This article is from the Australian Property Journal archive

OUTSTANDING senior commercial real estate debt in Asia Pacific totals at least US$257 billion, and Australia faces the largest funding gap in the region, according to analysis from CBRE, while investment volumes are expected to grow moderately over 2024 amid ongoing repricing of assets.

The debt funding gap in Asia Pacific expected between 2024 and 2026 of US$8.4 billion is relatively small compared to other major regions – Europe totals US$191.4 billion and the United States US$157.3 billion – owing to the limited repricing in Asia Pacific, which limits opportunities for distressed assets and non-performing loans in the region.

CBRE’s The Debt Funding Gap for Asia Pacific Real Estate report shows Australia faces a funding gap of US$4.6 billion, with mainland China the second-biggest in the region at US$2.9 billion.

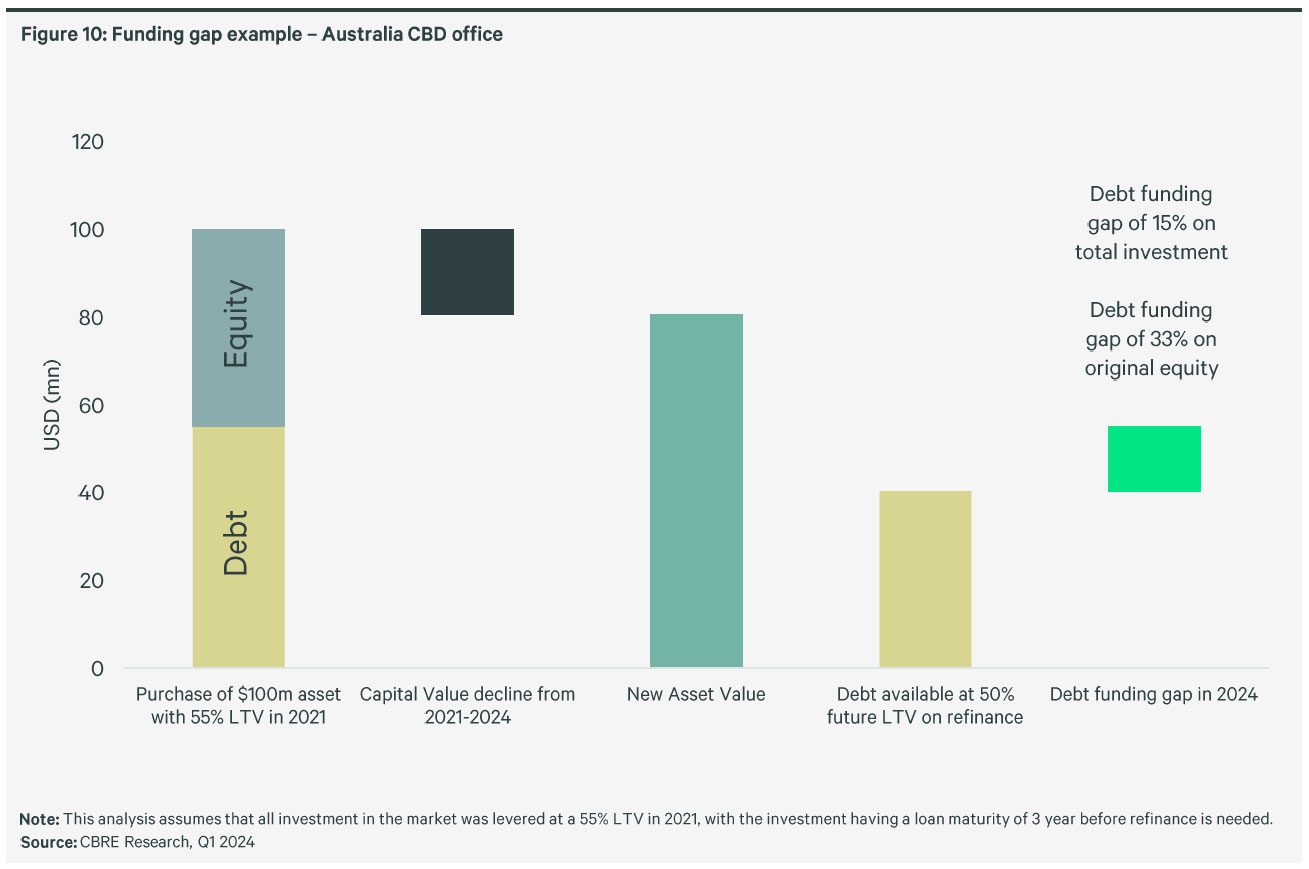

Office towers are expected to face the most significant gap, with further asset repricing anticipated throughout the remainder of 2024 as the sector continues to grapple with the higher vacancies and the working-from-home phenomenon.

“Many buyers believe that further price erosion and increased tenant demand are needed to justify current pricing.

“This repricing will particularly affect secondary properties that are currently out of favour with tenants. However, distressed office acquisitions will be limited in selective markets,” according to CBRE.

With the exception of those in mainland China, Japan and Singapore, current investments in most markets have been repriced in the range of 50 basis points to 200 basis points of cap rate expansion.

Banks will determine the extent to which the debt funding gap leads to distressed sales, with 72% of debt origination in Asia Pacific over the past three years being recourse loans.

“If banks become more aggressive in pursuing assets within underperforming investor portfolios, the risk of distress in certain markets and sectors will increase.”

Greg Hyland, head of capital markets, Asia Pacific for CBRE said that with cap rates expansion set to moderate and rates likely to stay higher for longer in the Asia Pacific, CBRE anticipates increased buying opportunities in the second half of 2024, particularly in the office sector.

CBRE expects commercial real estate investment volume in Asia Pacific to grow by 5% year-on-year in 2024, led by Japan, Korea and India, while other markets are poised to recover from a lower base. Buyers, particularly private and high-net-worth investors, will become increasingly active once there is greater clarity around future rate movements in the second half of 2024, CBRE expects.

“Property owners that want to refinance need to carefully monitor interest coverage ratios and interest expenses. The analysis shows that refinancing costs in Australia and Hong Kong SAR could be up to 1.9 times higher over the next two years.”

Japan will also undergo restructuring in interest expenses following the end of negative interest rates.

Henry Chin, global head of investor thought leadership and head of research, Asia Pacific for CBRE, said equity investors can find “attractive” opportunities, while alternative lenders may benefit from working with banks to restructure commercial real estate and development exposure in specific markets.

Overall, CBRE expects debt-specific funds to be limited, with most likely to consist of partly traditional strategies such as value-add, owing to the limited funding gap and capital raising issues within the region.