This article is from the Australian Property Journal archive

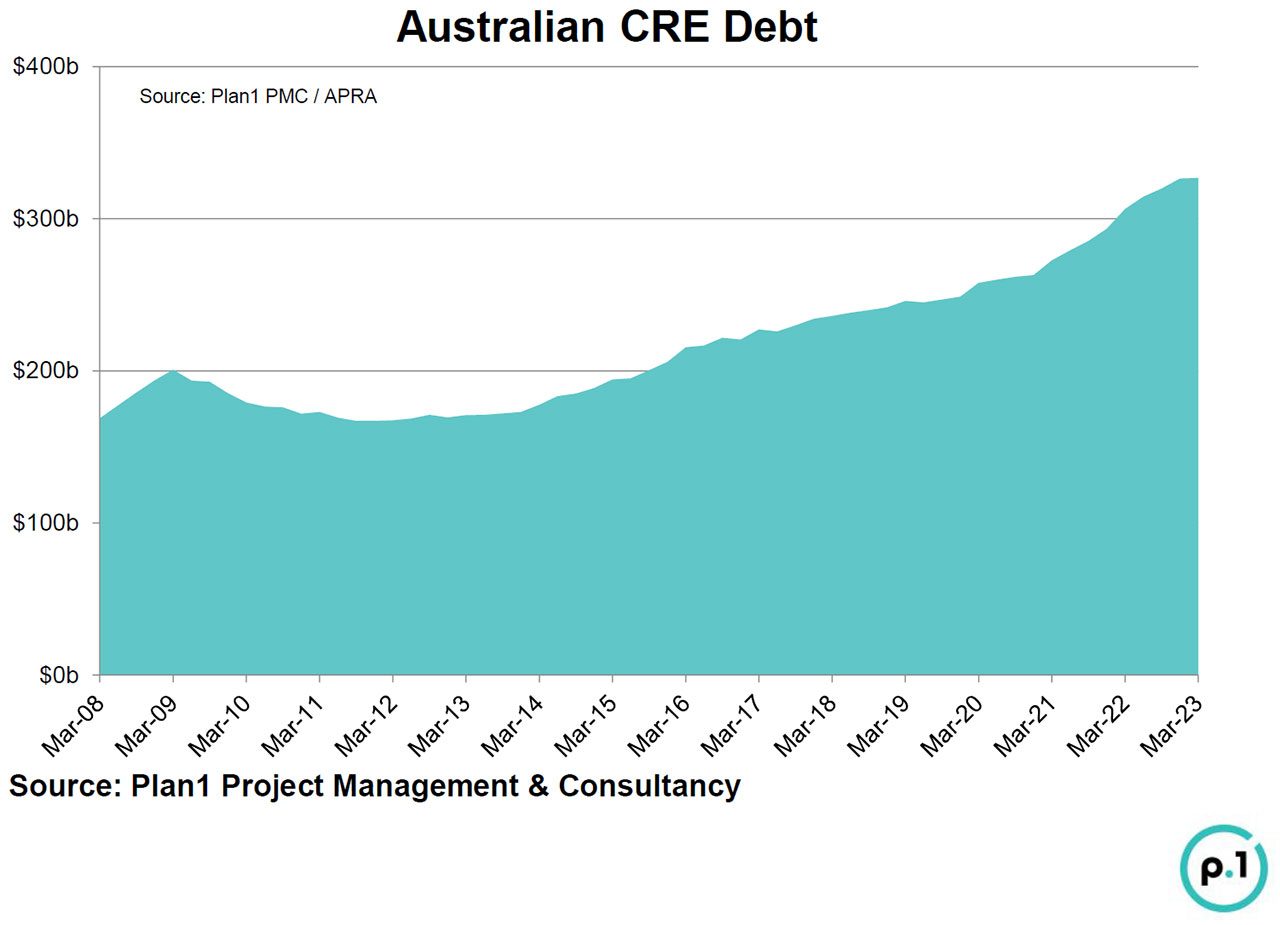

At $326.7 billion, total Australian commercial real estate debt has hit a new high, with banks increasingly focusing on the more resilient industrial sector.

According to the latest research from Plan1, total Australian real estate debt was up 6.7% over the last year, reflecting a $20 billion increase well above the 10-year annual average increase of $15 billion.

“With industrial and logistics properties benefiting from the acceleration in the structural shift to online retail trade, lenders have increasingly sought to increase their exposure to the sector,” said Richard Jenkins, co-founder at Plan1 Project Management & Consultancy.

“Australian industrial CRE debt has increased by 42% over the past two years, far surpassing the gains of the other sectors.”

Jenkins noted that CRE debt provided to the retail sector outpaced growth to the office sector, reflecting the ongoing uncertainty in the office space since the onset of the COVID-19 pandemic, with occupancy rates still low.

Australian ADIs cut back their exposure to the sector by more than $3 billion over the quarter, which was the most significant drop in the sector in 14 years.

Though the office sector does still make up 30% of all CRE debt held by Australian ADIs.

With ADIs withdrawing, the office sector offered non-bank lenders investment opportunities with landlords having to live up to improved ESG requirements and tenant demands.

“With inflation maintaining upward pressure on interest rates, economic uncertainty and hybrid work keeping office usage well below pre-pandemic levels, financing office assets remains challenging, with the cost of capital increasing and lender appetite diminishing,” added Jenkins.

Australian ADIs exposure to high-density residential development was also down for the quarter, with the number of apartments under construction still declining and debt provided to high-density developments also down annually.

“The composition of lenders in the Australian CRE debt market continues to evolve, with the share of Australian CRE debt held by the major banks (ANZ, NAB, CBA and Westpac) continuing to decline, falling to 68.4%, their lowest share of Australian CRE debt since March 2009,” said Jenkins.

The share of Australian CRE debt held by the major banks peaked at 84.7% in 2013, with Australian CRE debt held by the major banks decreasing over the quarter at the fastest rate since 2017.

“In response to APRA’s revisions to ADI capital requirements, banks have been forced to reweight their portfolios to loans backed by income-producing real estate assets,” added Jenkins.

“CRE debt exposure held by the major banks in the industrial and retail sectors have all reached record highs while their exposure in the office and tourism sector reduced. Major bank exposure to office sector lowest since 2021.”

Meanwhile, CRE debt held by foreign banks was up over the quarter to sit $8.9 billion higher than the same time last year.

The share of total CRE debt held by foreign banks is now at an all-time high, at 25.6%, having grown by 12%.

“Australia had gone beyond the Basel III global banking regulatory requirements and is the only jurisdiction in the world that mandates large banks carry capital to address the risk of rising interest rates as part of their core capital requirements,” said Jenkins.

“The health of Australia’s banking system is highlighted by the low level of “non-performing” loans (which are regarded as past 90 days due) which totals $1.8 billion (or 0.6% of total CRE debt in Australia).”

Jenkins concluded that the health of the Australian banking system remains in good shape but increased regulatory pressures have impacted the major banks’ capacity to meet CRE debt demand, leaving increased space for investment from foreign banks and non-bank lenders.