This article is from the Australian Property Journal archive

AUSTRALIA may have just five years of industrial land supply left, with demand to continue climbing and land absorption volumes holding strong.

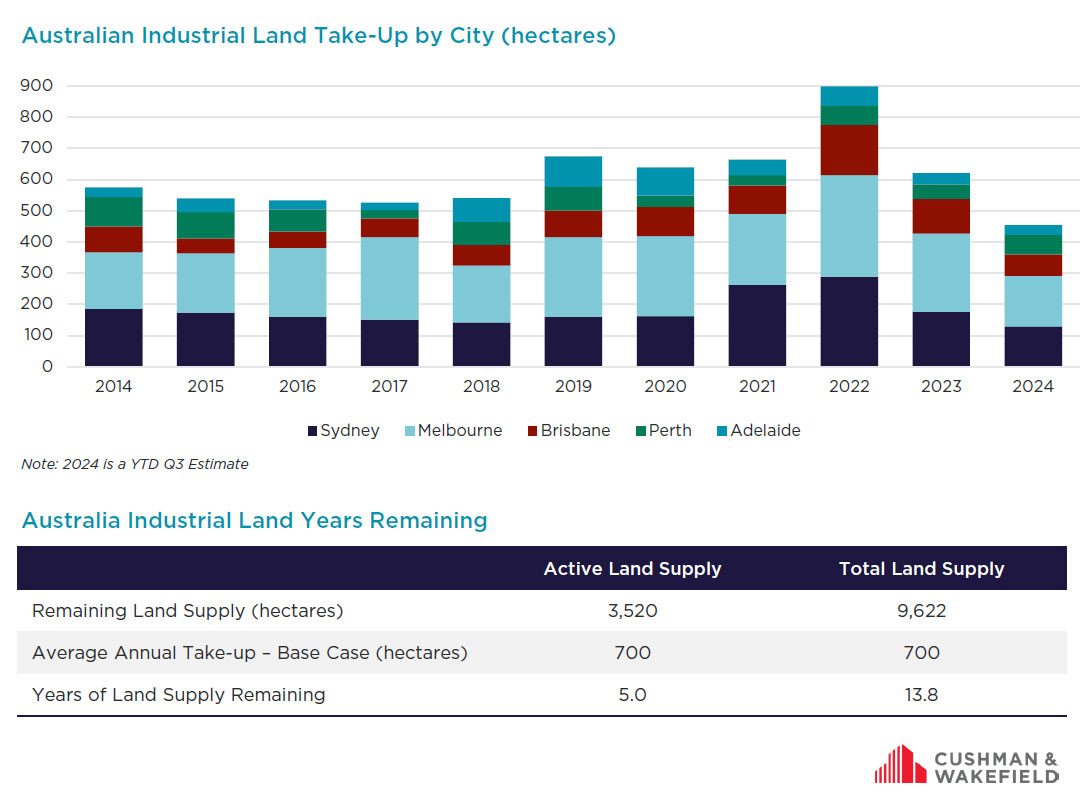

According to recent modelling from Cushman & Wakefield, Australia is expected to run out of industrial land by 2029, despite take up moderating from its 2022 peak, national take-up at 700-hectares per annum on average.

The report categorised land “active supply”, which would be development-ready within two years and “inactive supply”, land which is unserviced or unlikely to be ready in the current development cycle.

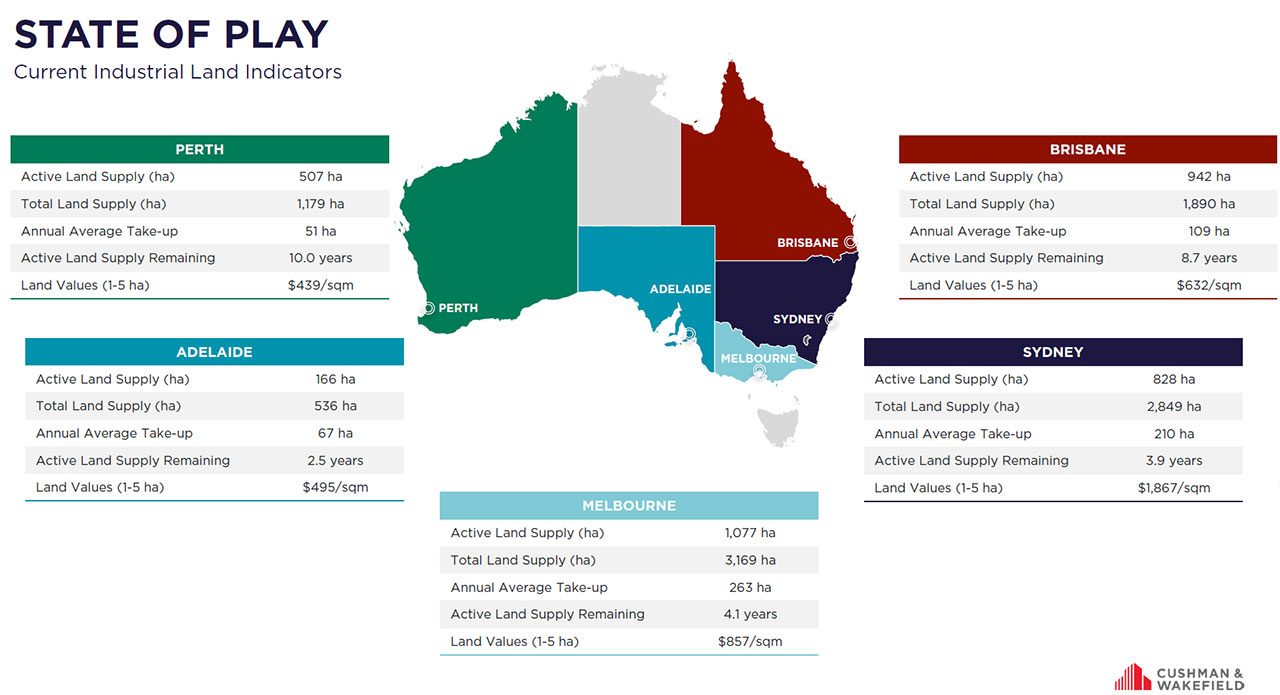

40% of the 9,600-hectares of vacant industrial land, or 3,520-hectares, has been identified as active supply.

“While signs of an industrial land shortage were evident in 2021 and 2022, economic uncertainty over the past two years has masked this issue,” said Luke Crawford, head of logistics and industrial research, Australia at Cushman & Wakefield.

“With demand expected to increase and the economic growth outlook improving, the true extent of the undersupply is becoming clear.”

Melbourne and Sydney represent the most significant supply, with a 33% and 30% share respectively, though both also see the fastest take-up and will run out of land in only around four years by the report’s modelling

In Melbourne, 1,077 of the 3,169 hectares of land was identified as active supply and is basically split across the North and West submarkets.

The city’s South East submarket is less suitable for institutional developers, with 60% of parcels in the area sub-four-hectares.

With an average annual take-up of 263-hectares, Melbourne is estimated to have 4.1-years of active land supply remaining.

In Sydney there is around 2,850-hectares of vacant industrial zoned land, which is mainly located with the Western Sydney Employment Area and the Aerotropolis precincts.

However, the NSW capital has far less land which is ready to be developed in the next two years, with just 828-hectares of active land supply

With an average annual take-up of 210-hectares, Sydney should have 3.9-years of active land supply remaining.

Additionally, land absorption is high in Sydney due to the increasing presence of and demand for data centres, which has made up 20% of transaction since 2020.

While CBRE’s Q1 Asia Pacific Data Centre Trends report found new Australian data centre supply is now fully contracted, due largely to rapid cloud adoption and AI demand.

In Brisbane there is 942-hectares of active supply, though just 24% of this is located in in-demand infill locations.

With a total industrial land supply of 1,890-hectares and an average annual take-up of 109-hectares, Brisbane should have 8.9-years of active land supply remaining.

Perth has just 507-hectares of active land supply, out of a total 1,179-hectares and with an annual average take-up of 51-hectares should have 10 years of stock remaining.

Adelaide currently has the smallest pipeline of active supply remaining, with a mere 166-hectares of active land supply out of a total 536-hectares and just 2.5-years of land estimated to remain.

“While overall land stocks may appear abundant on paper, the reality is that a large portion of this land is either unserviced, held by inactive owners or located in periphery precincts. With a shortage of developable parcels, we’re likely to see more redevelopment of infill sites, which could include multi-storey developments,” added Crawford.

“This is also in response to occupiers’ preference for sites that are close to end users, offer operational efficiencies and strong ESG credentials.”

“Population growth alone will underpin demand for up to 4,000 hectares over the next decade, and the challenge will be the availability of suitable and serviced sites.”

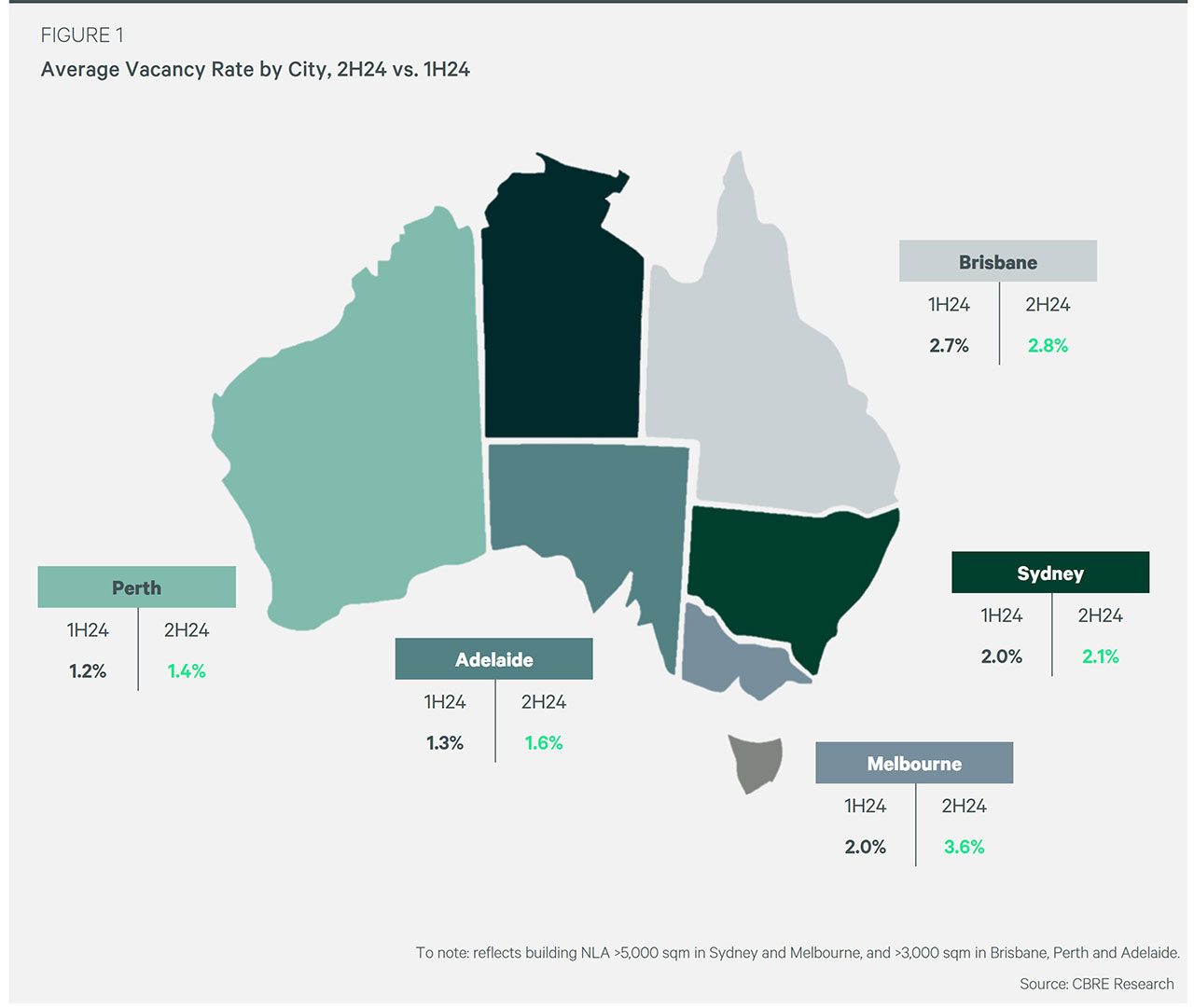

Meanwhile, according to CBRE’s H2 2024 Australia’s Industrial and Logistics Vacancy Report, the national vacancy rate in the sector rose to 2.5% over the second half.

Though, this still sits at one of the lowest rates in the world, despite seeing a significant lift from the all-time low of 0.6% in the first half of 2023.

Melbourne recorded the biggest increase and now sits at 3.6%, with Brisbane at 2.8%, Sydney at 2.1%, Adelaide at 1.6% and Perth at 1.4%.

“We believe most of the rise in incentive levels has occurred over the second half of 2024, and we anticipate a more moderate rate of growth in incentives throughout 2025,” said Sass Jalili, head of industrial & logistics and data centre research, Australia at CBRE.

“Over the medium to long term, Australia’s supply of serviced zoned industrial land will remain constrained, and this will continue to play a role in a limited development supply pipeline. This scarcity, combined with Australia’s expanding net exports, e-commerce sector, and strong population growth, will continue to support the long-term growth of the sector.”