This article is from the Australian Property Journal archive

PRIVATE investors appear to be the only ones still buying as Australia’s commercial real estate transaction volumes continue to hover around record lows, according to MSCI Real Assets, and several quiet years may be ahead for other buyers.

MSCI Real Assets research showed that for the first five months of 2023, private investors accounted for 57%, or $5.5 billion, of total transaction values, a jump from the 40% over the same period in 2022.

Listed players, on the other hand, made up only 11%, or about $1 billion – an 80% decrease year-on-year.

“We are witnessing a pattern reminiscent of previous slowdowns like the Global Financial Crisis (GFC) and during the COVID-19 pandemic,” Benjamin Martin-Henry, Head of Pacific Real Assets Research at MSCI, said

“One explanation may be the inherent opportunism of private investors. During periods of market turbulence, they often seek out opportunities when more cautious institutional investors remain on the sidelines,”

Offshore investors and private players driven by attractive asset pricing have been tipped to dominate Australian retail real estate acquisitions throughout 2023, while AREITs will likely be net sellers.

Private investors have shown a strong preference for the retail sector this year, which accounts for approximately 32% of their allocation as at the end of May, despite other investor groups largely avoiding it.

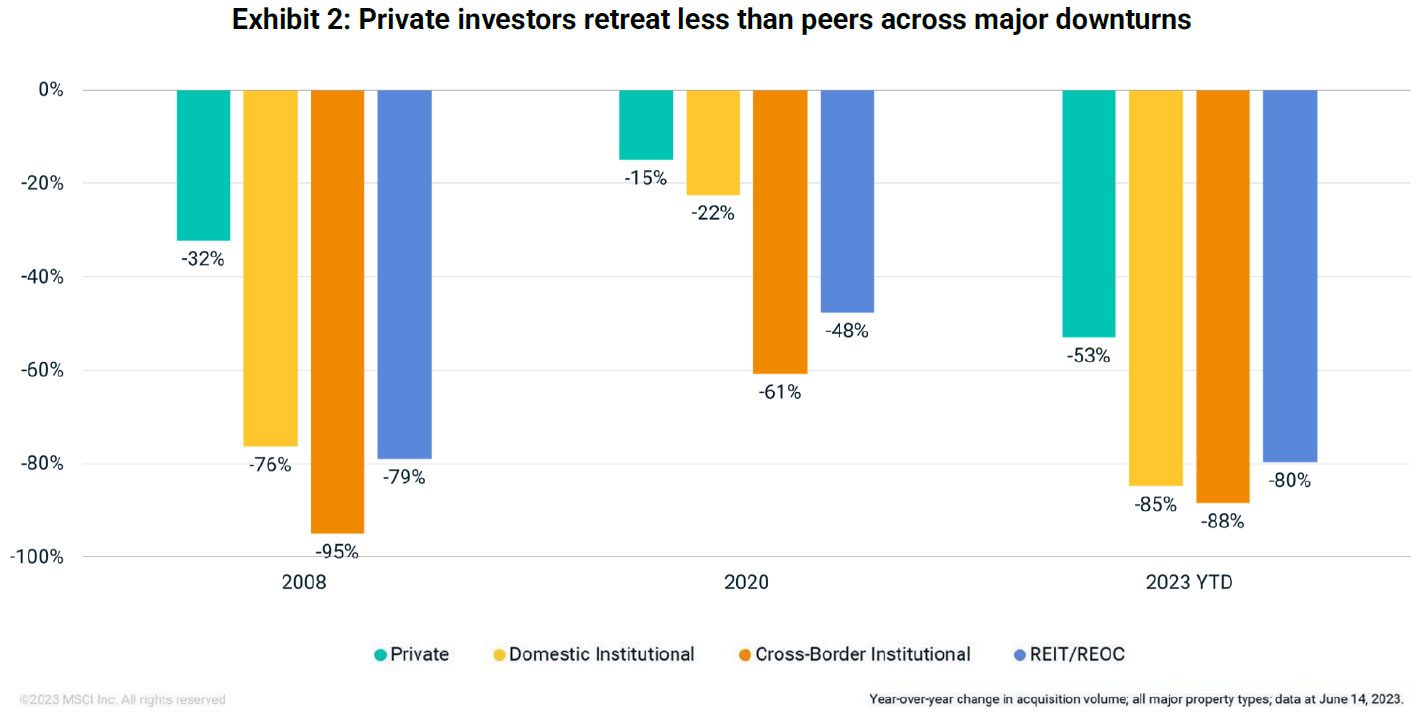

The total volume registered by private investors in the first five months of 2023 was still a decline of 53% year-on-year, but private investors are proving relatively more active than their counterparts. Martin-Henry said that besides listed players pulling back sharply, cross-border institutional investors are also largely absent.

A similar trend had emerged in the wake of the GFC in 2008, he said. During the GFC, private investors reduced acquisition levels by about 30% compared to 2007, listed players cut their acquisitions by around 80%, and institutional investors — both local and from overseas — almost entirely withdrew from the market, and stayed away in the aftermath.

“What might we infer about future buyer activity from historical trends? If patterns are to be repeated, it wouldn’t be surprising to see several quiet years ahead for buyers other than private players,” Martin-Henry said.

He said that In terms of recovery, it took private investors four years to return to pre-GFC (circa-2007) investment volume levels, whereas listed players took six years. Institutional cross-border investors did not return to 2007 levels until 2021. Domestic institutional investors did not reach 2007 levels until 2013 and their cross-border counterparts still have not recovered to those levels, even though they came close in 2021.

“Last year there was uncertainty around interest rates. Now, I think there’s more certainty about where interest rates are going…but, the problem we have down here is that pricing is a huge problem. There is quite a large gap between buyers and seller expectations.”

MSCI analysis showed office values would need to shift by 15% to 18% in order to get back to long-term liquidity levels. That figure is slightly higher for retail assets and slightly lower for industrial and logistics.

Dexus’ has just confirmed that its 44 Market Street tower in the Sydney CBD had sold at a 17.2% discount to book value, and it is also reportedly selling 1 Margaret Street at a 21% discount to the book value.