This article is from the Australian Property Journal archive

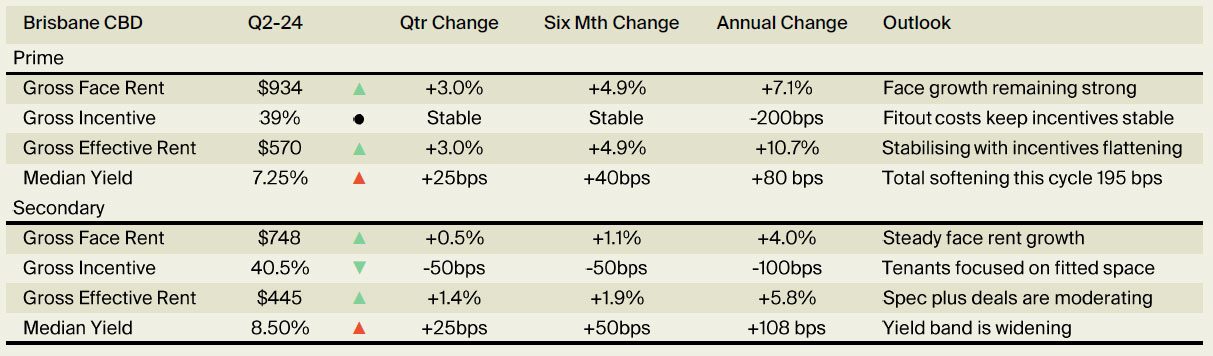

THE Brisbane CBD office market outperformed Sydney and Melbourne over the second quarter, with the city’s prime rent growing at its fastest rate since 2008.

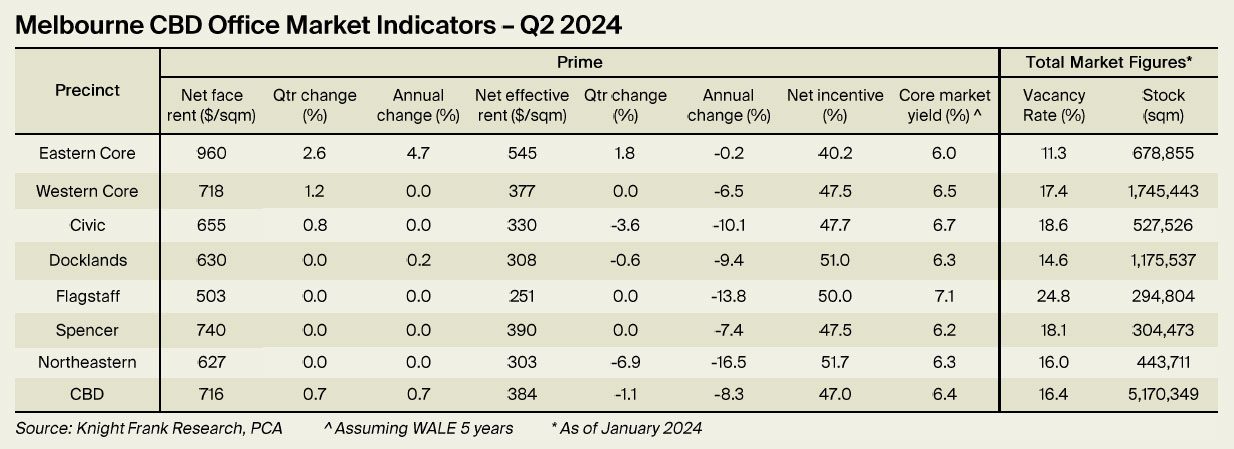

According to the latest research from Knight Frank, The Brisbane CBD market’s net face prime office rent was up by 3.6% over the quarter, followed by Melbourne at 2.3% and Sydney at 2.1%.

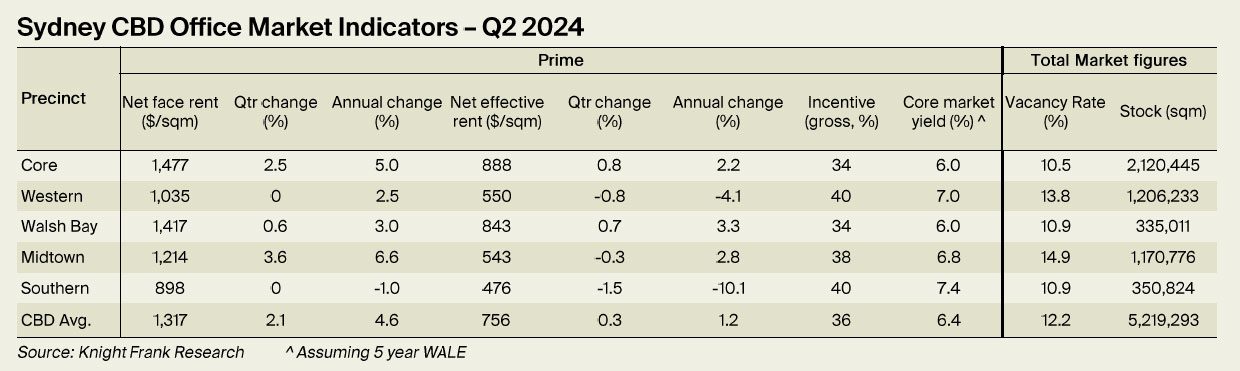

Annually, Brisbane’s prime rental growth rose to 8.1%, followed by Sydney at 4.6% and Melbourne at 2.4%.

“Strong prime rental growth in the Eastern Seaboard CBD office markets over Q2 demonstrates that occupier demand for quality office space remains resilient,” said Ben Burston, chief economist at Knight Frank.

“While the economy has been sluggish and vacancy rates are elevated, businesses continue to seek out higher-grade options that will appeal to staff and that align with wider corporate objectives including more stringent ESG requirements.”

While the city’s growth was even stronger on an effective basis, incentives falling and leading to an effective growth of 15.1% year-on-year.

With growth for Brisbane’s secondary assets was at 3.8% year-on-year.

“Multiple pressures are driving a rapid escalation in Brisbane rents, with the market responding to growing demand, high construction costs and limited availability of premium and upper A grade floorspace,” added Burston.

“Despite recent growth, Brisbane rents remain well below previous peaks and growth looks to have further to run.”

Annually, Sydney saw a 4.6% boost in average prime rents, with Melbourne trailing with a 2.4% increase in the year to the end of Q2 2024.

On an effective basis, Sydney saw growth of 1.2% year-on-year, while Melbourne saw a decline of 6.3%.

“While flexible working is here to stay, this has not hampered demand in the three key Eastern Seaboard CBD cores in Australia,” said Andrea Roberts, national head of leasing at Knight Frank.

“Occupiers recognise the need to provide workplaces that support high productivity, wellness, technology, collaboration and lifestyle.”

Roberts noted that the 2023-24 financial year has seen demand remain for amenity-rich well-located offices with close access to public transport, even with the rise in flexible working.

“Brisbane has certainly seen strong demand in FY 24 and we expect Melbourne and Sydney to continue to experience solid demand in FY 25. This will come off the back of ongoing occupier interest for the best office product, at the same time as we are seeing limited new development,” added Roberts.

“This scarcity of new office buildings will continue for remainder of the decade due to higher construction and financing costs, and will create improved deal metrics for landlords in the coming years.”

While occupier demand has remained solid over the year, office assets have been selling well below their peak book values in recent weeks.

The Australian Unity Office Fund recently finalised the sale of a relatively brand new office building in Brisbane’s south, for $29.7 million, after paying $33.52 million for the office in 2021.

With Quintessential also completing its $250 million acquisition of the 240 Queen Street at a 17% discount to its peak valuation.

Cbus Property is set to acquire a 50% share of 5 Martin Place in the Sydney CBD for $310 million, as reported by Australian Property Journal, which had previously shown a valuation of $405 million two years ago.

Meanwhile, Mirvac has sold its e 40 Miller Street North Sydney office building to Barings for $140 million and 367 Collins Street for $345 million, at a 20% discount to peak book values.

And Swiss fund AFIAA sold off its 628 Bourke Street for $115.8 million to Bayley Stuart, far below the $185 million it paid M&G Real Estate seven years ago.