these two categories.

“Upcoming major developments, such as the Capitol Grand and Aloft Hotel mixed-use residential/ retail projects and the Jam Factory redevelopment should revitalise the area, however these projects won’t be completed for another 2-3 years.

“In contrast to nearby Chapel St, vacancy along Toorak Rd, South Yarra has been trending down the last three years and is currently at 5.2%. Combined, food and clothing retailers represent more than half of Toorak Rd’s new tenants since 2017,” he added.

The latest Fitzroys’ Walk the Strip Vol. 2 report found online restaurant ordering services such as Uber Eats, Menulog and Deliveroo are driving demand from food retailers, and they do not necessarily seek prime locations.

Fitzroys’ director David Bourke noted that strip centres have seen a growing proportion of shops being used for service uses, with the number of new cafés, bars and restaurants well-documented.

“The proliferation of delivery services such as Uber Eats, Menulog and Deliveroo represents a growing proportion of food and beverage turnover, and some operators are finding a secondary location that is sufficient for their needs as there is less reliance on passing trade.

“In addition to this there are a huge number of personal care businesses such as hairdressers, beauticians, skin care clinics, masseurs and gyms opening in the strips, into locations they previously wouldn’t have considered. At this stage it is difficult for the online world to replicate this service offer,” he added.

Fitzroys’ report shows vacancies have tightened across most retail strips over the 12 months to June. Data shows Church St, Brighton had the tightest vacancy falling from 2.7% to 1.3%, and Upper Heidelberg Rd in Ivanhoe remained at a similarly low level. And Sydney Rd, between Victoria St and Brunswick Rd, fell sharply from 6% to 3%.

Senior manager Chris James said that High St, Armadale was one of the best performers, recording one of the largest falls in vacancy, from 7.9% to 4.1%. It is also the strip with the highest proportion of specialty retailers in its tenancy mix, of 59%.

Bourke said the move of Scanlon and Theodore from Chapel St early last decade began a steady migration of a number of traders, and the strip now offers an enviable range of high-end fashion retailers to go with its renowned bridalwear offering.

Fitzroys report also found rents along High St have shot up by some 20% over the past several years to be one of the biggest improvers, with prime spaces now attracting $900 to $1,000 per sqm, with those in the adjoining Glenferrie Rd, Malvern at $700 to $800 per sqm.

Glenferrie Rd, Malvern is also considered one of the strongest retail strips, with vacancies tightening from 7.4% to 4.6%. It has perhaps the most even tenancy breakdown of any of Melbourne’s strips – 32% service retail, 33% specialty retail and 31% food and beverage.

Divisional director Mark Talbot said Church St in Brighton has a high proportion of specialty retail at 52% and remains home to the highest rents across Melbourne’s suburban retail strips, with prime shops commanding between $1,250 to $1,350 per sqm.

“The long queue of high-end and national tenants for space in the strip is reflected in its continually low vacancy rate, which is constantly supporters by its constrained supply and location within one of Melbourne’s most exclusive suburbs,” Talbot said.

Conversely, the changing dynamic of once-dominant Chapel St has seen prime rents tumble from around $1,400 at the strip’s peak to around $900 to $1,000 per sqm.

Like High St and Church St, Chapel St has a considerably high 53% of specialty tenants, but the constant turnover of tenants has seen that an increase in food and beverage tenants and a different fashion offering overall.

Despite its vacancies easing out from 15.1% to 18.1% over the 12-month period, the strip is in a transition phase and its future viability is underpinned by major commercial developments in the pipeline to further complement its position next to the super-dense Forrest Hill high-rise precinct.

Stonnington City Council has also just approved Newmark Capital’s plans for a redevelopment of the iconic Jam Factory precinct in the heart of the strip with an estimated end value of $1.25 billion, joining the 10-level, 176-room Aloft Hotel development at 402 Chapel St and the 50-level Capitol Grand tower on the corner of Toorak Rd is under construction. In addition, a hotel and restaurant development is expected at 461-471 Chapel St, and a $55 million, seven-level mixed-use project at 430-438 Chapel St.

Fitzroys associate James Lockwood said that also benefiting from the development is the adjacent Toorak Rd, South Yarra strip, which now has one of the highest hospitality tenancy proportions with 37%, and vacancies have come in from 9.1% to 7.5% as rents have moved to $650 to $750 per sqm.

He added that Bay St, Port Melbourne and Toorak Rd, South Yarra have proven to be the best examples of medium and high-density residential enabling a turnaround and thriving of retail strips in the early part of this century. Bay St vacancies have come in from 7.2% to 4.9%, with rents now at $700 to $800 per sqm.

Glenferrie Rd, Hawthorn, neatly positioned in the affluent inner-eastern suburbs and with a pedestrian flow boosted by the adjacent Swinburne University and prestigious schools nearby, attracts rents of $1,000 to $1,100 per sqm. The precinct has seen food and beverage tenants increase by 4% over the past 12 months – the biggest jump of the 23 precincts surveyed – as vacancy firmed to 6.3%.

Director Chris Kombi said the retail mix in a strip centre reflects market demand rather than the pre-determined mix there is in major shopping malls, which may be seen as a strength and a weakness for strip retail, but reinforces the strips’ own individuality.

Brunswick St in Fitzroy has also seen vacancies come down, from 8.0% to 3.8%, as food and beverage operators increase their presence in the strip to a high 39%. Prime rents in the popular inner-north lifestyle and hospitality precinct are now at $550 to $650 per sqm.

Bridge Rd Richmond saw vacancies in the Punt Rd to Lennox St section come in from 25.0% to 18.7%, while the section from Lennox St to Church St eased out from 13.6% to 17.9%, according to Fitzroys.

Meanwhile Knight Frank’s Pellegrino said in strips where vacancy has risen, some retailers seeking space are being presented with a wider array of options and as a result are able to negotiate better deals by way of lower rents and more attractive incentives.

“In these cases, while rents have come back yields have remained unchanged as investors still view these areas as premium locations – an example is Chapel St where yields have remained in the range of 4.5% – 5.5% in the last year.

“Along prime strips with low vacancy there has been some yield compression associated with the promise of high tenant demand – an example is Church St where yields have compressed from 4.0% – 4.5% to 3.5% – 4.0% in the last year,”

Knight Frank found despite experiencing a decline since last year, vacancy along Bridge Rd, Richmond is still the highest of all 11 prime streets covered in the survey. For the second year running, one in every five (20.5%) shops on Bridge Rd are vacant.

“While the decline in vacancy since last year can be attributed to a number of offices and food retailers leasing out space, countering this new vacancies were mostly made up of clothing retailers vacating their premises. Increases in rents, a lack of car parking spaces, and the lure of retail options in the CBD are felt to be driving the high vacancy levels along Bridge Rd,” Trembath said.

According to Knight Frank, vacancy on Puckle St, Moonee Ponds remains the same at 8.1% while High St, Armadale rose slightly from 3.9% to 4.7%; Glenferrie Rd, Hawthorn increased from 6.7% to 8.5%while the Malvern end rose from 5.1% to 5.4%; Burke Rd, Camberwell had a slight rise from 5.6% to 6.0% and Church St, Brighton grew from 0.6% to 1.1%.

Strips that recorded a decline in vacancies includes Toorak Rd, South Yarra which fell from 6.0% to 5.2%, Acland St, St Kilda dropped from 11.2% to 6.6% while Clarendon St, South Melbourne fell from 5.1% to 4.0%.

Prime rents currently range between $400 to $800 per sqm.

Pellegrino said investment activity across the strips remains stable with $77.4 million in transactions over the past year with High St, Armadale accounting for $27.8 million of the total.

Australian Property Journal