This article is from the Australian Property Journal archive

THE next 12 to 18 months will be “difficult” for commercial real estate, with vacancies in the troubled office market are yet to reach their peak, according to Moody’s Ratings, and tower values are set for further falls as the sector continues to face existential challenges.

However, the flight-to-quality will support the ability of rated AREITs with more modern assets to attract and retain tenants.

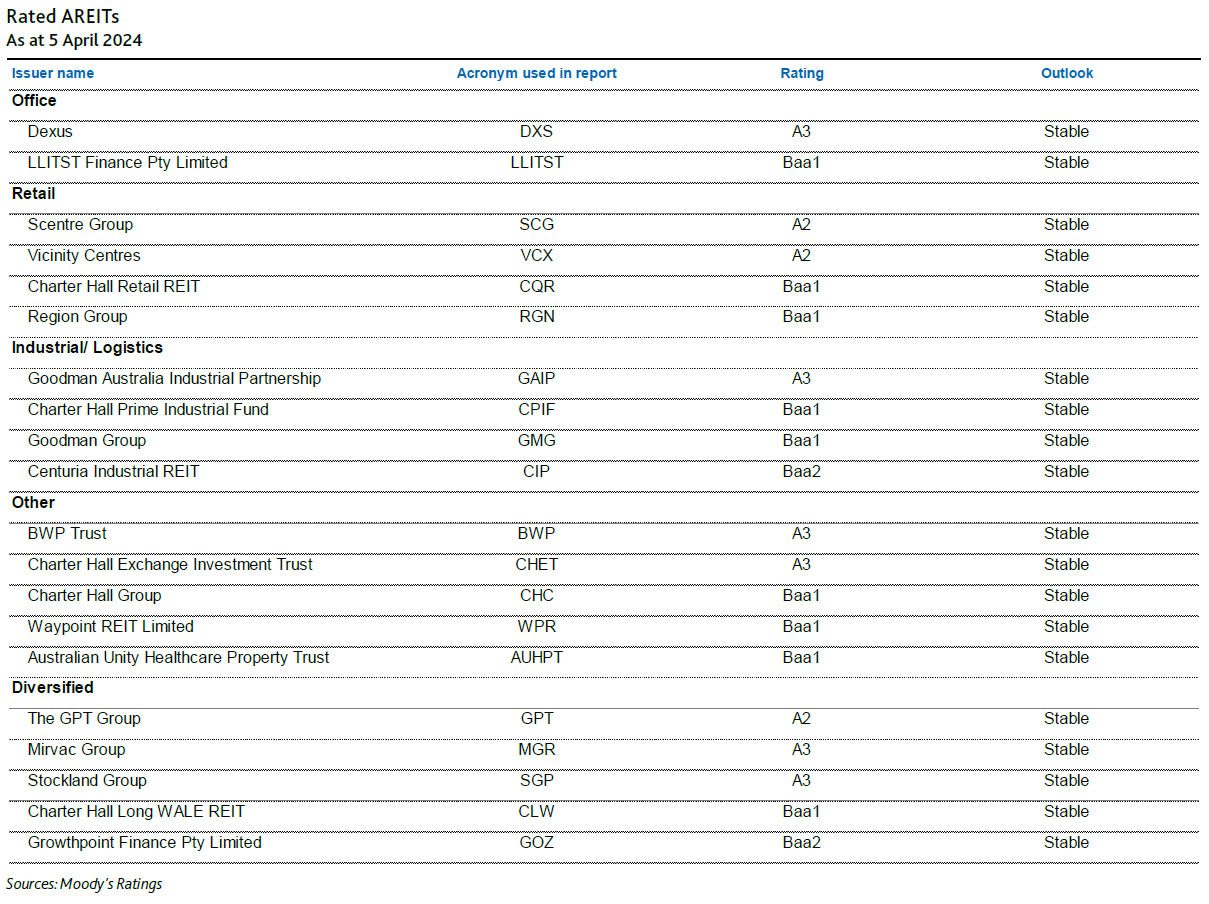

“The GPT Group (A2 stable), Mirvac Group (A3 stable) and Dexus (A3 stable), which have the largest office exposures, have high-quality assets, stronger and larger tenants, staggered lease maturities and leases that mostly have built-in rent escalations. They will maintain occupancy levels and register flat or slightly positive comparable rental growth,” Moody’s Ratings economists said in the Credit buffers diminish on high interest rates and falling asset values.

“Office building vacancies in Australia have risen above historical average levels as corporate tenants reassess their workspace needs in response to increased flexible working arrangements.

“This trend, together with elevated supply and a weaker economic growth outlook, will drive further increases in vacancy levels and asset value declines over the next 12 months.”

Mirvac has just offloaded its 50% share Sydney CBD office tower 255 George Street for $363.8 million, at a 9% discount to book value and 17% discount to its peak value.

Falling office tower values and higher interest were key reasons for commercial real estate transactions plummeting by nearly half in 2023 to $39.6 billion, according to MSCI.

“Asset values have fallen on the back of the high cost of borrowing, which weakens demand for real estate and overall economic activity. Further declines in asset values are likely in the next 12 months. The current average capitalization rate of 5.8% for office, 5.6% retail and 5.2% for industrial assets could widen further in the period,” the economists said.

These rates provide a margin of 1.5, 1.3 and 0.9 percentage points for office, retail and industrial, respectively, over the cash rate at March 2024 of 4.35%, according to Moody’s Ratings. In comparison, the eight-year average margin over the cash rate was 4.5% each for office and retail, and 4.7% for industrial.

“As a result, capitalisation rates will likely increase over time to reflect the higher cash rate, implying a further decline in asset values or increasing rents, or both.”

Moody’s Ratings said rated AREITs will continue to face “challenging” operating conditions in Australia from a combination of elevated interest rates, softer economic growth stemming from moderating household spending, and weakening asset values.

“The next 12 to 18 months will remain difficult for rated Australian real estate investment trusts.”

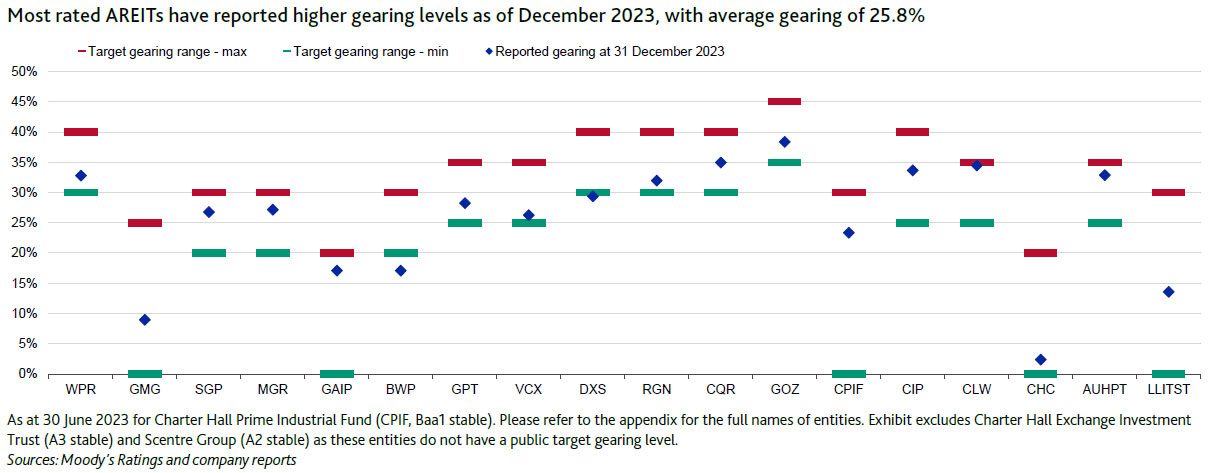

The sharp rise in interest rates will weigh on the debt serviceability and portfolio asset values and this will see credit continue to decline further over the period.

“However, the rated companies continue to benefit from good asset quality, favourable lease structures and solid, but reducing, balance sheet capacity. We expect the fixed charge coverage ratio, which tends to lag interest rate increases because of high levels of hedging, and debt-to-assets gearing to weaken further from current levels, but remain within rating tolerance and debt covenant levels.

“Liquidity is excellent.”

Strong population growth to buoy retail sector

Strong population growth and a strong employment market, and low new supply of retail space will support rated AREITs with retail exposure, the economists said.

“Despite a slowdown in retail spending, retail landlords’ rental income will grow on strong occupancy, improved releasing spreads, and rent increases either linked to the consumer price index or on a fixed basis, reflecting the strength of the portfolios.”

Meanwhile, industrial continues to be the strongest performing asset class, but the runaway rental growth of the past few years will ease.

“Industrial space availability remains tight on scarcity of serviced zoned land despite new supply. Tenant demand is solid on the back of population and e-commerce growth, global supply chain efficiencies, and growing cloud computing and artificial intelligence applications that drive demand for data storage.

“However, rental growth has peaked and vacancy rates will inch up from record-low levels.”