This article is from the Australian Property Journal archive

HIGHER-for-longer interest rates, falls in office tower values and slowing economic growth mean risks to credit quality will rise for REITs in the Asia-Pacific in 2024, according to Moody’s Ratings, as bumpy conditions will bring another year of softer rental growth and higher vacancies.

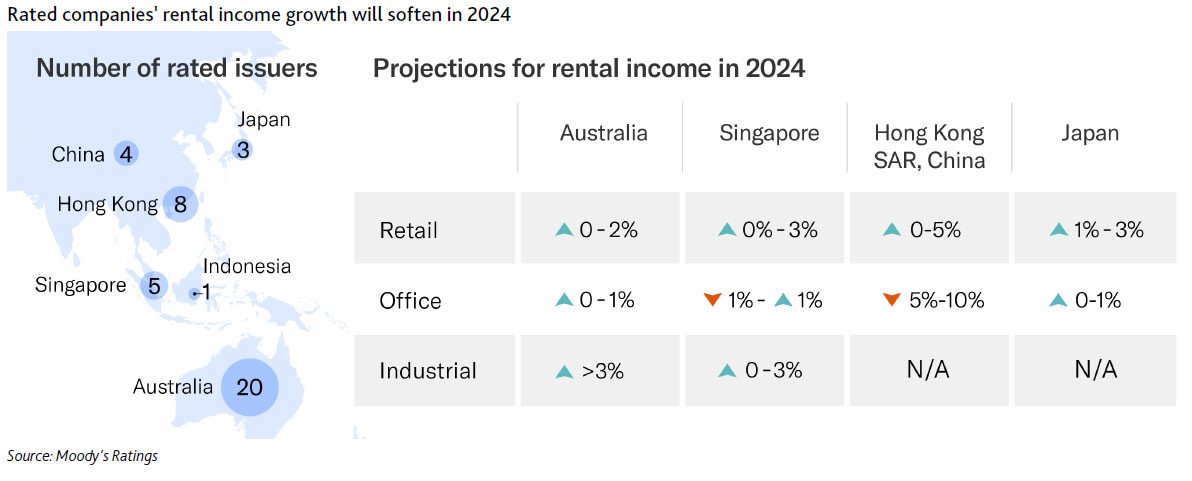

“Rental income growth for rated companies in the next 12 months will soften from the levels we had projected for 2023,” Moody’s Ratings said in its new report, Risks to credit quality to increase in 2024 amid high interest rates and office weakness.

“The combination of lower income growth and elevated interest rates will weaken rated companies’ credit metrics in 2024. But we expect an improvement in 2025, as macroeconomic conditions recover.”

“Office is particularly exposed among property sub sectors as weaker corporate sentiment and layoffs hit demand.”

“Weak demand for offices combined with oversupply constrains rents and occupancy levels.”

Average rental income growth for rated companies’ office portfolios will be “muted” in 2024, according to Moody’s Ratings, with the weakest performance in Hong Kong while growth will be “very modest” in Australia and Japan.

The firm said office rental income in Australia will supported by built-in annual rental escalations of 3% to 4%, but it expects incentives to remain high, which will offset growth in effective rents.

“Market vacancy levels have increased above historical averages, and we expect further increases in the next 12 months as more supply comes online.

“However, rated companies’ vacancy levels will remain stable at around 5% on average, reflecting the high quality of their asset base. Companies with well-located and good quality assets will continue to outperform those with secondary assets.”

Office rental income in Hong Kong will fall by between 5% and 10% in 2024 amid a supply glut and weak corporate expansion demand, the report said, while in China, the office segment will continue to weaken, driven by a high vacancy rate and lower rents, dampened further by the economic slowdown.

Singapore office rental income will be flat in 2024 amid weaker demand and new supply, while in Japan, modest growth in office rents in 2024 reflects stable supply and demand dynamics.

“The flight to quality continues to favour well-located and good-quality office assets owned by rated real estate companies. Vacancy rates in the market are still higher than pre-pandemic levels, but lower than those in other APAC gateway cities, such as Sydney, Melbourne and Hong Kong. The comparatively high office attendance rate after the pandemic will also likely support Japan’s office market.”

Weaker consumer spending will weigh on retail asset performance. But suburban assets that mostly cater to non-discretionary spending will be resilient, in contrast to downtown assets, which are more reliant on discretionary spending and tourism. Demand for industrial assets will ease from strong levels as a boom fades in the e-commerce and supply chain solutions sectors.

APAC interest rates likely to have peaked

“Interest rates in Asia-Pacific have likely peaked and will start to decline gradually,” the report said.

“Consequently, we expect rated real estate companies will start to see meaningful improvement in their credit quality in 2025. Lower borrowings costs will reduce interest expense. And a decline in interest rates will arrest the decline in property valuations.”

The Reserve Bank of Australia kept interest rates on hold, at 4.35%, at this week’s meeting, and a shift in its language on the path forward for interest rates was described by some analysts as “dovish”.

In a client note this week, Citi analyst Suraj Nebhani said, “Further asset value declines are likely in the Jun-24 half, but we see limited scope for declines beyond that given a favourable rate outlook in the second of calendar year both globally and in Australia”.

“We are positive on REITs into this rate stabilisation with key picks in sub-sectors with favourable demand supply dynamics including industrial, alternatives (land lease and self-storage) with recovery likely to benefit residential and fund managers.”

Australia’s largest owner of office buildings, Dexus swung to a first-half loss as another $687 million was wiped off the value of its portfolio as changing workplace habits continued to bring uncertainty to the sector. That followed a $1.184 billion devaluation in the previous half. Asset value losses were seen across the commercial real estate sector in 2023 as rising interest rates have affected yields and the office sector grapples with structural headwinds such as working from home.

Population growth and low supply to support retail sector

Moody’s Ratings expects retail sales growth will ease in 2024 as consumer spending slows on the back of still-elevated inflation and interest rates.

“Rated issuers with downtown retail assets and tenants that are exposed to discretionary products and services will be the most affected. But suburban assets that mostly cater to non-discretionary spending will prove to be more resilient.”

Rental income growth for retail property owners in Australia, Singapore and Hong Kong will moderate, it said, in contrast to slightly higher rental income growth in Japan.

In Australia, rental income growth of 0% to 2% will be underpinned by strong occupancy, improved releasing spreads, and rent increases either linked to the consumer price index or fixed, but weak sentiment and consumption will weigh on retail asset performance.

“Rated issuers with central business district retail assets and tenants that sell discretionary products and services will be the most exposed as foot traffic in the CBD has not yet returned to pre-pandemic levels and buyers remain cautious about rates and inflation.

“But overall population growth and low new supply of retail space will support the performance of rated Australian REITs, some of which will outperform our rental income growth estimates.”

E-commerce boom fading

The industrial sector continues to outperform other asset classes although rental growth and demand will moderate, Moody’s Ratings said.

“An e-commerce boom is fading, while economic growth is slowing and vacancy rates are climbing along with new supply. However, demand for well-located urban infill industrial assets will persist as tenants focus on cost management and supply-chain efficiencies,” Moody’s Ratings said.

It said industrial assets will continue to exhibit the strongest rental growth among all asset classes and the Australian market will remain remain tight. Rent growth will be above 3% in 2024 but lower than previous highs, as new supply comes online and vacancy rates steadily increase. Around 50% of supply in key markets is pre-committed, which will limit the impact on vacancy rates.