This article is from the Australian Property Journal archive

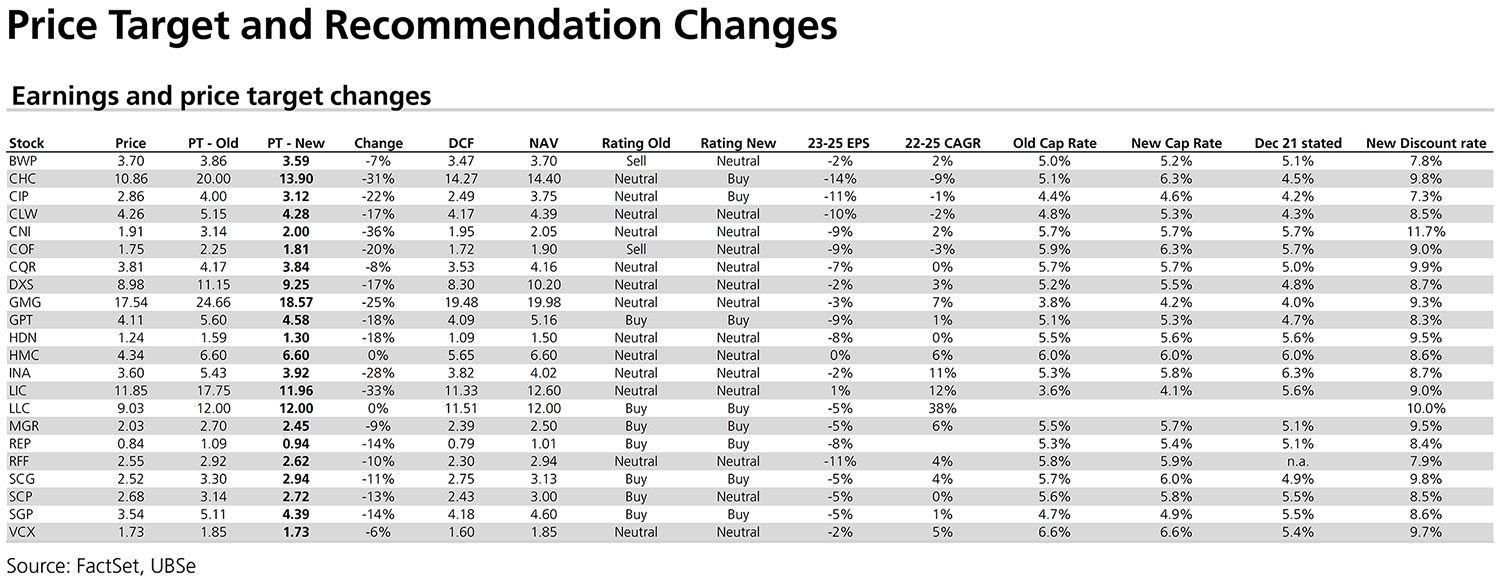

UBS has cut its price targets for A-REITS by an average of 15%, with trusts exposed to interest rates set to see a drop in profits between FY23 and FY26.

According to UBS’ latest Australian Real Estate Sector Update, the current environment of policy normalisation and surging inflation is leaving markets to price in negatives outcomes such as the risk of a recession or stagflation.

While an average upside of 11% is forecasted to blended price targets, UBS has adjusted targets to be 15% lower on average.

This was attributed to NAV-based valuations reflecting the normalisation of a higher growth/rate environment and a DCF scenario where debt costs for FY26 are looking to be 6% greater than previous forecasts.

The sector is now expected to see a 5% drop in earnings in the FY23-26e period, based on assumptions of base rates hitting 2.5% by the close of FY23, which should only be marginally off-set by inflation linked loans.

The decrease in sector earnings forecasts is also based on a circa 8% asset devaluations for real estate fund managers in in FY23, as well as a forecasted FY24 of declines for Mirvac (ASX:MGR) and Stockland (ASX: SGP) by 7% and 8% respectively due to their higher exposure to residential.

While UBS also most preferred in MGR, SGP, Charter Hall Group (CHC), GPT, Scentre Group (SCG) and Centuria Industrial REIT (CIP).

The update also affirmed logistics as the most preferred sub-sector, followed by retail and then office.

On the other end, UBS’ least preferred were Vicinity Centres (VCX), Dexus (DXS), Centuria Office REIT (COF), BWP Trust and Charter Hall Long WALE REIT (CLW).

The update upgraded its recommendation to buy for CHC and CIP, with respective cut price targets to $13.90 and $3.12.

Despite the declining profitability of CHC’s assets under management, lack of whole sale investor support, debt issues in funds and rising cost of capital in satellite REITs, CHC is expected to see a 38% discount to its five-year average.

“We believe CHC is still in a position to grow AUM through a period of dislocation with support from key investors,” said read the update by UBS analysts Grant McCasker and Tom Boder, and associate analysts Cody Shield and Julia Chen.

CIP on the other hand is set to benefit from high rates of demand for space from logistics tenants and resulting strong market rental growth and supporting asset valuations.

“We view CIP as the leading pure play logistics A-REIT,” read the update, looking to the REIT’s weighting UBS’ most preferred sub-sector (logistics) for listed and unlisted capital.

CIP provides investors with a secure defensive rental income in a turbulent environment, thanks to its long WALE and strong occupancy levels.

Meanwhile COF and Shopping Centres Australasia (SCP) were moved to neutral recommendations, with respective cut price targets to $1.81 and $2.72.

With high levels of inflation of circa 75bps to 100bps per annum, UBS believes the REIT sector is 4% to 8% below fair value.

A forecasted circa $3.5 billion in asset sales of circa $2.5 billion in equity is believed to be needed to restore interest rate coverage for the REIT sector.