This article is from the Australian Property Journal archive

DEMAND for office has improved across all CBD markets in the six months to January with tenants requiring more space as the COVID-19 pandemic changes how we use workspaces.

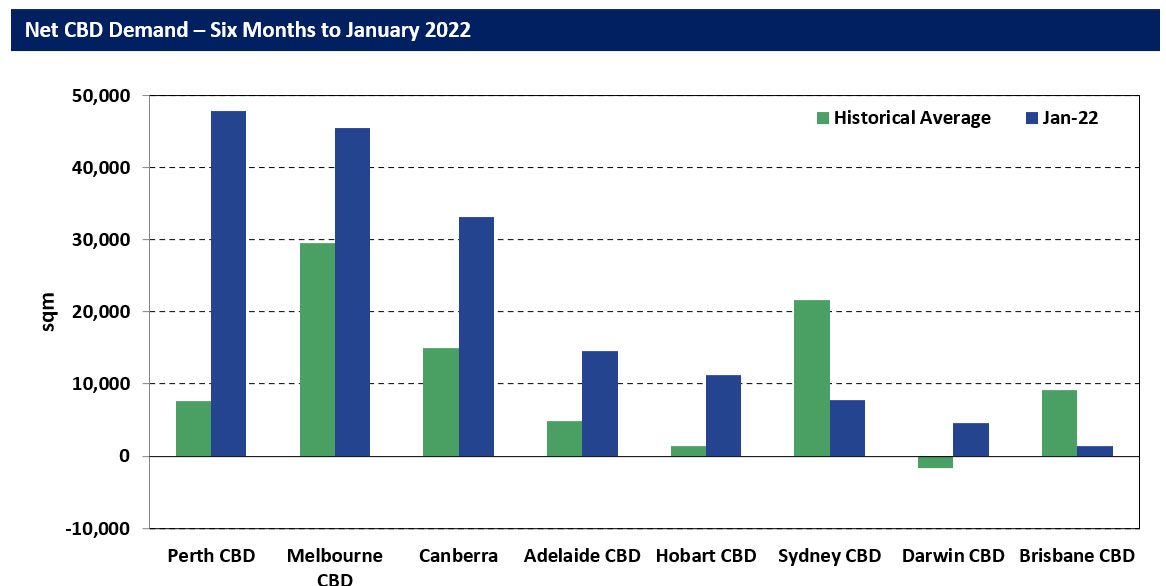

According to the Property Council of Australia’s latest Office Market Report, tenant demand improved by average 1% across the CBDs, and 0.7% in non-CBD markets.

With the exception of Sydney and Brisbane, all other cities reported demand increases higher than their historical average.

Property Council of Australia chief executive Ken Morrison said the figures were very heartening, especially given the spread of Omicron.

“These are a striking set of figures which illustrate that the office is alive and well in today’s economy, even as the pandemic changes how we use workspaces.

“While many expected this once in 100 year global pandemic to cause a major spike in office vacancy, these figures show that hasn’t eventuated,” he added.

Although the lift in demand was not enough to offset the new supply, which pushed vacancy rates marginally higher from 11.9% to 12.1%, CBRE head of office leasing, Pacific, Mark Curtain said the national office market continued to recover through H2 2021.

“Despite Sydney and Melbourne being in lockdown for more than 50% of this period, tenants around the country pressed on, implementing their long-term office accommodation strategies.

“Net absorption across Australia for the full year improved significantly, recovering all of the ground lost in 2020 and then some. Most markets have now passed the worst of the downturn and we expect the recovery story of the Australian office market to continue in 2022.

“The national recovery has been led by Sydney, where leasing market fundamentals have largely stabilised, and enquiry and deal volumes have increased considerably over 2020 levels. Sydney recorded more than 500,000sqm of new tenant enquiries throughout 2021 – a record high – translating into 200,000 deals for 1,000sqm-plus spaces. Notably, Sydney’s sublease vacancy reduced by more than 44% during the year, a good indication that the worst of the office market downturn is now past us.” Curtain said.

Sydney

Sydney CBD has more than 150,000 sqm of new and refurbished space coming online CBD over 2022. The average Prime grade incentive remains at 35% and gross face rents continue to average $1,355 sqm per annum (pa). Although the Omicron variant has increased the downside risk to this forecast in the short term, barring further economic restrictions growth may be pushed back into the second half of 2022.

Cushman & Wakefield national director, office leasing, Jamie King said the first two weeks of 2022 saw approximately 30 new briefs in the market with requirements totalling circa 18,000sqm, a positive sign for the year ahead.

“Existing quality fit outs and new build fit outs are the key focus for tenants, as opposed to refurbished suites. Working from Home pressures continue along with a fight for talent, resulting in tenants keen to place make their new office providing reason for a return from staff.”

Melbourne

Melbourne CBD net incentives stabilised in Q4 2021 with premium grade net incentives are 39% for the third consecutive quarter.

Cushman & Wakefield joint head of CBD office leasing Chas Keogh said the Melbourne CBD office market has become quite segmented, and incentives aren’t necessarily the key story anymore, although they look to have stabilised, with landlords being able to hold face rents steady.

“Smaller tenants do have greater optionality by comparison to larger occupier however that isn’t abnormal in any market. However, what it does highlight for landlords targeting these tenants is that how they position their asset needs to fast tracked and proactive.” Keogh said.

CBRE head of office leasing Victoria Ashley Buller observed that the overall, CBD occupancy levels remain low, expected to improve when government occupants return in 2022.

Buller said the sub-500sqm market remains the most-active sector, and prime-grade owners are continuing to construct spec suits across the market in a bid to capitalise on this.

“As measured by CBRE, Melbourne’s sublease availability sat at approximately 190,000sqm as of December 2021, which is a historical high.

“The Southern Cross precinct has completed more sublease transactions than any other precinct. Sporadic successes through the CBD and fringe sublease market have tended to follow sub-lessors who were prepared to walk away from their fitout and furniture improvements for nil or minimal return, and extend an additional market incentive. Typically, as time has passed, the incentive has increased from a target to recover full costs to a compromised level or cost recovery.” Buller said.

Brisbane

Brisbane CBD gross effective rents have remained stable in both the Premium and A grade office markets across 2021, with gross effective rents averaging $540 and $410 per sqm per annum, respectively. B grade gross effective rent remains at $340 sqm pa. Like the rents, incentives in Premium and A grade markets have remained stable for 2021, with gross incentives averaging 37.5% and 41.5% respectively. B grade incentives remain at 45.0%, having only recorded a slight increase in Q2.

Colliers office leasing national director Matt Kearney said whilst the current total market vacancy rate in the Brisbane CBD sits at 15.4% and is likely to peak just shy of 16%, the demand outlook for new developments and prime grade assets is strengthening with most occupiers now seeking next-generation workplaces.

“This activity has no doubt created positive momentum with current market requirements including BDO, Hopgood Ganim and Brisbane City Council. We are also expecting further requirements to come online in 2022 from the major banking, energy and professional services sectors.

“We have no doubt that the CBD is on the road to returning to its former glory. Brisbane is now in the enviable position of entering a ‘golden decade’ as the 2032 Olympic City which will further endorse the appeal of Brisbane as an idyllic destination to live, work and play and will see significant economic benefits.” Kearney said.

Gold Coast

Cushman & Wakefield Gold Coast associate director Ed Howard said the Gold Coast strata market is performing well with most of vacant office strata being purchased by owner occupiers.

“Notably the Gold Coast strata office market makes up about 30% of all office space that exists in the city, being the highest concentration of strata titled office property compared to any other city/office market in Australia.”

CBRE Gold Coast senior director Tania Moore said the market is experiencing ongoing high demand from the SME sector, along with the education sector following the opening of international borders to students.

“The main challenges for Gold Coast occupiers in 2022 will be limited stock opportunities under 150sqm and over 750sqm. Managing timelines on fitout construction, due to the lack of supplies and availability of contractors, and forward planning will also be critical.

“There is currently approximately 21,200sqm of new office space under construction, with precommitments accounting for about 40% of the supply that’s due for completion between mid-2022 and mid-2023. In the core office precincts, 8,800sqm of new supply is being constructed and only 908sqm remains for supply, therefore we do not expect any real impact to the market from these additions.” Moore said.

Adelaide

Meanwhile it will be a landlords market in Adelaide in the year ahead as there will be next to zero availability when it comes to large amounts of new Prime-grade space in the city.

CBRE director Andrew Bahr said strategic repositioning discussions are continuing in relation to various assets, though, which will result in large vacancies in 2023, and all of Adelaide’s new builds are on track for completion as scheduled.

“Sublease availability continues to decline, falling by 42.7% in Q4 to just 4,900sqm of available supply. That is Adelaide’s lowest figure since June 2020, and comfortably the lowest of any city in Australia, representing only 1% of the national total.

“The impact of 2022’s state and federal elections is yet to be seen, and this may have an effect on demand and companies’ decision-making until the outcomes of those are known. Historically, though, any impact has been short-lived, and we would expect demand to remain strong throughout the year.” Bahr said.

Canberra

Canberra had a strong finish to 2021 with vacancy levels continuing to tighten. CBRE director Troy Markos said occupiers did not have as much choice as they once had, especially in specific locations and in the A-grade market, which is desperately in need of new supply coming online in 2022.

“The lack of supply and flight to quality has resulted in an uplift in face rents, and kept incentives relatively consistent.

“Enquiry levels remained strong in the second half of the year. From the enquiries, 71% sought space smaller than 500sqm, and 18% in excess of 1,000sqm, with the Commonwealth Government seeking the majority of the larger requirements.

“The Commonwealth government remained active despite the looming 2022 election. In H2 2021, numerous long-term requirements came to market, such as for the Australian Maritime Safety Authority, while shorter-term project space requirements slowed compared to H1. There remains a lack of suitable A-grade supply and options suitable to Commonwealth standards,” he added.

Perth

Overall vacancy in the Perth CBD declined further over the second half of 2021 to 15% from 16.9%. Cushman & Wakefield WA director James Cox said face rents within Premium and A-grade office buildings in Perth have remained relatively stable for the past 12 months whilst incentives remain at historical highs ranging from around 45% to 55% depending upon the face rent, lease term and quality of covenant.

“We are seeing a higher percentage of longer (7 to 10 year) lease terms being negotiated for Premium and high A grade space as tenants seek to lock in historically high incentives, with a flight to quality and centrality being a continued theme from tenants moving away from older secondary office stock.” Cox said.

Meanwhile Morrison said talks about a pandemic-led collapse of the office market were premature.

“The reality is that most CBD businesses continue to see the office as integral to their future, and that is reflected in the increased demand for office space over the past six months.

“The comparison to the 1990s recession is stark. During that crisis, vacancy rates blew out by a massive 15.6% over three years, whereas during the two years of the COVID-19 pandemic, they’ve shifted only 3.3%.

“The data matches what we’re hearing, and that is that tenants clearly see collaborative and well-designed office space as a key component of their ‘new normal’ of working.

“Although these results illustrate the resilience of the office market, there remains a critical need for governments and businesses alike to reinvigorate our CBDs as soon as the health situation allows, and the Property Council of Australia remains committed to leading and contributing to those efforts,” he concluded.