This article is from the Australian Property Journal archive

AUSTRALIA’S build-to-rent sector has seen a massive surge over 2023, with Victoria still leading state for the sector.

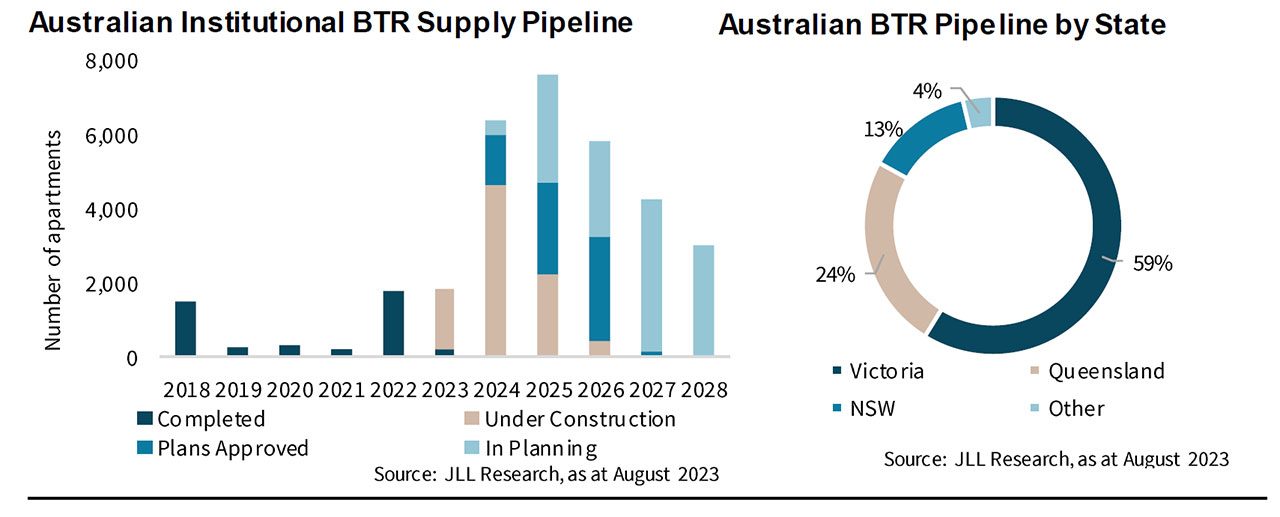

According to JLL’s latest Build-to-Rent (BTR) Residential Australia report for September 2023, institutional grade BTR projects in the pipeline are up 56%, with the number of apartments under construction nationally up 65% over the first 8 months of 2023.

Additionally, the number of apartments with planning approval awaiting construction was up 15% and the number of known projects proposed at various stages of planning was up 78%.

“Low vacancies, rapidly rising rents and growing displacement of low-income earners has undoubtedly focused the attention of all levels of government nationally on addressing what has become a critically important social issue,” said Leigh Warner, head of residential research at JLL, Australia.

“Accordingly, in 2023 we’ve seen the introduction of a range of government incentives aimed at supporting the emerging BTR market.”

There are forecast to be more than 4,000 BTR apartments under construction and due in 2024 and more than 7,500 are in various stages of the planning and construction that are due in 2025.

“But while BTR is gaining momentum quickly following those changes, the BTR supply pipeline is not yet large enough to offset the fall in BTS [build-to-sell] construction and we still will not build anywhere near enough apartments over the next few years,” added Warner.

“Indeed, we expect if all BTR currently proposed over the next five years is delivered, it will still only equate to around 10% of historical apartment supply levels.”

At the same time, the latest research from Knight Frank found the BTR sector is expected to see 55,000 dedicated units completed by 2030, based on the current pipeline of developments along with the UK’s current BTR growth trajectory.

59% of the current pipeline is located in Victoria, followed by 24% in Queensland and 13% in NSW.

“Investors now largely accept the macro investment case for BTR in Australia. As capital markets continue to stabilise and as investors become more familiar with underwriting what is still a relatively nascent sector, we expect investor demand will only increase,” said Luke Prokuda, head of equity advisory at JLL, Australia.

Prokuda noted that activity in the BTR and broader living sectors remained relatively strong, while capital market conditions left vast majority of the commercial real estate sector strained.

“Furthermore, we expect further clarity will emerge on the Federal Government’s decision to reduce the withholding tax rates for foreign investors in MITs, which will allow investors to factor this change into the underwriting considerations,” added Prokuda.

Increasing residential rents across the country have also supported BTR project feasibilities, attracting greater interest from developers and investors.

“Long selling periods, particularly for larger BTS projects, are highly detrimental in a market where construction resources remain stretched and finance costs uncertain, which leaves developers very vulnerable to any rise in a project’s cost base,” said Warner.

‘’Not only do BTR projects have the benefit of no selling period, but project revenues are rising in a market of strong rental growth and this is supporting project feasibilities.”