This article is from the Australian Property Journal archive

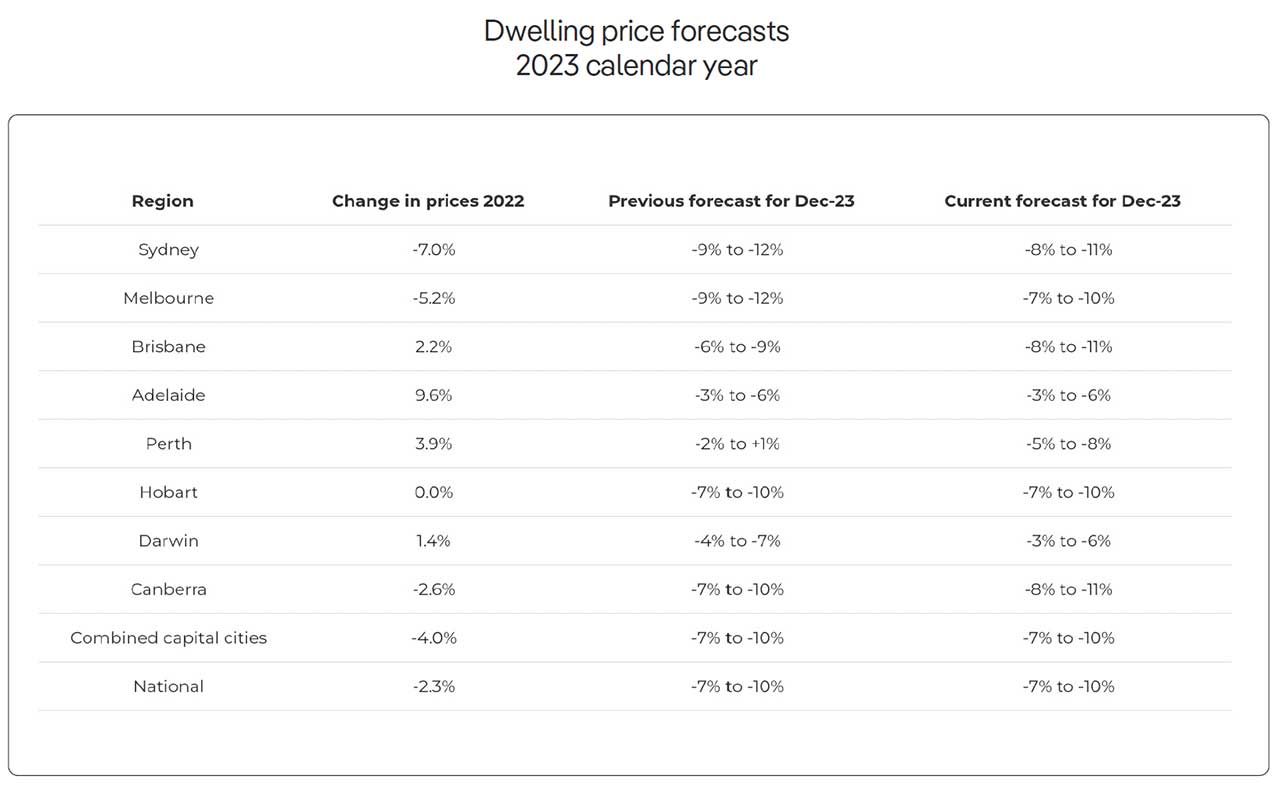

RESIDENTIAL property prices are forecast to fall between 7% and 10% this year, as further hikes to the cash rate leave borrowing power diminished.

According to REA Group’s PropTrack Property Market Outlook February 2023 Report, predicted declines to property prices follow a 2.3% decline over 2022 and will impact each capital city.

Sydney, Brisbane and Canberra are expected to see the greatest declines in property prices over 2023, with falls set to be between 8% and 11%.

While both Melbourne and Hobart are forecasted to see falls in line with the national average, between 7% and 10%.

Adelaide, Darwin and Perth are expected to remain the most resilient, with respective falls between 3% to 6%, 3% to 6% and 5% to 8%.

These forecasted declines are based around the assumption of a further 50 basis point rise to the cash rate before the RBA’s February meeting, which currently sits at 3.1%.

“At the beginning of May 2022, official interest rates were sitting at 0.1%. By the end of 2022, the cash rate had increased to 3.1% – the highest it has been since November 2012 – due to the fastest and most substantial interest rate tightening cycle in many decades,” said Cameron Kushner, report author and director of economic research at PropTrack.

“While we don’t expect interest rates to rise as fast and high as they did in 2022, we are expecting some additional increases early on in 2023.”

While February is likely to see a 25 basis point increase, and interest rate rise just 50 basis points would see borrowing capacities down by around 30%.

“We expect two 25 basis point cash rate hikes from the Reserve Bank of Australia, one to be delivered today. Following this, we expect a period of interest rate stability. However, an interest rate cut late in 2023 is a very real possibility depending on how the economy performs,” added Kushner.

“With borrowing costs continuing to rise and the subsequent reduction in borrowing capacities, property price falls are likely to continue and accelerate in 2023, with the more expensive cities likely to see the largest price falls.”

Kushner added that falls to prices wouldn’t be restricted to the capitals, with demand likely to dip for regional locations, where growth has been elevated since the onset of the pandemic.

“After exceptional price growth throughout the pandemic, last year’s changing market conditions saw prices fall 2.3%. With prices down 4.3% from their peak, a fall of up to 10% this year would result in cumulative declines of close to 15% since the start of the downturn,” said Kushner.

“Importantly, this fall would represent a decline of around half that of the decline in borrowing capacities and would still have national home prices sitting above their pre-pandemic levels.

The report also found that preliminary sales volumes in 2022 were 16.5% lower than 2021 levels, though 16.9% higher than 2019.

The total number of properties listed for sale on realestate.com.au in December 2022 was up 6.3% year-on-year, while enquiries per listing on realestate.com.au was down 34.6%.

With the volume of new stock coming to market slowing since its peak in March 2022, down 24.8% on December 2021 levels, with the median number of days a property was listed on realestate.com.au at 42 days, up 10 days on the December 2021 record low.