This article is from the Australian Property Journal archive

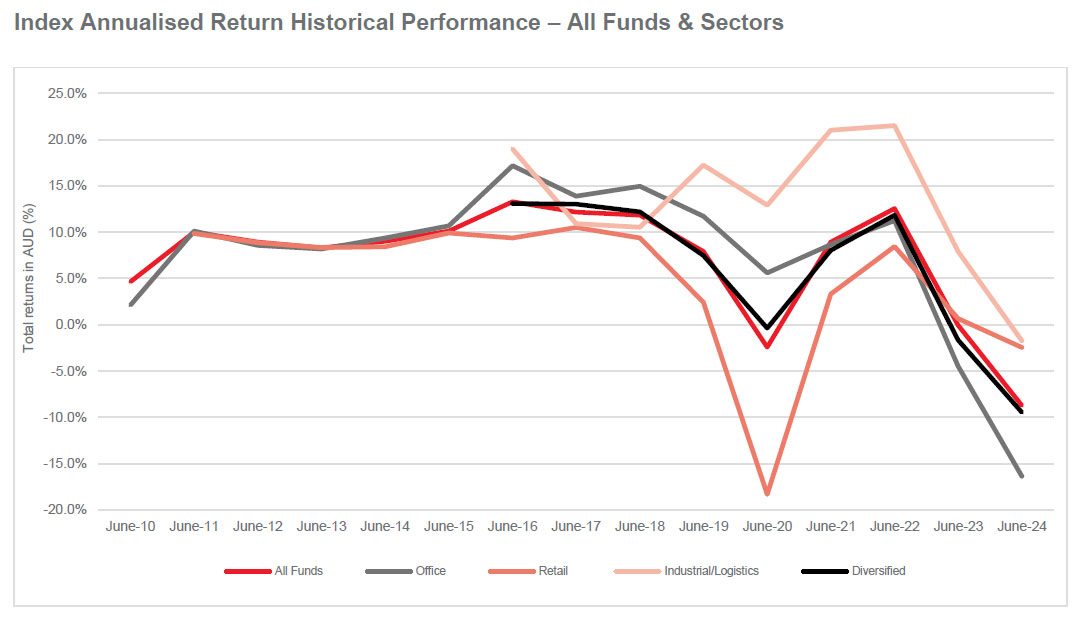

CORE open-end funds in Australia saw a negative total return of 8.7% in FY24 on the back of declining asset values and high interest rates, and there may still be value pain to wash through yet, as cost of debt and inflation remain high.

ANREV’s Australia Core Open End Fund Monthly Index (ACOE) showed the capital growth component declined by 11.7% year-on-year, mitigated by the income return which amounted to 3.36%, “illustrating the headwinds experienced by non-listed real estate investment vehicles in the Australian market”.

“The latest performance of the core open end funds in Australia reflects the macroeconomic headwinds that are still weighing on the sector, and this may continue to persist for some time,” warned senior director of research and professional standards at ANREV, Amélie Delaunay.

“Given the repricing in the market, it remains to be seen whether such may relaunch market activity.

Office single sector funds broadly delivered a “lacklustre” performance, with measured funds delivering net annual total return in the range of -12% to -25% as capital values declined. This translates to the sector level performance in which the annual performance registered a total return of -16.34%.

“It is noteworthy to highlight that for the office-focused funds, along with the decline in value the gearing also rose significantly from 24% at the end of June 2023 to 28% at the end of June 2024,” Delaunay said.

Office sales transactions increased from a low base in the June quarter as large institutional sales started to filter through, typically at notable discounts to peak and prior book values.

Among those, Cbus Property is spending $310 million to acquire a 50% share of 5 Martin Place in the Sydney CBD, as reported by Australian Property Journal, which had shown a valuation of $405 million two years ago, while Mirvac has just divested the 40 Miller Street, North Sydney office building to Barings for $140 million, and 367 Collins Street in Melbourne for $345 million, with both deals struck at a 20% discount to peak book values.

“Though transactions have resumed, pricing may take a while to bottom out as cost of debt and inflation remain persistently high, and there has been renewed volatility in the interest rate outlook,” said Jade Tan at APG.

“The underperformance of the office sector return is a reflection of weak fundamentals. Lease negotiation periods continued to be protracted with minimal change in tenant footprints due to the work-from-home practice. Well-located quality office assets that meet sustainability and amenity requirements will benefit from stronger tenant demand and drive bifurcation.”

Retail-focused funds registered -2.45% total return for the past year – however, the average was dragged down by one fund as all the other measured funds delivering positive total returns. Outperformers were the GPT Wholesale Shopping Centre Fund and the ISPT Retail Australia Property Trust, with both funds delivering one-year net total return of 2.49%.

“The retail sector seems more resilient to the current market environment and the polarising performance of the different sectors suggest the increasing importance of diversification in asset and sector allocation,” Delaunay said.

“Retail presented more resilient returns than expected, reversing the underperformance over the last decade or so. Retail’s performance appears to be underpinned by population growth, stable spending intentions and limited new retail supply, especially regional developments.”

As the industrial sector typically has in recent years, funds focused on logistics returned the best set of numbers. Total return was slightly down, by 1.72%, which outperformed the all funds average as well as the other sector funds. Goodman GAIP fund was the best-performing single sector industrial fund, recorded a one-year net total return of 1.63%.

Delaunay said that Despite some slowdown, demand remained solid in the industrial sector due to the push toward automation and efficiency, localisation of supply chain and continued growth in ecommerce and consumer demand.